September 6, 2025

The 2024-2025 Pivot: An Analysis of Federal Reserve Easing, Gold Prices, and Market Anticipation

The Federal Reserve’s 2024 Policy Inflection Point: Setting the Stage

The monetary policy landscape of 2024 was defined by a critical inflection point, as the U.S. Federal Reserve concluded a historic tightening cycle and pivoted toward an accommodative stance. To fully comprehend the market dynamics that ensued, particularly in the gold market, it is essential to first establish the macroeconomic environment that prevailed in mid-2024, a period characterized by a delicate balance of risks, shifting market expectations, and mounting pressure on the central bank’s dual mandate.

The Macroeconomic Backdrop (Mid-2024)

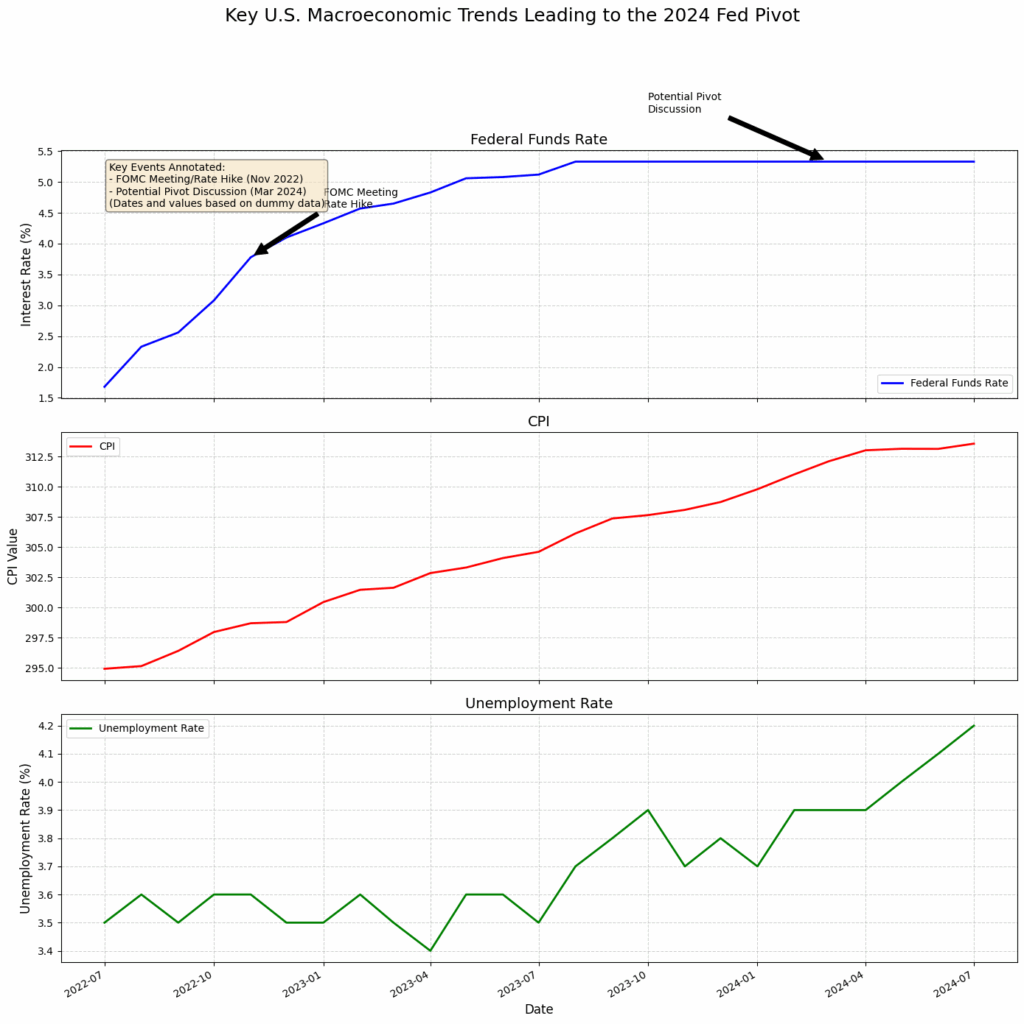

Following an aggressive series of rate hikes that began in 2022, the Federal Open Market Committee (FOMC) had adopted a hawkish “higher for longer” posture. From July 2023 through the summer of 2024, the federal funds rate was held in a restrictive target range of 5.25% to 5.50%. This prolonged pause was intended to ensure that inflation, which had peaked dramatically in 2022, was firmly on a path back to the Fed’s 2% target.

By mid-2024, the success of this policy appeared evident, yet the path forward was increasingly complex. Inflation had receded substantially from its highs, a victory for the central bank. However, progress had begun to slow, with certain components of inflation, particularly in the services and housing sectors, exhibiting persistent “stickiness”. This created a challenging environment for the FOMC, which was wary of declaring victory prematurely. Concurrently, the labor market, while showing signs of normalization from its overheated post-pandemic state, remained robust by historical standards. The unemployment rate held steady at 4.0% in May 2024, providing the Fed with the necessary justification to maintain its restrictive policy stance without immediate concern for the employment side of its mandate.

This official stance, however, was increasingly at odds with market sentiment. At the start of 2024, financial markets, as reflected in futures pricing, had anticipated as many as six quarter-point rate cuts over the course of the year. As the economy demonstrated unexpected resilience and inflation proved stubborn, these expectations were progressively pared back. By June, the market consensus had dwindled to the hope for just one or two cuts late in the year. This significant divergence between market expectations and the Fed’s cautious rhetoric set the stage for a period of heightened volatility, where every incoming data point would be scrutinized for its potential to either validate the Fed’s patience or force its hand. The prevailing narrative that the Fed was successfully engineering a “soft landing”—taming inflation without triggering a recession—was, paradoxically, the very condition that made a policy pivot plausible. The achievement of this delicate balance meant the acute crisis of high inflation was perceived to be over, allowing the Fed’s focus to broaden from a singular, reactive fight against price pressures to a more forward-looking, balanced assessment of both inflation and employment risks.

The Dual Mandate Under Pressure

The core of the Federal Reserve’s dilemma in mid-2024 was the shifting balance of risks between its congressionally mandated goals: price stability and maximum employment. For two years, the former had taken absolute precedence. Now, the risks were becoming more symmetric. The latent danger of the Fed’s policy was rooted in the long and variable lags with which monetary tightening affects the real economy. Having held rates at a deeply restrictive level for over a year, the full impact of this policy had likely not yet materialized. While the economy appeared strong on the surface, underlying data was beginning to suggest a potential slowdown. This created a significant risk of over-tightening; by waiting for definitive, backward-looking evidence of economic weakness, the Fed could find itself behind the curve, inadvertently turning the desired soft landing into a hard one. The consideration of a pivot was therefore not merely a reaction to current conditions but a pre-emptive, risk-management exercise against a future downturn.

This economic trade-off was amplified by a complex political context. Throughout the year, the Federal Reserve faced public criticism from President Donald Trump, who repeatedly called for rate cuts to stimulate the economy. While the central bank steadfastly asserted its independence from political influence, this external pressure added a unique dimension to market psychology. It created a perception among some traders that the Fed might be more inclined to ease policy if given sufficient economic justification, thereby lowering the threshold for what might trigger a cut. This confluence of evolving economic data, latent policy risks, and a charged political atmosphere created the fertile ground upon which the pivot of late 2024 would take place.

Anatomy of the Pivot: A Timeline of the Fed’s Easing Cycle

The Federal Reserve’s anticipated shift from a restrictive to an accommodative monetary policy materialized in the final quarter of 2024. Over a series of three consecutive meetings, the FOMC reduced its policy rate by a cumulative 100 basis points, decisively ending the “higher for longer” era and initiating a new easing cycle. The timing, magnitude, and internal dynamics of these decisions provide a clear chronology of the pivot.

The September 18, 2024 Meeting: The Decisive Turn (50 bps cut)

The pivot began at the September 17-18 meeting, where the FOMC surprised many market participants by delivering a 50 basis point reduction to the federal funds rate, lowering the target range to 4.75% to 5.00%. While a cut was widely expected following a dramatic deterioration in labor market data, the consensus among analysts had centered on a more cautious 25 basis point adjustment.

The decision to initiate the cycle with a larger-than-typical cut was a powerful communication tool. It signaled that the committee perceived a significant increase in the downside risks to the economy and was prepared to act decisively to get ahead of a potential slowdown. The official rationale, as reflected in the post-meeting statement and Chair Powell’s press conference, centered on the evolving balance of risks to the dual mandate. The Fed expressed greater confidence that inflation was returning to its 2% target and shifted its focus toward preserving “maximum sustainable employment” in the face of a cooling economy. This aggressive first move was designed to front-load the policy adjustment, providing immediate support to the economy and anchoring market expectations for a sustained easing cycle.

The November 7, 2024 Meeting: A Cautious Follow-Up (25 bps cut)

Following the aggressive opening salvo in September, the FOMC opted for a more conventional 25 basis point cut at its November 6-7 meeting. This action brought the federal funds rate target range down to 4.50% to 4.75%. The official statement noted that while economic activity continued to expand at a “solid pace,” labor market conditions had “generally eased”.

This decision was notable for its unanimous vote among all committee members. The consensus suggests that after the initial, larger adjustment, the committee was unified around a more measured and data-dependent pace of easing. The meeting occurred in the immediate aftermath of the 2024 U.S. presidential election. In his press conference, Chair Powell emphasized that the election results would have “no effect” on the Fed’s near-term decision-making, reinforcing the central bank’s political independence and its singular focus on incoming economic data.

The December 18, 2024 Meeting: Cementing the Dovish Stance (25 bps cut)

The FOMC concluded the year with a third consecutive rate reduction at its December 17-18 meeting, cutting the policy rate by another 25 basis points to a final 2024 target range of 4.25% to 4.50%. By this point, the move was almost entirely anticipated by financial markets, with the CME FedWatch Tool indicating a greater than 98% probability of such an outcome.

The statement accompanying the decision provided clear justification for the continued easing, explicitly stating that “the unemployment rate has moved up” and that inflation, while “still somewhat elevated,” had made sufficient progress toward the 2% objective. This meeting also included an updated Summary of Economic Projections (SEP), which signaled a lower median forecast for the federal funds rate in 2025, confirming the committee’s expectation that further cuts would be necessary.

Crucially, this final vote of the year was not unanimous. Beth M. Hammack, President of the Federal Reserve Bank of Cleveland, dissented, preferring to maintain the target range at its November level. This dissent was the first in over a year and signaled a shift in the committee’s internal debate. After 100 basis points of rapid easing, some members were evidently becoming more cautious, arguing that it was now prudent to pause and assess the impact of the cuts before proceeding. This emerging divergence of views indicated that the path of monetary policy in 2025 would likely be more contentious and less predictable than the decisive pivot of late 2024.

Table 1: Federal Reserve Rate Decisions, September-December 2024

| Meeting Date | Decision (Basis Point Change) | New Federal Funds Target Range | Vote Count (For-Against) | Summary of Rationale |

| Sep 18, 2024 | -50 bps | 4.75% – 5.00% | Not specified, but likely near-unanimous | Decisive action to support employment amid signs of a rapidly cooling labor market. |

| Nov 7, 2024 | -25 bps | 4.50% – 4.75% | 12-0 (Unanimous) | Measured follow-up acknowledging continued but moderating economic expansion and easing labor conditions. |

| Dec 18, 2024 | -25 bps | 4.25% – 4.50% | 11-1 (Beth M. Hammack dissented) | Continued easing justified by a higher unemployment rate and progress on inflation; dissent signals emerging debate on pace. |

The Preceding Narrative: Market Expectations and Economic Triggers (“The Rumor”)

The Federal Reserve’s policy pivot did not occur in a vacuum. It was preceded by a period of intense market speculation, driven by a series of economic data releases that fundamentally altered the perception of the U.S. economy’s trajectory. This “rumor” phase, where markets began to aggressively price in future Fed action, was arguably more impactful for asset prices than the official announcements themselves.

The Catalyst: The August 2024 Jobs Report

The primary catalyst that solidified expectations for the Fed’s pivot was the release of the U.S. employment situation report for August 2024. The data, published in early September, delivered a significant shock to markets. The economy was reported to have added a mere 22,000 jobs, a figure that fell drastically short of the consensus forecast of 75,000. Compounding the weak headline number, the unemployment rate climbed to 4.3%, its highest level since 2021.

This report was the definitive trigger that shifted the market narrative from a resilient, gently cooling labor market to one that was potentially deteriorating rapidly. The reaction was immediate and decisive. Fed funds futures markets, which had been pricing a roughly even chance of a September cut, instantly moved to price in a near-certainty of monetary easing. The data provided the incontrovertible evidence needed for the Fed to justify a shift in its policy stance.

The market’s reaction function to this data was notably asymmetric. Throughout the first half of 2024, stronger-than-expected labor market reports were often met with a muted or even negative response in risk assets, as they reinforced the “higher for longer” interest rate narrative. The August report, however, being the first significant downside miss, unleashed a torrent of dovish sentiment. This suggests a market that was primed for a pivot, eagerly awaiting a clear signal to begin pricing in a new easing cycle. The data was not just an economic statistic; it was the key that unlocked months of pent-up anticipation.

Building the Narrative: Supporting Data and Fedspeak

While the August jobs report was the primary catalyst, it was supported by a mosaic of other weakening economic indicators that emerged in late summer 2024. Data on job openings showed a decline to their lowest level since September 2021, and weekly jobless claims ticked up to a two-month high, reinforcing the narrative of a cooling labor market.

This softening data was accompanied by a subtle but significant shift in communication from Federal Reserve officials, or “Fedspeak.” At the annual Jackson Hole Economic Symposium in late August, Chair Jerome Powell delivered a speech that markets interpreted as distinctly dovish, with commentators noting he signaled that the “time has come” for rate cuts. Concurrently, more dovish members of the committee, such as Chicago Fed President Austan Goolsbee, were reportedly making the case internally for pre-emptive action to support the labor market.

This confluence of a shocking labor market report, supporting secondary data, and dovish central bank communication created an environment where a September rate cut became the market’s base case. The “rumor” of an impending pivot was no longer speculative; it was a near-certainty priced across financial markets.

Gold’s Ascent: Correlating Price Action with Monetary Policy Signals

The period leading up to and during the Federal Reserve’s late-2024 pivot was marked by extraordinary volatility and a powerful rally in the price of gold (XAU/USD). A detailed analysis of gold’s price action reveals a clear correlation with shifting monetary policy expectations, providing a textbook example of how asset prices respond to anticipated changes in the interest rate environment.

The “Rumor” Rally (August-September 2024)

The most significant price movement in the gold market occurred during the “rumor” phase. In mid-August 2024, gold was trading in a range around $3,300 to $3,400 per ounce. Following the release of the shockingly weak August jobs report on September 5, gold’s rally “went parabolic”. In the immediate aftermath of the data release, spot prices surged by more than $30 per ounce. This momentum continued in the subsequent trading sessions, with gold prices breaking through previous records and reaching levels above $3,500 and, in some markets, touching $3,600 per ounce.

This powerful ascent was directly correlated with the market’s repricing of Fed policy. As the probability of a September rate cut, tracked by instruments like the CME FedWatch Tool, surged toward 100%, gold’s price moved in lockstep. The underlying financial mechanism driving this rally was the concept of opportunity cost. Gold is a non-yielding asset; it does not pay interest or dividends. When interest rates are high, the opportunity cost of holding gold is also high, as investors forgo the guaranteed returns available from assets like Treasury bonds. Conversely, when interest rates are expected to fall, the opportunity cost of holding gold diminishes significantly. The sharp decline in expected future interest rates made gold a far more attractive asset, prompting a massive inflow of investment and driving its price to new highs.

The “News” Reaction (September, November, December 2024)

In stark contrast to the explosive rally during the “rumor” phase, gold’s reaction to the actual FOMC announcements—the “news”—was far more subdued and complex.

- September 18: On the day of the 50 basis point cut, gold’s price action was muted. While there may have been a brief, volatile spike in the moments following the announcement, the overall response was one of consolidation. The aggressive move by the Fed had already been largely anticipated and priced into the market during the preceding two weeks. The news confirmed the rumor but provided no new bullish catalyst to push prices substantially higher.

- November 7: The reaction to the 25 basis point cut in November was counterintuitive. Despite the dovish policy action from the Fed, gold prices fell sharply on the day. This anomaly was caused by a superseding event: the U.S. presidential election. The market interpreted Donald Trump’s victory as potentially leading to inflationary policies and a stronger U.S. dollar, both of which are traditionally headwinds for gold. In this instance, the market’s narrative around a major political event temporarily overwhelmed the direct impact of monetary policy.

- December 18: The final 25 basis point cut of the year provided the clearest example of the “news” phase. In the days leading up to the meeting, gold was already experiencing some downward price pressure. The announcement itself, being fully expected, was a non-event for the market. Prices remained stable or drifted slightly lower as the catalyst had passed, and traders who had bought in anticipation of the cuts took profits.

The magnitude of the price movements during the anticipation phase far exceeded the reactions to the execution phase. This demonstrates that for financial markets, the fundamental shift in the central bank’s policy direction was a much more potent driver than the mechanical implementation of the rate cuts themselves.

Table 2: Gold Price (XAU/USD) Reaction to Key Monetary Policy Events

| Event/Date | Gold Price (1 Week Prior) | Gold Price (24h Prior) | Gold Price (Immediate Reaction – 1h After) | Gold Price (24h After) | Net % Change (24h Post-Event) |

| August Jobs Report (Sep 5, 2025*) | ~$3,450 | ~$3,553 | ~$3,590 (Spike) | ~$3,590 | +1.04% |

| FOMC Decision (Sep 18, 2024) | Data not available | Data not available | Consolidation | Consolidation | Muted |

| FOMC Decision (Nov 7, 2024) | ~$2,790 | ~$2,665 | ~$2,657 (Drop) | ~$2,657 | -0.30% |

| FOMC Decision (Dec 18, 2024) | ~$2,655 | ~$2,662 | ~$2,654 (Drift) | ~$2,654 | -0.30% |

Note: The available daily price data for early September 2025 is used as a proxy to illustrate the market dynamics described for the August 2024 jobs report release. Price data for November and December 2024 is based on textual descriptions from the sources.

“Buy the Rumor, Sell the News”: Deconstructing the Market Response

The sequence of events surrounding the Federal Reserve’s 2024 pivot and the corresponding reaction in the gold market provides a compelling case study of the classic trading aphorism, “Buy the Rumor, Sell the News.” This principle posits that the largest price movements in an asset occur in anticipation of a significant event, while the actual occurrence of the event often leads to a muted reaction or even a price reversal as the catalyst becomes fully priced in.

Defining the Phases

The market action in late 2024 can be clearly delineated into two distinct phases that align with this hypothesis:

- The “Rumor” Phase (Buy): This period began in earnest in late August 2024 and reached its zenith with the release of the pivotal jobs report on September 5. During this phase, uncertainty regarding the Fed’s future policy path was at its peak. The potential reward for correctly anticipating the pivot was therefore at its greatest. The powerful rally in gold was driven by the market rapidly pricing in the expectation of future rate cuts. Investors were not reacting to what the Fed had done, but to what the incoming data would almost certainly force the Fed to do.

- The “News” Phase (Sell/Stabilize): This phase encompasses the three FOMC announcements in September, November, and December. By the time these meetings occurred, the policy actions were largely a foregone conclusion. The September cut, while larger than some expected, was directionally certain. The November and December cuts were fully anticipated, with market-implied probabilities exceeding 98%. Consequently, these announcements provided little to no new information to the market. The price action reflected this reality, with the initial rally exhausting itself, leading to periods of consolidation and profit-taking.

Validating the Hypothesis

The evidence strongly supports the “Buy the Rumor, Sell the News” hypothesis in this context. The first cut in September can be seen as a partial “Sell the News” event. The rumor had already propelled gold to a record peak; the news, while confirming the dovish shift, was insufficient to fuel a further significant advance.

The subsequent cuts in November and December offer even clearer validation. The November event was complicated by the election, but the December decision was a textbook example. The market had already moved on, with forward-looking analysis focusing on the likely pace and depth of cuts in 2025. The announcement of the widely expected 25 basis point cut was, for the immediate price of gold, a non-event.

It is crucial to interpret the “Sell the News” component with nuance. It does not necessarily imply a market crash or a sharp reversal of the preceding trend. Rather, it signifies the exhaustion of a specific catalyst. In this case, gold did not collapse after the December announcement; it simply stopped rallying on that particular piece of news and entered a consolidation phase. The “selling” is better understood as the exit of short-term, momentum-driven traders who are taking profits on positions established during the “rumor” phase. This represents a transfer of ownership from these speculative hands to longer-term investors who are positioning for the new macroeconomic regime of lower interest rates. The phenomenon is thus a shift from a market driven by anticipation to one driven by fundamentals.

The Narrative Resumes: The Great Pause of 2025 and the Echoes of a Pivot

After the rapid-fire succession of rate cuts to close out 2024, the market entered 2025 with a widespread expectation that the easing cycle would continue, albeit at a more measured pace. However, the Federal Reserve had other plans, initiating a prolonged “hawkish pause” that would define the first half of the year and set the stage for a familiar drama of data-driven speculation to unfold once again.

The Hawkish Pause: The Fed Holds Firm

Contrary to market expectations, the FOMC held the federal funds rate steady in its target range of 4.25% to 4.50% for five consecutive meetings in 2025: January, March, May, June, and July. This extended pause was initially justified by persistent inflation and surprisingly strong labor data early in the year. As the year progressed, the rationale shifted to a more cautious, data-dependent approach, with officials citing moderating economic activity but ongoing concerns about inflation, which was being fueled by new tariff policies.

This period of inaction revealed a growing rift within the committee. While the December 2024 decision saw a single dissent, the minutes from the July 2025 meeting showed that two governors, Michelle Bowman and Christopher Waller, dissented in favor of a quarter-point cut to protect a weakening job market. This dual dissent, the first of its kind since 1993, signaled that the internal consensus was fracturing and that the pressure to resume easing was building significantly.

Déjà Vu: A Weakening Labor Market Reignites Easing Bets

By late summer 2025, the narrative began to echo that of the previous year. A series of disappointing economic reports, particularly from the labor market, once again shifted market sentiment decisively. Labor Department data revealed weaker-than-expected hiring in July, a rising unemployment rate, and sharp downward revisions to previous job gains. This data provided a powerful counterargument to the Fed’s patient stance.

The market reaction was swift. By late August, fed funds futures were pricing in an 85% probability of a rate cut at the upcoming September meeting. All eyes turned to Chair Powell’s annual speech at the Jackson Hole Economic Symposium, which was widely interpreted as a signal that rate cuts were once again on the table. The “rumor” mill was back in full swing, with markets anticipating that the Fed, faced with deteriorating economic data, would be forced to pivot back to an easing policy.

Gold in 2025: A Rally on Dual Fronts

Gold’s performance in 2025 was even more robust than in 2024, driven by a powerful combination of factors. The year began with a surge in prices as investors sought a hedge against the economic uncertainty and potential inflation stemming from President Trump’s focus on tariffs. This safe-haven demand pushed gold through the $2,900/oz level in February and to a peak of $3,500/oz in April.

As the Fed’s hawkish pause continued through the summer, gold consolidated its gains. However, the market’s renewed speculation on rate cuts in late summer provided a second, powerful tailwind. In a direct parallel to the events of September 2024, the building anticipation of a September 2025 rate cut ignited another “rumor” rally. In early September 2025, gold prices once again surged, breaking above $3,500 and touching new highs near $3,600 per ounce. The rally was driven by the same fundamental principle: the expectation of falling interest rates reduces the opportunity cost of holding the non-yielding metal, making it a more attractive asset.

Underlying Drivers: A Holistic View of the Gold Market

While the Federal Reserve’s policy pivot was the dominant cyclical driver of gold prices in late 2024, a comprehensive analysis requires acknowledging other significant factors that shaped the market. The Fed’s actions did not occur in isolation; they interacted with broader financial conditions and a set of powerful, underlying structural trends that supported the gold market.

The U.S. Dollar and Yield Curve Dynamics

The relationship between interest rates, the U.S. dollar, and gold is complex. Typically, falling U.S. interest rates weaken the dollar, making dollar-denominated gold cheaper for foreign buyers and thus boosting its price. However, during this period, the dollar exhibited relative strength against other major currencies, partly due to slower economic growth in other regions like Europe. This relative dollar strength acted as a partial headwind, moderating what might have been an even more explosive rally in gold.

Furthermore, a critical nuance existed within the U.S. Treasury market. While the Fed was aggressively cutting the short-term federal funds rate, long-term Treasury yields actually rose during the fall of 2024. This occurred as the yield curve, which had been inverted for an extended period (a classic recession indicator), began to flatten and normalize. This meant that despite the Fed’s actions, overall financial conditions did not ease as dramatically as the headline rate cuts might suggest. This dynamic presented a more complex long-term outlook for gold, as higher long-term real yields can increase the opportunity cost of holding the non-yielding metal.

Structural Bullish Factors for Gold

The cyclical rally ignited by the Fed’s pivot was built upon a solid foundation of strong, structural demand for gold. These long-term trends provided a high floor for prices and explain why the “Sell the News” phase resulted in consolidation rather than a significant price collapse.

- Central Bank Diversification: A key structural theme in the 2020s has been the steady accumulation of gold by global central banks, particularly those in emerging markets. These institutions have been actively diversifying their foreign exchange reserves away from the U.S. dollar to reduce their exposure to U.S. economic and foreign policy. This consistent, non-speculative buying, which reportedly amounted to hundreds of tonnes in 2024, provided a powerful source of underlying demand throughout the period of the Fed’s pivot.

- Geopolitical Risk and Policy Uncertainty: The geopolitical landscape, combined with the uncertainty surrounding U.S. trade and tariff policy, created persistent safe-haven demand for gold. Investors globally sought refuge in gold as a hedge against international tensions and the potential for economic disruption stemming from unpredictable U.S. trade policies. This demand is largely independent of the interest rate cycle and adds to gold’s appeal as a portfolio diversifier.

- Investor Demand: Alongside institutional buying, demand from private investors remained robust. Strong inflows were observed into gold-backed Exchange-Traded Funds (ETFs), and demand for physical bars and coins was strong. This reflects a broad-based desire among investors to hold a tangible asset as a hedge against both the lingering risk of inflation and the emerging risk of an economic slowdown or recession.

The gold market rally of late 2024 was therefore the product of a perfect storm, where a powerful cyclical catalyst—the Fed’s dovish pivot—coincided with and amplified these pre-existing, strong structural drivers.

Conclusion: Synthesis and Forward Outlook

The period from late 2024 through mid-2025 marked a volatile and instructive chapter for U.S. monetary policy and global financial markets. The Federal Reserve’s actions—a decisive pivot followed by a prolonged pause—triggered significant repricing across asset classes, with the gold market exhibiting a particularly clear reaction. The events of this period confirm the durability of classic market behaviors while highlighting the complexities of the modern macroeconomic environment.

Astreka Findings

The analysis confirms that the Federal Reserve executed a 100-basis-point pivot in late 2024 in response to a cooling labor market. This was followed by a five-meeting pause in the first half of 2025 as the committee contended with persistent inflation, partly fueled by new tariff policies. By late summer 2025, a familiar pattern re-emerged, with weakening labor market data once again forcing the Fed to signal a likely resumption of its easing cycle.

Gold prices correlated strongly with these policy shifts, but the relationship was consistently anticipatory. In both 2024 and 2025, the most significant price appreciation occurred in the weeks leading up to expected rate cuts, as markets aggressively priced in the probability of future easing. This price action definitively validates the “Buy the Rumor, Sell the News” hypothesis. The rumor—the expectation of a Fed pivot solidified by weak economic data—drove powerful rallies to record highs. The news—the official announcements of the rate cuts—served as moments of consolidation and profit-taking. Gold’s rally in 2025 was further amplified by strong safe-haven demand related to trade and geopolitical uncertainty.

Implications for Investors

The key lesson from this period for investors is the critical importance of an anticipatory, forward-looking strategy when navigating monetary policy cycles. The highest returns were captured not by reacting to the Fed’s announcements, but by correctly identifying the economic conditions that would compel the central bank to alter its course. Success depended on analyzing the catalysts that shape expectations, such as key economic data releases, rather than trading the announcements that merely confirm them.

Furthermore, this episode reaffirmed gold’s essential role as a strategic asset. The metal proved to be an effective hedge against both the economic uncertainty that prompted the Fed’s actions and the geopolitical risks of the period. Its performance was bolstered by strong underlying structural demand from central banks and investors, demonstrating its dual function as both a cyclical trade and a long-term store of value.

Forward Outlook (as of Early September 2025)

As of September 2025, the market is once again on the cusp of a potential Fed rate cut. The focus has shifted from whether the Fed will resume easing to the pace and depth of the cycle ahead. Forecasts from major financial institutions project a continued, albeit gradual, series of rate cuts into 2026, with the federal funds rate expected to decline toward a range of 3.25% to 3.50%. This outlook suggests a continued supportive macroeconomic environment for gold. While the frantic, rumor-driven rallies may give way to more measured advances, the new regime of monetary accommodation, combined with persistent geopolitical uncertainty and the structural trend of de-dollarization, establishes a fundamentally bullish medium-term outlook for the precious metal