May 24, 2026

Quantum Computing Industry Report 2026

Quantum computing in 2026 is best described as an early-commercialization industry built on still-precarious physics and engineering. The field has moved well beyond laboratory curiosity: there are more than 40 commercially available QPUs globally, venture funding rebounded in 2024, corporate references to quantum are increasing, and more than 300 organizations are collaborating with quantum-technology vendors. But the core technical truth has not changed: today’s machines remain noisy, small in logical-qubit terms, and too fragile for broad, repeatable economic advantage across mainstream enterprise workloads. NIST still characterizes current systems as rudimentary and error-prone, while MIT’s Quantum Index and McKinsey both frame the sector as commercially promising but timing-uncertain. [1]

For investors, the industry is not yet in scaling mode. It is in a transition zone between research and commercialization. Annealing and hybrid quantum-classical workflows already generate some real revenue; cloud access, hardware-as-a-service, on-premise sovereign installations, quantum networking, and post-quantum cybersecurity are all monetizing now. By contrast, large-scale fault-tolerant gate-based quantum computing is still ahead of us. IBM’s public roadmap targets its first fault-tolerant system in 2029, while multiple rivals are only beginning to show early logical-qubit milestones rather than production-scale logical machines. [2]

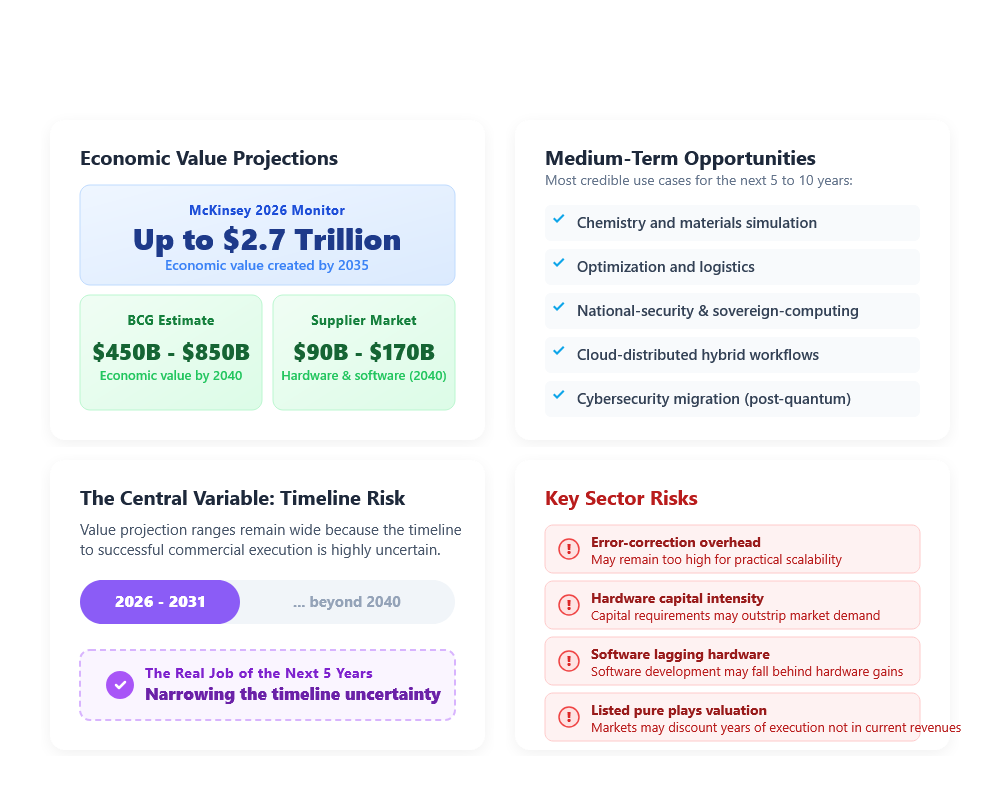

The opportunity is large enough to matter. McKinsey’s 2026 monitor says quantum computing could create up to $2.7 trillion of economic value by 2035, while BCG still estimates $450 billion to $850 billion of economic value by 2040 and a $90 billion to $170 billion supplier market for hardware and software providers by that point. Those ranges are wide because timeline risk is the sector’s central variable. Narrowing that uncertainty is the real job of the next five years. [3]

The biggest opportunities over the next five to ten years are concentrated in a few areas. The most credible medium-term use cases remain chemistry and materials simulation, optimization and logistics, national-security and sovereign-computing programs, cloud-distributed hybrid workflows, and cybersecurity migration to a post-quantum world. The biggest risks are equally clear: error-correction overhead may remain too high, the capital intensity of hardware programs may outstrip demand, software may lag hardware, and listed pure plays may already discount years of successful execution that are not yet visible in today’s revenues. [4]

A concise investor framing is below.

| Scenario | What has to go right or wrong | Investor implication |

|---|---|---|

| Bull case | Logical qubits scale faster than expected; trapped-ion, superconducting, neutral-atom, or photonic architectures cross from “demonstrations” to repeatable utility; government funding remains strong; enterprise buyers convert pilots into production; post-quantum security budgets pull adjacent revenue forward. | A handful of platform leaders and ecosystem enablers re-rate sharply upward, and the winning hardware stack captures outsized economic rents. [5] |

| Base case | Near-term revenue grows through cloud access, sovereign deployments, tools, and security, but broad fault-tolerant utility arrives later than the most aggressive roadmaps suggest. | Big tech and well-capitalized leaders win; many public pure plays remain tradable but volatile; returns hinge on milestone timing rather than near-term earnings. [6] |

| Bear case | Error correction proves much more expensive than expected; hardware advances remain impressive but commercially irrelevant; enterprise budgets shift back to classical AI/HPC; public-market valuations compress toward revenue reality. | Many pure plays underperform badly, while diversified incumbents absorb failed quantum optionality without major shareholder damage. [7] |

My bottom line as of late May 2026: the sector is investable, but mostly through quality filters. If an investor wants exposure, the highest-quality approach is still to own the companies with real balance sheets, broad ecosystems, and credible technical evidence. The pure plays can work, but only with explicit acceptance that these are milestone-driven venture-style equities rather than conventional growth stocks. That distinction matters more in quantum than in almost any other public technology sub-sector today. [8]

Technology foundations

What quantum computing is

Classical computers store information as bits that are either 0 or 1. Quantum computers store information in qubits, physical systems whose state is described by quantum mechanics. Unlike a classical bit, a qubit can exist in a combination of 0 and 1 until it is measured; multiple qubits can also become correlated in ways that have no classical analog. NIST’s plain-language summary is still the cleanest framing: quantum computers use the laws of physics at very small scales to process certain classes of problems in ways classical computers cannot efficiently emulate. [9]

A simple analogy helps, with one caution: analogies are directional, not literal. A classical bit is like a coin lying flat—heads or tails. A qubit is more like a spinning coin whose full state contains richer information than either heads or tails alone. Superposition is the spinning; interference is the ability to guide the spin so good answers reinforce and bad answers cancel; entanglement is when multiple spinning coins become linked such that describing one without the others becomes impossible. The analogy is imperfect, because real quantum states are complex amplitudes rather than fuzzy probabilities, but it is useful for investors deciding whether the technology is “more parallelism” or something fundamentally different. It is fundamentally different. [10]

Why quantum can outperform classical

Quantum computers do not replace classical computing. They are specialized coprocessors for certain classes of problems. Their long-term promise comes from the fact that the state space of a quantum system grows exponentially with qubit count, which can make some simulation, search, optimization, and algebraic tasks tractable in ways classical systems struggle to match. The most famous examples are Shor’s algorithm for factoring and discrete logs, and quantum simulation of molecules and materials. The practical question is not whether these algorithms exist on paper; it is whether hardware can execute them with enough logical fidelity to matter. That is where the industry remains constrained. [11]

Superposition, entanglement, interference, error correction

The four load-bearing ideas are straightforward in investor language.

| Concept | Plain-English explanation | Why investors should care |

|---|---|---|

| Superposition | A qubit can encode a weighted combination of basis states. | Potentially explores computational state spaces more efficiently than classical bits. [9] |

| Entanglement | The state of one qubit becomes inseparable from another. | Enables correlations and computational structures that classical machines must simulate expensively. [9] |

| Interference | Quantum algorithms amplify correct paths and suppress wrong ones. | This is where speedup comes from; a quantum computer is not “trying all answers at once” and magically reading them out. [9] |

| Error correction | Information from one logical qubit is spread across many physical qubits so noise can be detected and corrected. | Commercial viability depends on this. Without error correction, nearly every grand claim about chemistry, cryptography, or AI remains limited. [12] |

Error correction is the central bottleneck. Google’s Willow result is important because it showed a below-threshold surface-code demonstration in which larger error-corrected qubits improved rather than worsened. Microsoft and Quantinuum jointly created 12 logical qubits in 2024, while Microsoft and Atom Computing later reported 24 entangled logical qubits and computation on 28 logical qubits using neutral atoms. Those are meaningful milestones, but they are still far from the hundreds or thousands of logical qubits many practical applications require. [13]

Gate-based quantum computers versus quantum annealing

Gate-based systems are the quantum analog of general-purpose computers. They execute sequences of logic operations on qubits and, in principle, can run universal quantum algorithms. IBM, Google, Microsoft, IonQ, Rigetti, Quantinuum, Intel, Atom Computing, QuEra, Pasqal, and PsiQuantum are all pursuing gate-based or gate-based-compatible paths. [14]

Quantum annealing is different. It is purpose-built for optimization and related energy-minimization problems, rather than universal gate-model computation. D-Wave’s commercial systems are the leading annealing example, and its Advantage2 system with more than 4,400 qubits and 20-way connectivity is already in market. Annealing has much weaker claims for universal quantum advantage, but it has the strongest claim to near-term commercial relevance because customers can use it now for certain optimization tasks. D-Wave’s January 2026 acquisition of Quantum Circuits reflects its decision to add a gate-model path on top of annealing rather than rely on annealing alone forever. [15]

Why scaling is hard

Quantum computing is difficult to scale for reasons that are more brutal than most equity narratives admit. Qubits decohere when the environment “looks at” them. Control systems introduce crosstalk. Connectivity is imperfect. Readout is noisy. Cooling, lasers, electronics, and packaging become harder as systems grow. Even if physical-qubit counts rise quickly, the physical-to-logical conversion ratio can be punishing; Atom Computing’s 2025 white paper notes that one logical qubit may require anything from 10 to 1,000 physical qubits, depending on architecture and code assumptions. Nature warned in 2026 that the field needs more rigorous KPIs precisely because raw qubit count alone is too easy to game. [16]

The metrics that matter

For investors, the correct KPI set is broader than qubit count.

| Metric | What it means | Why it matters | Illustrative examples |

|---|---|---|---|

| Physical qubit count | Number of hardware qubits on the device. | Useful, but low-signal by itself. | IBM Heron 156 qubits; Google Willow 105 qubits; Rigetti Ankaa-3 84 qubits; Quantinuum H2-1 56 qubits; D-Wave Advantage2 4,400+ annealing qubits. [17] |

| Logical qubits | Error-corrected qubits built from many physical qubits. | The most important long-run metric. | Microsoft–Quantinuum 12 logical qubits; Microsoft–Atom 24 entangled logical qubits. [18] |

| Coherence time | How long a qubit keeps its quantum state. | Longer coherence supports deeper circuits. | NIST stresses coherence as foundational; AWS Ocelot reported bit-flip times approaching one second for cat-qubit elements with 20 microsecond phase-flip times. [19] |

| Gate fidelity / error rate | Probability that a quantum gate performs correctly. | Small improvements compound rapidly. | Quantinuum cites 99.921% average two-qubit fidelity on H2-1; Rigetti reports 99.5% median fSim fidelity; Google Willow reported mean simultaneous CZ error of about 0.33%. [20] |

| Quantum volume | A system-level benchmark combining count, fidelity, connectivity, and compiler performance. | Better than raw qubit count for broad comparability. | IBM defined the metric; Quantinuum reported quantum volume of 2^23 in 2025. [21] |

| CLOPS / speed metrics | How fast a system executes layers or circuits. | Determines practical throughput for hybrid workflows. | IBM has increasingly emphasized layer fidelity and speed rather than only raw QV. [22] |

The investor takeaway is simple: logical qubits, system fidelity, and application-specific throughput matter more than raw qubit counts. This is now a consensus view among the most credible industry observers, including Nature, IBM, and Quantinuum. [23]

Industry landscape

Market size, demand, and where value can accrue

The sector’s forecast range remains unusually wide, which is itself informative. McKinsey’s 2026 monitor estimates quantum computing could create up to $2.7 trillion in economic value by 2035. BCG’s more conservative long-range estimate still sees $450 billion to $850 billion of economic value globally by 2040, supporting a $90 billion to $170 billion supplier market. MIT’s 2025 Quantum Index found quantum-computing venture funding rebounded to $1.6 billion in publicly announced investment in 2024, with patent activity and corporate mentions also rising sharply. [24]

The right way to think about TAM is not as one monolithic “computer market.” It is a layered opportunity comprising hardware, cloud access, compilers, control systems, cryogenic and photonic subsystems, error-correction software, workflow orchestration, application software, consulting, and eventually vertical services in chemistry, logistics, finance, and defense. In the near term, the most monetizable layers are cloud access, quantum-ready software, sovereign installations, and security migration, not world-changing universal quantum compute sold by the rack. [25]

Commercial applications and adoption timeline

| Application area | Why quantum matters | Commercial status in 2026 | Likely timeline for meaningful value |

|---|---|---|---|

| Drug discovery | Molecular simulation and electronic-structure calculation are natural quantum targets. | Real partnerships exist, but production-grade advantage is still limited. Microsoft–Quantinuum demonstrated a chemistry workflow using logical qubits, AI, and HPC. IonQ cites AstraZeneca and pharmaceutical-type use cases. [26] | Late 2020s for narrow workflows; 2030s for broader impact. |

| Materials science | Battery chemistry, catalysts, superconductors, and advanced materials fit quantum simulation well. | One of the strongest long-term theses; still pre-broad-production. IBM, Google, and multiple startups position chemistry/materials as first-tier targets. [27] | Late 2020s to early 2030s. |

| Optimization and logistics | Routing, scheduling, portfolio optimization, supply chains. | Strongest current monetization for annealing and hybrid systems. D-Wave and IonQ both market here today. [28] | Now through 2030, mostly hybrid and domain-specific. |

| Financial modeling | Portfolio construction, risk, Monte Carlo acceleration, optimization. | Pilot-heavy; still evidence-light for broad superiority, but interest from JPMorgan and others remains material. [29] | Late 2020s for selected tasks; 2030s if FTQC arrives. |

| Cryptography / cybersecurity | Future fault-tolerant quantum systems could break widely used public-key cryptography; defensive migration is already underway. | This is happening now as a budget line item, even before cryptographically relevant quantum computers exist. [30] | Immediate on defense spending; offensive impact remains uncertain. |

| AI acceleration | Potential future gains in sampling, optimization, or model components. | Mostly experimental today; no evidence that quantum will accelerate frontier LLM training soon. NVIDIA, AWS, and D-Wave focus on hybrid workflows rather than pure quantum AI. [31] | 2030s for meaningful narrow applications. |

| Defense / intelligence | Secure communications, sensing, optimization, cryptanalysis, sovereign compute. | Already a major funding channel. IonQ won SDA HALO and MDA SHIELD-adjacent work; U.S. defense documents emphasize long-term military relevance. [32] | Now for R&D and procurement; later for operational compute. |

The current limitations preventing mass adoption are not mysterious. They include insufficient logical-qubit scale, high error-correction overhead, fragile hardware, expensive and specialized facilities, limited benchmark standardization, unclear software ROI for many enterprise workloads, and a shortage of quantum-skilled talent. Nature’s 2026 KPI article is especially important because it captures a genuine market problem: the field is producing milestones faster than it is producing apples-to-apples comparability. That tends to inflate hype cycles and punish uninformed capital. [33]

Government funding and geopolitical competition

Quantum is now an industrial-policy contest as much as a research contest.

| Region | What matters most in 2026 | Funding / policy signal | Strategic read |

|---|---|---|---|

| United States | Strongest commercial vendor base, deepest big-tech stack, strongest cloud ecosystem. | The National Quantum Initiative continues to coordinate federal R&D, and Reuters reported a new $2 billion U.S. investment across nine quantum firms in May 2026, including a $1 billion IBM-linked foundry venture. [34] | The U.S. still leads in commercialization quality and ecosystem depth. |

| China | Massive state backing, centralized coordination, strong publication output, opacity around true capability. | MERICS and Belfer both cite Chinese government quantum investment at roughly $15 billion, significantly above Western public-sector norms. [35] | China is the main geopolitical challenger, especially in state-directed scaling and secure communications. |

| European Union | Strong research base, cross-border infrastructure, sovereign-HPC integration. | The Quantum Flagship carries an expected €1 billion budget; EuroHPC had procured six quantum computers across Europe by April 2026. [36] | Europe is building sovereign hybrid HPC-plus-quantum infrastructure rather than betting on one national champion. |

| Canada | Deep research heritage and startup density. | Canada’s National Quantum Strategy allocates C$360 million in dedicated funding, with Budget 2025 adding further support. [37] | Canada punches above its weight through ecosystem quality and commercialization support. |

| Japan | Long-duration national planning and HPC/industrial integration. | Moonshot Goal 6 explicitly targets a fault-tolerant universal quantum computer by 2050, while SIP3 quantum is aimed at social implementation. [38] | Japan is patient capital in policy form: slower headlines, serious strategic intent. |

The geopolitics matter for investors because sovereign demand may be the first reliable buyer of expensive systems. Commercial demand is still variable; national-security demand is becoming structural. That is one reason the most credible companies increasingly pair technical milestones with sovereign manufacturing, domestic foundry plans, export-control relevance, and defense partnerships. [39]

Competitive landscape and technical deep dive

Major-company comparison

The table below blends public technical evidence with investor judgment. “Technological lead” is necessarily subjective and should be read as a relative, evidence-based assessment, not an official ranking.

| Company | Technology approach | Hardware type | Technological lead | Partnerships / distribution | Revenue model | Funding strength | Main advantages | Main weaknesses | Sources |

|---|---|---|---|---|---|---|---|---|---|

| IBM | Gate-based, modular FT roadmap | Superconducting | Top tier | IBM Quantum Network, cloud, enterprise relationships | Cloud access, services, ecosystem lock-in | Very strong | Deep enterprise sales, roadmap credibility, fabrication and systems depth | Quantum revenue is tiny inside IBM; execution must match 2029 roadmap | [40] |

| Gate-based with surface-code emphasis | Superconducting | Top tier | Internal research + cloud adjacency | Strategic R&D inside Alphabet | Very strong | Strong science bench; Willow below-threshold milestone is one of the most important error-correction results in the field | Limited stand-alone commercialization versus IBM/AWS/Azure | [41] | |

| Microsoft | Azure quantum stack plus hardware bets | Neutral atom via Atom alliance; topological internal program | Top tier on software/orchestration; high-variance on hardware | Quantinuum, Atom Computing, Azure | Cloud platform, software, orchestration | Very strong | Best enterprise distribution with Azure; real logical-qubit milestones via partners | Majorana 1 is promising but not yet de-risked enough to underwrite as core thesis | [42] |

| IonQ | Modular trapped-ion roadmap, networking, sensing, security | Trapped ions | Upper tier among public pure plays | AWS, Azure, Google Cloud, sovereign deals | Cloud access, systems sales, platform services | Strong among pure plays | Best balance sheet in public quantum; diversified quantum platform; strong commercial momentum | Valuation extremely demanding; roadmap claims are aggressive | [43] |

| Rigetti | Full-stack gate-based quantum | Superconducting | Mid tier | AWS, Azure, government, India C-DAC | QCaaS, QPUs, system sales | Improved | Own fab, fast gates, chiplet roadmap, government support | Very small revenue base; still far behind IBM/Google on scale and visibility | [44] |

| D-Wave | Annealing today, gate-model optionality after QCI acquisition | Annealing plus superconducting gate-model path | Leader in annealing; uncertain in universal QC | Enterprise and sovereign customers | Systems, QCaaS, hybrid optimization software | Improved | Only major annealing company with real commercial traction and large installed usage | Annealing is not universal QC; revenue still lumpy; investor confusion remains high | [15] |

| PsiQuantum | Fault-tolerant-first architecture | Photonic | High-upside private leader | GlobalFoundries, Chicago, Australia, DARPA evaluation | Ultimately systems and infrastructure | Very strong private backing | Photonics plus semiconductor-manufacturing thesis is one of the cleanest scale stories | Timelines are highly ambitious and still largely unproven at system level | [45] |

| Quantinuum | Full-stack trapped-ion plus software | Trapped ions | Likely current performance leader | Microsoft, JPMorgan, Amgen, BMW | Cloud, software, HaaS, applications | Very strong private backing | World-leading fidelity/QV, meaningful logical-qubit results, full-stack software | Revenue still small relative to valuation; trapped-ion gate speeds remain slower | [46] |

| Intel | Research-led scaling thesis | Silicon spin qubits | Research option | National labs and academic partners | Primarily R&D/IP today | Strong corporate parent, limited strategic urgency | CMOS compatibility and industrial fabrication know-how are real assets | Commercial progress is much earlier than leading platforms | [47] |

| Amazon | Cloud marketplace plus internal research | Braket marketplace; superconducting/cat-qubit Ocelot research | Platform leader, hardware optionality | Braket partners across modalities | Cloud service, workflow tools | Very strong | Best neutral marketplace model; Ocelot is a credible internal hardware signal | No public evidence yet of leadership in production-scale gate-model hardware | [48] |

| NVIDIA | Quantum-adjacent enabling stack | Simulation, control, hybrid orchestration | Infrastructure leader, not QPU leader | CUDA-Q, DGX Quantum, NVQLink, multiple QPU partners | Software, accelerators, control-stack leverage | Very strong | Could capture value regardless of winning qubit modality | Does not own the core QPU hardware race | [49] |

Most promising startups and likely acquisition targets

Among the private names with the strongest public evidence, Quantinuum, PsiQuantum, QuEra, Atom Computing, and Pasqal stand out. Quantinuum looks like the most mature private full-stack operator today; PsiQuantum has the largest photonic ambition and enormous capital backing; QuEra and Atom Computing give neutral atoms the strongest case for a fast rise into the top tier; Pasqal is emerging as a sovereign-EU neutral-atom infrastructure player through actual on-site deployments. [50]

The most plausible acquisition targets are not necessarily the flashiest hardware vendors. In my view, the most strategic M&A targets over the next five years are likely to be control-stack, compiler, and error-correction companies, because they can slot into hyperscaler, defense, and semiconductor roadmaps without requiring a winner-take-all bet on one qubit modality. Public evidence for that thesis is indirect rather than explicit, so I would treat it as a strategic inference, not a consensus fact. The D-Wave/Quantum Circuits transaction is already a concrete example of how hardware players are buying missing pieces rather than relying on internal development alone. [51]

Which modalities look strongest

No single modality has won. That is the clearest sign the industry is still young.

| Modality | Core strengths | Core weaknesses | Commercial viability in 2026 | Estimated path to fault tolerance |

|---|---|---|---|---|

| Superconducting qubits | Fast gates; strongest semiconductor-tooling ecosystem; most developed big-tech roadmaps | Heavy cryogenic and wiring burden; crosstalk; scaling control complexity | High | Best-funded short path, with IBM targeting 2029 and Google already showing below-threshold surface-code progress. [52] |

| Trapped ions | Excellent coherence and fidelity; often all-to-all connectivity; strongest commercial logical-qubit evidence today | Slower gates; laser/control complexity | High | Best risk-adjusted current modality for near-term logical-qubit credibility. [53] |

| Photonic | Natural for networking; compatible with semiconductor manufacturing; room-temperature optical components in parts of stack | Photon loss, source/detector complexity, difficult full-stack integration | Medium, but promising | Very high upside, high execution risk. PsiQuantum is the flagship thesis. [54] |

| Neutral atoms | Massive qubit arrays; identical qubits by nature; strong scaling story; room-temperature surroundings for some subsystems | Laser complexity; control and fidelity are improving but still maturing | Rising fast | Most underappreciated challenger after trapped ions and superconducting. [55] |

| Topological qubits | In theory, lower error rates and lower correction overhead | Experimental validation remains incomplete | Low today | Potentially transformative, but too early to underwrite aggressively. [56] |

| Silicon spin qubits | CMOS compatibility and density | Immature commercial stack; readout/control challenges | Early | Longer-dated option, probably a 2030s story. [47] |

If forced to choose one modality for a risk-adjusted five-year investment view, I would pick trapped ions. The reason is not ideology; it is evidence. Quantinuum has the best public performance claims on fidelity and quantum volume, Microsoft–Quantinuum delivered logical-qubit results, and IonQ has paired trapped ions with the strongest public-company commercial balance sheet. If forced to choose one modality for a manufacturing-scale 10- to 15-year moonshot, I would say the answer is still open among superconducting, neutral atom, and photonic approaches. That is why diversified exposure often beats pure hardware purity for most investors. [57]

Public equities and investment analysis

Fundamental snapshot of the main public stocks

The table below mixes reported financials with approximate late-May-2026 market values. Market caps and ownership percentages change daily; they should be read as directional, not immutable.

| Company | Ticker | Approx. market cap | Latest reported revenue growth | Cash position | Profitability snapshot | R&D spending snapshot | Ownership snapshot | Valuation read | Competitive moat | Key catalysts | Key risks | Sources |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| IonQ | IONQ | ~$23–24B | +755% YoY in Q1 2026; FY2026 guide $260M–$270M | $3.1B | Q1 GAAP net income was driven by a large non-cash warrant gain; core operations remain loss-making | FY2025 R&D $305.7M | Institutions 41.42%; insiders 5.20% | Extremely rich; by guide, roughly ~80x+ market cap / 2026 sales | Strongest pure-play balance sheet, cloud distribution, platform breadth | Large system sales, SkyWater integration, sovereign contracts, networking/security expansion | Valuation, execution risk, dilution risk via M&A, roadmaps may outrun delivery | [58] |

| Rigetti | RGTI | ~$8–9B | ~+199% YoY in Q1 2026 | $569.0M and no debt | Q1 net income was helped by non-cash warrant gains; operations remain sharply loss-making | Q1 2026 R&D $20.0M | Institutions 35.38%; insiders 1.60% | Very rich versus revenue; annualized Q1 sales imply triple-digit sales multiple | Own fab, superconducting expertise, chiplet roadmap | India 108-qubit system sale, U.S. Commerce LOI for up to $100M, 100+ qubit roadmap | Tiny revenue base, capital intensity, high volatility, technology-gap risk | [59] |

| D-Wave | QBTS | ~$8–9B | Q1 2026 revenue down 81% YoY, but bookings up 1,994% | $588.4M | Net loss $18.4M in Q1 2026 | Q1 2026 R&D $25.8M | Institutions 42.47%; insiders 3.20% | Rich on present revenue, but improved if bookings convert | Only scaled commercial annealing platform; hybrid optimization credibility | Bookings conversion, Advantage2 deployments, gate-model progress via QCI | Annealing may remain niche; revenue lumpiness; acquisition-integration risk | [60] |

| IBM | IBM | ~$235–240B | Q1 2026 revenue +9% YoY | $11.8B cash, restricted cash, and marketable securities | Profitable and cash-generative | Q1 2026 R&D $2.17B; FY2025 $8.32B | Institutions 58.96%; insiders 0.27% | Reasonable versus pure plays; quantum optionality is not the main valuation driver | Deep enterprise moat, installed base, roadmap credibility, sovereign support | 2029 FT roadmap milestones, Anderon foundry venture, enterprise AI + quantum stack | Quantum may stay too small to move the needle financially for years | [61] |

| Alphabet | GOOGL | ~$4–5T | Q1 2026 revenue +22% YoY | $126.8B cash and marketable securities | Strongly profitable | Q1 2026 R&D $17.0B | Institutions 40.03%; insiders 11.61% | Premium but supported by massive cash generation | Google Research, AI-HPC scale, quantum science bench | Further Willow-class breakthroughs; cloud commercialization | Quantum remains non-material financially; antitrust and AI competition dominate valuation | [62] |

| Microsoft | MSFT | ~$3.1T | FY26 Q3 revenue +18% YoY | $78.3B cash, equivalents, and short-term investments | Strongly profitable | FY26 Q3 R&D $8.9B | Institutions 71.13%; insiders 0.03% | Premium, but quantum optionality is largely “free” inside broader AI/cloud story | Azure distribution, orchestration layer, partner ecosystem | Atom/Quantinuum logical-qubit scaling, Azure monetization | Hardware modality uncertainty; quantum immaterial to near-term earnings | [63] |

| NVIDIA | NVDA | ~$5.4T | Q1 FY2027 revenue +85% YoY | $80.6B cash plus marketable securities and equity securities | Exceptionally profitable | Q1 FY2027 R&D $6.32B | Institutions 65.27%; insiders 4.17% | Rich, but execution supports premium | Owns the AI/HPC control plane that quantum will likely need | CUDA-Q and NVQLink adoption; more partnerships; hybrid quantum-AI workflows | Quantum hardware makers may capture less value than enablers hope; AI cycle risk dominates | [64] |

Stock-by-stock outlook

IonQ

Short-term outlook: constructive, but valuation-dependent. IonQ has the strongest pure-play commercial story in public markets right now: Q1 2026 revenue of $64.7 million, raised full-year guidance to $260 million to $270 million, a first 256-qubit system sale, and a very large $3.1 billion cash and investments balance. That combination is rare. [65]

Long-term outlook: one of the highest-upside public names if its modular trapped-ion roadmap and platform expansion into networking, sensing, and security execute. The balance sheet gives IonQ time that peers do not have. But the stock already prices in a lot of future perfection. [66]

Risk rating: high.

Speculative potential: very high.

My probability of long-run success: 55% as a relevant independent quantum platform; lower for justifying today’s valuation from fundamentals alone. This is an analyst estimate, not a consensus statistic.

Rigetti

Short-term outlook: tradable, not investment-grade in the classic sense. Q1 2026 revenue grew sharply to $4.4 million; the balance sheet improved materially to $569 million cash/investments; and the U.S. government LOI for up to $100 million plus the India 108-qubit order are meaningful validating events. [67]

Long-term outlook: plausible survival and relevance, but not yet a clear lead candidate. Rigetti’s chiplet architecture and own-fab advantage are real, yet it trails IBM and Google in scale and credibility. [68]

Risk rating: very high.

Speculative potential: very high.

My probability of long-run success: 30% as an independent significant winner; 50%+ probability of remaining strategically relevant in some form, including partnership-heavy or M&A-led outcomes. This is an analyst estimate.

D-Wave

Short-term outlook: mixed but improving. On pure revenue, Q1 2026 looked weak; on bookings, it looked excellent. That divergence is exactly why D-Wave is difficult for the general market to price. The installed annealing business is real; the gate-model roadmap is interesting but unproven. [69]

Long-term outlook: more attractive than many skeptics assume if one accepts that not all quantum value must come from universal gate-model systems. D-Wave can remain relevant even if annealing never becomes the dominant modality, because optimization and hybrid workflows have paying customers now. [70]

Risk rating: very high.

Speculative potential: high.

My probability of long-run success: 40% as a meaningful niche or dual-platform winner. This is an analyst estimate.

IBM

Short-term outlook: attractive for conservative investors who want quantum exposure without balance-sheet drama. IBM’s quantum optionality is backed by a profitable business, a credible roadmap, and growing sovereign support. [71]

Long-term outlook: one of the best risk-adjusted quantum investments in public markets. If IBM hits its 2029–2033 roadmap, the market may start re-rating quantum optionality more seriously; if it misses, the downside for shareholders is still cushioned by the rest of the business. [72]

Risk rating: medium.

Speculative potential: moderate.

My probability of long-run quantum success: 70% that IBM remains a top-tier quantum platform, though the shareholder payoff may unfold more slowly than enthusiasts want. This is an analyst estimate.

Alphabet

Short-term outlook: positive for the business, neutral for a pure quantum thesis. Willow is scientifically important, but quantum remains a small part of the Alphabet story relative to AI, ads, cloud, and regulation. [73]

Long-term outlook: very strong as a scientific optionality vehicle. If superconducting fault tolerance arrives, Google is likely to be one of the winners. If not, shareholders still own an extremely powerful AI, cloud, and advertising compounder. [73]

Risk rating: medium.

Speculative potential: moderate.

My probability of long-run quantum success: 65% that Alphabet remains one of the scientific leaders; lower that quantum materially drives stock performance in the next five years. This is an analyst estimate.

Microsoft

Short-term outlook: positive. Microsoft may have the best public-market “barbell” in quantum: partner-driven logical-qubit progress today, topological optionality tomorrow, and Azure monetization in between. [74]

Long-term outlook: among the best long-duration quantum holdings for institutional investors. Azure distribution, orchestration software, HPC integration, and multi-modal partnering make Microsoft less dependent on guessing the single winning hardware stack. [75]

Risk rating: medium-low.

Speculative potential: moderate.

My probability of long-run quantum success: 75% that Microsoft captures meaningful value somewhere in the stack, even if not through its own topological hardware. This is an analyst estimate.

NVIDIA

Short-term outlook: strong, though quantum is not the primary reason to own it. NVIDIA is becoming the compute-control layer for hybrid quantum-classical workflows, and that is a strategically valuable position even if it never manufactures a QPU. [76]

Long-term outlook: one of the lowest-risk ways to benefit from quantum adoption, because almost every serious quantum workflow will require substantial classical acceleration, simulation, calibration, and orchestration. If quantum succeeds, NVIDIA likely participates; if it stalls, NVIDIA still has the dominant AI/HPC story. [77]

Risk rating: medium.

Speculative potential: moderate.

My probability of long-run quantum relevance: 80% at the infrastructure layer. This is an analyst estimate.

Best ideas, valuation calls, and hype filter

The easiest conclusions are also the most defensible.

| Category | My view |

|---|---|

| Best pure-play quantum stock | IonQ, because it combines the strongest public-company balance sheet, fastest reported commercial momentum, and a broader platform story than “compute only.” [65] |

| Best big-tech quantum exposure | Microsoft for risk-adjusted exposure; IBM for direct quantum purity inside a profitable incumbent; NVIDIA for picks-and-shovels exposure. [78] |

| Most overvalued on current fundamentals | Rigetti and D-Wave, followed by IonQ. The issue is not that they are bad companies; it is that current revenues are tiny relative to market value. [79] |

| Most undervalued quantum exposure | IBM. Quantum optionality is meaningful, but the stock is still primarily priced off software, infrastructure, consulting, and cash flow. [80] |

| Likely hype versus real technical leadership | Real technical leadership today looks strongest at Quantinuum, IBM, Google, and the Microsoft partner ecosystem, with IonQ strongest among public pure plays. Higher-hype areas include any valuation that assumes rapid mass-market adoption before logical-qubit economics are proven. [81] |

AI convergence and the skeptical case

What AI and quantum can realistically do for each other

The most realistic AI-plus-quantum story is not “quantum computers train giant AIs soon.” It is the opposite: AI and accelerated classical computing are likely to make quantum hardware more useful before quantum hardware makes AI dramatically faster. NVIDIA’s CUDA-Q and NVQLink efforts are explicitly built around hybrid orchestration across CPU, GPU, and QPU resources. D-Wave is integrating machine learning into hybrid solvers. Microsoft and Quantinuum already demonstrated a chemistry workflow that combined logical qubits, AI, and HPC. [82]

That means AI can help with calibration, pulse optimization, noise characterization, compiler optimization, experiment scheduling, and error decoding—all areas where large amounts of messy system data need fast pattern recognition. In other words, AI may be the thing that makes early quantum hardware less frustrating, rather than quantum being the thing that suddenly makes large AI models cheap. [31]

Quantum acceleration of AI is still mostly a long-horizon optionality story. The most credible future pathways are likely in sampling-heavy subroutines, certain optimization kernels, and scientific ML workflows rather than general-purpose frontier model pretraining. That is an inference from current hardware limits and available commercial messaging, not a settled consensus. The hype level here remains high relative to the evidence. [83]

Why the skeptical view deserves respect

Skeptics are not saying quantum mechanics is false; they are saying commercial timelines are often oversold. That skepticism is credible. Scientific American described 2026 as a make-or-break period for the field. Nature argued that stronger KPIs are needed to distinguish genuine advances from spurious or over-interpreted claims. And the MIT-linked timeline material notes that many academics still see the commercialization potential of NISQ-era systems as far from clear, especially in highly promoted areas such as finance and machine learning. [84]

The hardest skeptical arguments are economic, not philosophical. Even if the physics works, the industry may still disappoint investors if useful applications arrive too late, require too much capital, or accrue mostly to governments and hyperscalers rather than to small independent vendors. Quantinuum’s IPO filing is an emblematic example: impressive technical reputation, but 2025 revenue of only $30.9 million against a $10 billion private valuation and IPO talk as high as $15 billion to $20 billion. That gap between technical stature and current revenue is not unique. It is the sector’s defining financial issue. [85]

Energy and infrastructure are concerns, but investors should be precise about them. The bigger issue is not that quantum will necessarily consume more energy than AI data centers in aggregate; it is that leading architectures demand specialized physical infrastructure—cryogenics, lasers, vibration isolation, custom packaging, photonic components, or quantum networking gear—which raises total cost of ownership and slows deployment. Even architectures with lighter utility burdens still require floor space, integration, networking, and local support. [86]

The skeptical investment conclusion is not “avoid everything quantum.” It is simpler: pay for evidence, not aspiration. In this sector, valuations can move years ahead of revenues. That is exactly why diversified exposure and milestone-based discipline matter so much. [87]

Outlook and investment conclusions

Forecasts for 2030, 2035, and 2040

The most useful forecast format is probabilistic rather than categorical.

| Year | My base-case forecast | Probability estimate | Industries most likely to feel impact first |

|---|---|---|---|

| 2030 | A few vendors operate early fault-tolerant or quasi-fault-tolerant systems with tens to low hundreds of logical qubits; annealing and hybrid optimization are commercially normal; post-quantum security spending is large and unavoidable. | 35% probability of genuinely useful fault-tolerant systems for narrow workloads; 70% probability of meaningful commercial quantum revenue growth without broad FTQC. | Cybersecurity, defense, optimization, chemistry R&D. |

| 2035 | At least one architecture supports repeatable fault-tolerant workflows with real scientific or industrial value; market leadership narrows from many modalities to a smaller top cohort. | 60% probability of meaningful fault-tolerant commercial systems; 30% probability of still-fragmented, limited utility. | Materials, pharma, sovereign compute, selected finance workflows, industrial optimization. |

| 2040 | The sector either becomes an established strategic-compute layer or settles into a narrower but still valuable specialized market. The supplier market could plausibly fall somewhere inside BCG’s wide range. | 75% probability that quantum is commercially significant in at least a few industries; 25% probability that it remains important but more limited than current hype suggests. | Chemistry, materials, security, national infrastructure, advanced manufacturing, selected AI/HPC co-processing. |

Those probabilities are my own estimates, but they are grounded in public roadmaps, current logical-qubit progress, and the unusually wide forecast bands from McKinsey and BCG. [88]

Which companies are most likely to survive and dominate

I expect the long-term quantum market to be concentrated but not fully winner-take-all. Hardware may have a few leaders, but the total value stack will likely support separate winners in cloud distribution, orchestration, error correction, vertical software, and sovereign manufacturing.

My current probability-weighted view is:

- Most likely long-term platform leaders: IBM, Microsoft, Quantinuum, Google. [89]

- Most likely infrastructure/enabler leader: NVIDIA. [90]

- Most likely public pure-play survivor with premium optionality: IonQ. [65]

- Most interesting private moonshot: PsiQuantum. [91]

- Most underappreciated modality challengers: Atom Computing and QuEra in neutral atoms. [92]

Ranked list of the top quantum investments

This ranking is for an intelligent investor balancing technology quality, market structure, and valuation discipline.

| Rank | Investment | Why it ranks here |

|---|---|---|

| Microsoft | Best risk-adjusted mix of Azure distribution, partner ecosystem, logical-qubit progress, and low downside from quantum underperformance. [74] | |

| IBM | Best direct quantum exposure inside a profitable incumbent; roadmap and sovereign support are unusually credible. [93] | |

| NVIDIA | Best picks-and-shovels quantum exposure through the hybrid compute stack. [94] | |

| Alphabet | Exceptional scientific optionality, though quantum is still a side story relative to AI and ads. [73] | |

| IonQ | Best public pure play, but only for investors who can tolerate venture-like volatility and valuation risk. [65] | |

| D-Wave | Better near-term commercial evidence than many rivals, but architecture and valuation both complicate the thesis. [95] | |

| Rigetti | Highest beta among the named public names; real upside, but hardest to justify fundamentally today. [96] |

Conservative and aggressive strategy examples

A conservative strategy should assume that quantum value accrues slowly and unevenly. In that framework, I would emphasize diversified incumbents with real quantum optionality:

| Conservative model portfolio | Weight |

|---|---|

| Microsoft | 30% |

| IBM | 25% |

| NVIDIA | 25% |

| Alphabet | 15% |

| IonQ | 5% |

That portfolio treats quantum as a meaningful upside call option, not as the sole investment case. Its logic is that if fault tolerance slips, the portfolio still owns businesses with dominant positions in AI, cloud, enterprise software, and infrastructure. [97]

An aggressive / speculative strategy can own pure-play convexity, but it should still be balanced by at least one enabler:

| Aggressive model portfolio | Weight |

|---|---|

| IonQ | 30% |

| Rigetti | 15% |

| D-Wave | 15% |

| IBM | 15% |

| NVIDIA | 15% |

| Microsoft | 10% |

That mix is appropriate only for investors who understand that these are effectively public venture bets. A bad quarter or delayed technical milestone can cut these names dramatically even if the long-term thesis survives. [98]

What to monitor every quarter

The right leading indicators are not generic software KPIs. They are a mixture of technical and commercial evidence.

| Indicator | Why it matters |

|---|---|

| Logical-qubit count and quality | This is the bridge from science project to useful machine. [18] |

| Two-qubit fidelity and error suppression | Small improvements compound into much deeper usable circuits. [20] |

| Backlog / RPO / bookings | Sector revenue is lumpy; order quality matters. IonQ and D-Wave both show why. [99] |

| Cash burn versus runway | Most pure plays are still pre-profit economically. [100] |

| Government awards and sovereign deployments | These are becoming the cleanest non-hype demand signal. [101] |

| Independent benchmarks, not just company claims | Nature’s warning on KPI inflation should be taken seriously. [102] |

| Evidence of production workflows | Especially chemistry, optimization, and security use cases that survive outside press releases. [103] |

Open questions and limitations

Some parts of the sector remain difficult to compare cleanly because benchmarking is not yet standardized, private-company financial disclosure is sparse, and public-market valuations can change materially week to week. That matters especially for current market-cap snapshots and for any claim of “technology lead” across different modalities. Where possible, I have used official company disclosures, major research or government sources, and recent Reuters or equivalent reporting; where I have given probabilities or rankings, those are explicitly my own analytical judgments rather than established market consensus. [104]

The final investment conclusion is straightforward: quantum computing is real, but the market is still pre-separation between enduring winners and expensive stories. Investors should resist the temptation to confuse spectacular science with near-term shareholder value. If you want upside with survivability, own the incumbents and enablers first. If you want venture-style convexity, IonQ is the cleanest public expression today. Everything else in public pure-play quantum should be sized as speculation, not as certainty. [105]

navlistRecent quantum industry developmentsturn13news18,turn11news38,turn13news31,turn30news22,turn40news28,turn40news29

- [1][9][10][11] NIST – Quantum Computing Explained

- [2][5][52][72][89][93] IBM Quantum Roadmap

- [3][4][6][24][27][88] McKinsey Quantum Technology Monitor 2026

- [7][23][33][87][102][104] Nature – Quantum Computing Article

- [8][32][58][65][66][98][99][100][105] SEC Filing – IonQ Exhibit 99.1

- [12][13][41][73] Google Research – Making Quantum Error Correction Work

- [14][17][40] IBM Quantum Hardware

- [15] D-Wave Advantage2 Processor Milestone

- [16][19] NIST Q&A on Quantum Computing

- [18][26][74][75][78][97][103] Microsoft & Quantinuum Logical Qubits Breakthrough

- [20][46][53][57][81] Quantinuum 56-Qubit Quantum Computer Launch

- [21][22] IBM Quantum Layer Fidelity Metric

- [25][48] AWS Braket

- [28][60][69][95] D-Wave Q1 2026 Results

- [29] BCG – Quantum Computing

- [30] Barron’s – Quantum Computing Cybersecurity Risk

- [31][49][76][77][82][83][90][94] NVIDIA CUDA-Q

- [34] National Quantum Initiative Annual Report FY2025

- [35] MERICS – China’s Quantum Technology Strategy

- [36] EU Quantum Technologies Flagship

- [37] Canada’s National Quantum Strategy

- [38] Japan Moonshot Goal 6 – Quantum Technologies

- [39][101] Reuters – US Quantum Computing Investment

- [42][56] Microsoft Majorana 1 Quantum Processor

- [43] IonQ Roadmap

- [44][68] Rigetti 84-Qubit Ankaa 3 Launch

- [45][54] PsiQuantum

- [47] Intel Quantum Computing Chip Research

- [50][85] Reuters – Quantinuum IPO Filing

- [51] D-Wave Acquires Quantum Circuits

- [55] Atom Computing

- [59][67][79][96] Rigetti Q1 2026 Financial Results

- [61][71][80] IBM First Quarter 2026 Results

- [62] Alphabet SEC Filing Q1 2026

- [63] Microsoft FY2026 Q3 Income Statements

- [64] NVIDIA SEC Filing 2026

- [70] D-Wave Quantum Systems

- [84] Scientific American – Quantum Computing’s Make-or-Break Moment

- [86] arXiv Quantum Computing Paper

- [91] PsiQuantum $1B Fundraise

- [92] Microsoft & Atom Computing Quantum Machine