July 22, 2025

Cash-Secured Puts: A Guide to Income and Stock Buying

Introduction

In the landscape of modern investment strategies, the cash-secured put (CSP) stands out as a versatile and disciplined tool for the discerning investor. Often misunderstood as a purely speculative maneuver, a properly executed cash-secured put is, in fact, a conservative options strategy designed to achieve one of two distinct and often complementary objectives: generating a consistent income stream from cash reserves or acquiring a desired stock at a price below its current market value. It is a strategy built on patience, allowing an investor to be compensated for their willingness to purchase a quality asset at a predetermined, favorable price.

This report provides an exhaustive analysis of the cash-secured put, tailored for the investor who possesses a foundational understanding of market principles and seeks to integrate more sophisticated, income-oriented techniques into their portfolio. The analysis will deconstruct the strategy’s core mechanics, rigorously evaluate its risk and reward profile, and define the optimal conditions for its deployment. The core philosophy of the investor employing this strategy is a critical starting point; success is predicated on the understanding that both primary outcomes, whether the option expires worthless or results in the purchase of the stock, are considered acceptable and align with a pre-established financial goal. This pre-commitment to either outcome is the strategy’s defining characteristic, transforming what could be a speculative bet into the methodical execution of a deliberate acquisition or income plan.

Moving from foundational principles to practical application, this report will offer detailed guidance on the critical parameters of trade selection, including the choice of the underlying asset, strike price, and expiration date. It will provide a comparative framework, positioning the cash-secured put against related strategies like the covered call and the high-risk naked put. Through a detailed, data-driven case study on a well-known equity, the report will illustrate the strategy’s real-world dynamics across various market scenarios. Finally, it will explore the strategy’s role within the more advanced “Wheel” methodology and conclude with a crucial examination of the tax implications for U.S. investors, providing the comprehensive knowledge necessary to move from theory to confident and informed application.

Deconstructing the Cash-Secured Put: Core Principles and Mechanics

Defining the Strategy: From Obligation to Opportunity

At its most fundamental level, a cash-secured put is an options strategy in which an investor sells (or “writes”) a put option contract while simultaneously setting aside sufficient cash in their brokerage account to purchase the underlying stock at the agreed-upon price if the option is exercised by the buyer. A standard options contract typically represents 100 shares of the underlying security.

The transaction creates a distinct set of rights and obligations. The buyer of the put option pays a premium for the right, but not the obligation, to sell the underlying stock to the writer at a specified price, known as the strike price, on or before a specified expiration date. Conversely, the seller of the put option receives the premium and, in exchange, accepts the obligation to buy the underlying stock at that strike price if the buyer chooses to exercise their right. The “cash-secured” component is the defining feature that ensures the seller can fulfill this obligation without resorting to margin or leverage, thereby fundamentally altering the risk profile of the position.

The Anatomy of the Trade: Seller, Buyer, Premium, and Collateral

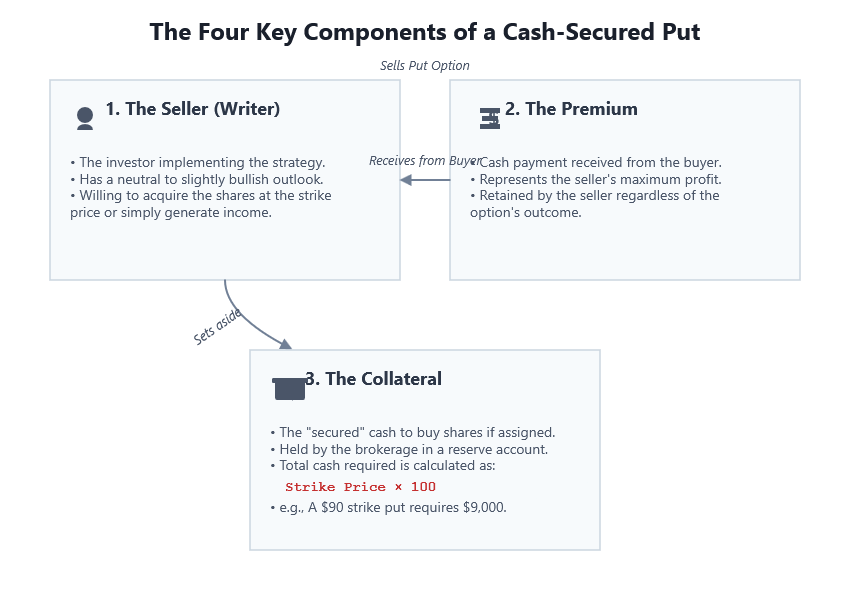

Executing a cash-secured put involves four key components:

- The Seller (Writer): This is the investor implementing the strategy. This individual typically has a neutral to slightly bullish long-term outlook on the underlying stock and is willing to either acquire the shares at the strike price or simply generate income from the premium.

- The Premium: This is the cash payment the seller receives from the buyer at the time the put option is sold. This premium represents the seller’s maximum potential profit on the options position and is retained by the seller regardless of whether the option is ultimately exercised or expires worthless.

- The Collateral: The “secured” cash is the total amount required to purchase the shares if assigned. This amount is calculated as the strike price multiplied by the number of shares in the contract (typically 100). Brokerage firms will hold these funds in a segregated “cash-covered put reserve,” which reduces the investor’s “cash available to trade” but often continues to earn interest in a money market fund.10 The total cash required is StrikePrice×100. For example, selling one put with a $90 strike price requires $9,000 of secured cash.

The act of fully collateralizing the trade is what transforms the risk profile. It distinguishes the conservative cash-secured put from its high-risk cousin, the “naked put.” A naked put seller uses margin and does not hold the cash to buy the shares; their goal is purely to collect the premium, and an assignment can lead to significant, leveraged losses. The cash-secured put writer, by contrast, has already committed the capital and views assignment as a potentially favorable outcome, making the strategy’s risk profile comparable to that of direct stock ownership.

How It Works: A Step-by-Step Walkthrough with a Foundational Example

The mechanics of a cash-secured put can be illustrated with a straightforward example.

- Select a Stock and a Target Purchase Price: An investor has researched Company XYZ, which is currently trading at $55 per share. The investor is bullish on the company’s long-term prospects but believes the current price is slightly elevated and would prefer to purchase shares at a lower price point, specifically $50 per share.1

- Sell the Put Option: The investor sells one put option contract on XYZ with a strike price of $50 that expires in one month. For selling this contract, they receive a premium of $2.30 per share, for a total of $230 ($2.30 x 100 shares).1

- Secure the Cash: Immediately upon execution of the trade, the investor’s brokerage firm will reserve the necessary funds to cover a potential assignment. The required collateral is $50 (strike price) x 100 shares = $5,000.1

- Await Expiration: The investor now waits until the option’s expiration date, at which point one of two primary outcomes will occur.

- Outcome 1: Stock Price Stays Above the Strike Price. If, at expiration, XYZ is trading at any price above $50 (e.g., $52), the put option is “out-of-the-money.” The buyer will have no incentive to exercise their right to sell the stock at $50 when they could sell it on the open market for a higher price. The option expires worthless. The investor keeps the $230 premium as pure profit, and the $5,000 in secured cash is released. The investor has successfully generated income on their capital.1

- Outcome 2: Stock Price Falls Below the Strike Price. If, at expiration, XYZ is trading at a price below $50 (e.g., $48), the option is “in-the-money.” The buyer will likely exercise their right to sell their shares at the advantageous price of $50. The investor is assigned and is obligated to buy 100 shares of XYZ at $50 per share, using the $5,000 of reserved cash. The investor now owns the stock. However, the effective purchase price, or cost basis, is reduced by the premium they initially received. The effective cost per share is $50 (strike price) – $2.30 (premium) = $47.70.1 The investor has successfully acquired the desired stock at a discount to both the original market price and the strike price.

The Strategic Calculus: Risk, Reward, and Profitability

Understanding the precise financial parameters of a cash-secured put is essential for effective risk management and strategy deployment. The profit and loss profile is distinct, characterized by a capped upside and substantial, though defined, downside risk.

Maximum Profit: Capped by the Premium

The maximum profit an investor can realize from the cash-secured put position itself is strictly limited to the net premium received when the option was sold.6 This best-case scenario is achieved if the underlying stock price closes at or above the strike price at the expiration date, causing the option to expire worthless. The investor retains the full premium, and the cash held as collateral is freed. The formula for maximum profit is:

Maximum Profit=Premium Received per Share×100Maximum Risk: The Nuances of “Stock-Equivalent” Downside

The maximum potential loss on a cash-secured put is substantial and is realized if the underlying stock’s price falls to $0. In this extreme scenario, the investor is still obligated to purchase the shares at the strike price, leaving them with worthless stock. The loss is buffered only by the initial premium received.6 The formula for maximum loss is:

Maximum Loss=(Strike Price×100)−(Premium Received per Share×100)It is critical to recognize that this risk profile is functionally equivalent to the risk of owning the stock directly from the breakeven price.1 An investor who buys a stock outright also faces the risk of the price falling to zero. The cash-secured put seller faces the same downside exposure, but their loss is always less than that of an investor who bought the stock at the strike price, thanks to the cushioning effect of the premium.6

This asymmetrical risk profile, with its limited profit and substantial potential loss, is not a design flaw but a deliberate strategic trade-off. The investor consciously forgoes the unlimited upside potential that comes with direct stock ownership. In exchange, they receive two immediate and tangible benefits: a guaranteed income stream from the premium and the opportunity to acquire the stock at a lower effective price. The decision to use a cash-secured put is therefore a calculated choice to prioritize income generation and a favorable entry point over capturing potentially explosive upward price movements, reframing the “risk” as a known and accepted opportunity cost.

Calculating the Breakeven Point: Your Margin of Safety

The breakeven point is the stock price at expiration at which the investor, if assigned, would have neither a profit nor a loss on the overall position. It represents the true cost basis of the acquired shares. Any stock price above this level at assignment results in an unrealized gain, while any price below it results in an unrealized loss.14 The formula is straightforward:

Breakeven Price=Strike Price−Premium Received per ShareUsing the previous example of Company XYZ, the breakeven price was $50 (strike) – $2.30 (premium) = $47.70. If the investor is assigned the stock, their position is profitable as long as the market price of XYZ remains above $47.70.

The Greeks for the Put Seller: Understanding Delta, Theta, and Vega

For a more nuanced understanding, investors can use the “Greeks,” which are measures of an option’s sensitivity to various factors. For a put seller, the most important are:

- Theta (θ): Often called “time decay,” theta measures how much an option’s price is expected to decrease each day, all else being equal. Theta is the primary ally of the option seller. As time passes and the expiration date approaches, the option’s extrinsic value erodes, which benefits the seller who wants the option’s value to go to zero. This is why selling options is known as a “positive theta” strategy.8

- Delta (Δ): Delta measures the expected change in an option’s price for a $1 change in the underlying stock’s price. For put options, delta ranges from 0 to -1.0. Importantly for put sellers, delta can also be used as a rough approximation of the probability that the option will expire in-the-money. A put with a delta of -0.25 has approximately a 25% chance of expiring in-the-money and being assigned. Investors can use delta to select a strike price that aligns with their desired probability of acquiring the stock.19

- Vega (ν): Vega measures an option’s sensitivity to changes in the implied volatility of the underlying stock. Higher implied volatility leads to higher option premiums. Therefore, a put seller benefits from selling an option when volatility is high, as they receive more premium for taking on the same obligation. An unexpected increase in volatility after the put is sold will increase the option’s price, creating an unrealized loss for the seller.3

The Investor’s Intent: Why and When to Deploy Cash-Secured Puts

The decision to use a cash-secured put strategy stems from a specific set of investment goals and a particular market outlook. The strategy is not a one-size-fits-all solution but a targeted tool for achieving one of two primary objectives.

Primary Objective 1: A Disciplined Approach to Stock Acquisition

The foremost motivation for many investors using this strategy is to acquire a specific stock at a price they deem attractive, with the assignment of shares being the desired outcome.3 In this context, the cash-secured put functions as a superior alternative to a standard limit buy order. While a limit order simply sits and waits to be filled, generating no return, the cash-secured put pays the investor a premium for their patience.4

If the stock price falls and the option is assigned, the investor purchases the shares at the strike price, with the premium received effectively lowering the net purchase price. This disciplined method ensures the investor only enters a position at a pre-determined, favorable cost basis.

Primary Objective 2: Generating Enhanced Yield on Cash

The second primary objective is to generate income on cash that is otherwise sitting idle in a portfolio.8 An investor might have cash reserves set aside for future opportunities but wants that capital to be productive in the interim. By selling out-of-the-money cash-secured puts on stable, high-quality stocks, the investor can collect regular premium income.

In this application, the investor’s primary goal is for the option to expire worthless. They select strike prices far enough below the current market price that assignment is unlikely. If the option expires out-of-the-money, they keep the premium, and the process can be repeated, creating a consistent yield on their cash holdings that typically surpasses what is available from traditional money market accounts or short-term bonds.14

Ideal Market Outlook: Neutral to Mildly Bullish Conviction

The cash-secured put strategy is most appropriate for an investor who holds a neutral to mildly bullish long-term forecast for the underlying security.1 This outlook is nuanced. The investor is fundamentally positive on the company’s prospects but may anticipate a period of short-term price consolidation, sideways movement, or a minor pullback.6

- A strongly bullish investor would likely be better served by purchasing the stock or call options directly to capture the full upside potential.

- A strongly bearish investor should avoid this strategy, as the risk of being assigned a rapidly depreciating asset is significant.

The ideal scenario is one where the stock price remains stable or drifts slightly higher, allowing the option to expire worthless for an income-focused investor, or dips just below the strike price, triggering a favorable assignment for an acquisition-focused investor.

The Art of Selection: Key Parameters for Execution

The success of a cash-secured put strategy hinges on a series of deliberate choices made before the trade is ever placed. These decisions regarding the underlying asset, strike price, and expiration date are interconnected and should be guided by the investor’s primary objective and risk tolerance.

Choosing the Underlying Asset: Beyond High Premiums

The single most important rule when selling cash-secured puts is to only use the strategy on an underlying asset—be it a stock or an ETF—that one would be genuinely comfortable owning for the long term at the strike price.3 The possibility of assignment must always be treated as a realistic and acceptable outcome. An investor should never sell a put on a low-quality or speculative company simply because it offers a high premium, as this is a direct path to being forced to buy a deteriorating asset.

Key criteria for selecting a suitable underlying asset include:

- Fundamental Strength: The company should have a solid balance sheet, consistent earnings, and a durable competitive advantage.

- Reasonable Valuation: The investor should have a thesis as to why the stock is a good value at or below the chosen strike price.

- Liquidity: The stock and its options should have high trading volume and tight bid-ask spreads. This ensures that the position can be entered and exited efficiently and at a fair price.22

Selecting the Strike Price: Balancing Probability and Profit

The choice of strike price is a direct trade-off between the amount of premium received and the probability of assignment.

- Out-of-the-Money (OTM): Selling a put with a strike price below the current stock price is the most common approach. OTM puts offer lower premiums but have a higher probability of expiring worthless, making them ideal for investors focused primarily on income generation. A strike with a delta of -0.30 or lower (e.g., -0.20) is a common choice for this objective, implying a 70-80% probability of the option expiring worthless.

- At-the-Money (ATM): Selling a put with a strike price very close to the current stock price will generate a much higher premium. However, it also carries a significantly higher probability of assignment (approximately 50%, as indicated by a delta near -0.50).6 This is more suitable for an investor whose primary goal is to acquire the stock and who wants to maximize the premium collected to lower their cost basis.

Choosing the Expiration Date: The Role of Time Decay (Theta)

The selection of an expiration date involves balancing premium income against the rate of time decay.

- The 30-45 Day “Sweet Spot”: Many experienced options sellers favor expirations in the 30 to 45 day range.4 This period is considered optimal because it is when the rate of theta decay begins to accelerate significantly. The option loses its time value most rapidly during this window, which is highly beneficial to the seller.

- Short-Term vs. Long-Term Expirations:

- Weekly Options: Offer the potential for higher annualized returns if the strategy is repeated successfully. However, they are more susceptible to short-term price swings (gamma risk) and require more active management.

- Longer-Dated Options (90+ days): Provide a larger upfront premium in absolute terms. However, they tie up capital for a longer period, and the rate of time decay is much slower in the early stages of the option’s life.

The Impact of Implied Volatility on Premium and Strategy

Implied volatility (IV) is a measure of the market’s expectation of future price swings in a stock. It is a key determinant of an option’s price; higher IV results in higher premiums.3 The ideal time to sell a cash-secured put is when a stock’s implied volatility is elevated, perhaps due to market uncertainty or an upcoming earnings announcement. Selling options in a high-IV environment means the investor receives more income for taking on the same level of price risk. This concept is often referred to as “selling fear,” as the seller is compensated for providing a form of price insurance when demand for that insurance is high.

These strategic variables—underlying asset, strike price, expiration, and volatility—are not independent. A sophisticated investor manipulates these levers to construct a trade that aligns perfectly with their goals. For instance, an investor seeking a 1.5% return on cash over 30 days might find that a low-volatility blue-chip stock requires selling a strike very close to the current price. Alternatively, they could seek out another high-quality stock that has recently experienced a temporary spike in implied volatility, allowing them to sell a strike much further out-of-the-money (and thus with a higher margin of safety) while still achieving their desired premium income. This demonstrates a proactive, goal-oriented approach to trade construction rather than a passive acceptance of market prices.

A Comparative Framework: Cash-Secured Puts vs. Alternative Strategies

To fully appreciate the unique role of the cash-secured put, it is useful to compare it against other common investment strategies that share similar objectives or risk profiles.

The Synthetic Twin: In-Depth Comparison with the Covered Call

The covered call is perhaps the strategy most closely related to the cash-secured put. A covered call involves owning at least 100 shares of a stock and selling one call option contract against those shares. While the mechanics are different, their financial risk profiles are synthetically identical, a principle derived from put-call parity.6

- Mechanics and Outcome: A covered call can result in the investor selling their stock if the price rises above the call’s strike price. A cash-secured put can result in the investor buying stock if the price falls below the put’s strike price.25

- Risk Profile: Both strategies have limited profit potential (capped by the premium plus any capital appreciation up to the strike price) and substantial downside risk that is buffered by the premium received.

- Investor Position and Outlook: The primary difference lies in the investor’s starting position and goal.

- Covered Call: Best for an investor who already owns the stock, is neutral to slightly bullish, and wishes to generate income from their holding.25

- Cash-Secured Put: Best for an investor who currently holds cash, is neutral to slightly bullish, and wishes to either acquire the stock at a lower price or generate income on that cash.

Beyond the Basics: Contrasting with Naked Puts and Limit Orders

- Naked Puts: As previously discussed, a naked put writer sells a put without holding the cash to purchase the shares, instead using brokerage margin. The motivation is purely to collect the premium, and assignment is an undesirable outcome that can lead to a forced, leveraged stock purchase. It is a high-risk, speculative strategy fundamentally different in both intent and risk management from the conservative cash-secured put.6

- Limit Orders: A limit order is a simple instruction to a broker to buy a stock at a specified price or better. While it serves the goal of acquiring a stock at a target price, it generates zero income while the investor waits for the order to be filled. The cash-secured put can be viewed as a limit order that pays the investor a premium for their patience and commitment.1

The following table provides a clear, at a glance comparison of these strategies.

| Feature | Cash-Secured Put | Covered Call | Naked Put | Limit Buy Order |

| Primary Goal | Acquire stock at a discount or generate income on cash | Generate income on existing stock holdings | Generate premium income only | Acquire stock at a specific price |

| Required Position | Cash equal to strike price x 100 | 100 shares of underlying stock | Sufficient margin | None (cash needed upon execution) |

| Market Outlook | Neutral to Mildly Bullish | Neutral to Mildly Bullish | Neutral to Bullish | Bullish (at the limit price) |

| Maximum Profit | Limited to premium received | Limited to premium + (strike – stock cost) | Limited to premium received | Unlimited |

| Maximum Risk | Substantial (strike price – premium) | Substantial (stock cost – premium) | Substantial and potentially leveraged | Substantial (limit price) |

| Key Advantage | Generates income while waiting to buy stock | Generates income from an existing asset | High leverage and capital efficiency | Simple, direct execution |

Case Study: Executing a Cash-Secured Put on Apple Inc. (AAPL)

To illustrate the practical application of the strategy, this case study will analyze a hypothetical cash-secured put trade on Apple Inc. (AAPL), using realistic market data.

Scenario Setup: Market Conditions, Investor Thesis, and Initial Trade

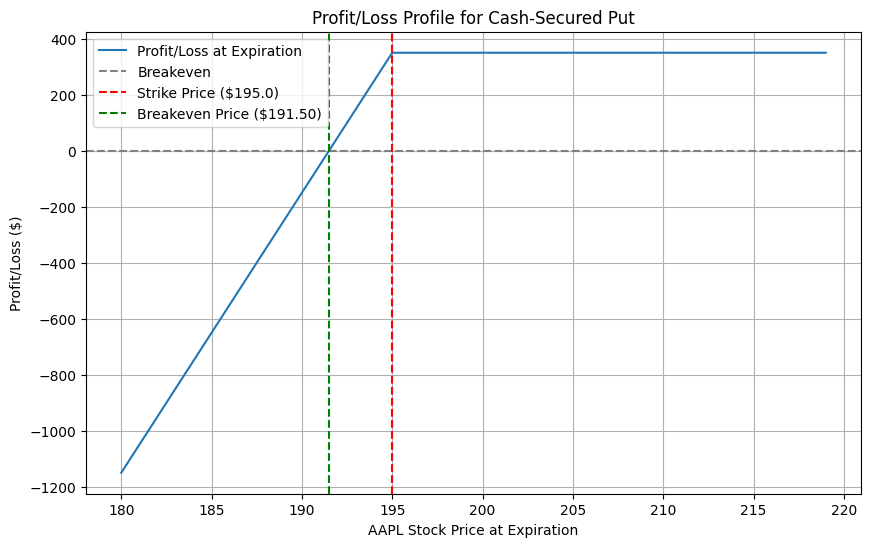

- Date: June 3, 2025

- Market Price of AAPL: $203.27

- Investor Thesis: An investor holds a long-term bullish view on Apple due to its strong brand, ecosystem, and financial health. However, they note the stock has had a strong run and would prefer to initiate a position at a lower price, viewing the $195 level as a zone of technical support and better value. Their dual goal is to either acquire 100 shares at an effective price below $195 or generate a solid return on their cash reserve of $19,500.

- The Trade: The investor decides to sell one cash-secured put contract on AAPL.

- Action: Sell to Open 1 AAPL Put Contract

- Expiration Date: July 18, 2025 (45 days until expiration)

- Strike Price: $195.00

- Premium: Based on historical options data patterns, a realistic premium for this out-of-the-money put would be approximately $3.50 per share.30

- Trade Summary:

- Total Premium Received: $3.50 x 100 shares = $350

- Cash Secured by Broker: $195.00 x 100 shares = $19,500

- Breakeven Price at Expiration: $195.00 (Strike) – $3.50 (Premium) = $191.50

Outcome A: The Option Expires Worthless (Profit Scenario)

- Condition: On the expiration date, July 18, 2025, Apple’s stock price closes at $205.00. This price is well above the $195 strike price.

- Result: The put option is out-of-the-money and expires worthless. The investor’s obligation to buy the shares is extinguished.

- Financial Outcome: The investor retains the full $350 premium as profit. The $19,500 cash reserve is released by the broker.

- Analysis: This outcome fulfills the investor’s income generation goal. They achieved a return of 1.79% on their secured capital ($350 / $19,500) over a 45-day period. This equates to an annualized return of approximately 14.5% (1.79%×(365/45)), significantly outperforming typical cash-equivalent yields. The investor can now choose to repeat the process by selling another put for a future expiration date.

Outcome B: The Option is Assigned (Acquisition Scenario)

- Condition: On July 18, 2025, AAPL stock has experienced a minor pullback and closes at $192.00 per share. This price is below the $195 strike price.

- Result: The put option is in-the-money and is exercised by the buyer. The investor is assigned and is obligated to purchase 100 shares of AAPL at the strike price of $195 per share. The $19,500 of secured cash is used to complete the transaction.

- Financial Outcome: The investor now owns 100 shares of AAPL. Their effective cost basis for these shares is the breakeven price of $191.50 per share.

- Analysis: This outcome fulfills the investor’s stock acquisition goal. They have purchased AAPL at an effective price that is not only below the price when they initiated the trade ($203.27) but also below the current market price ($192.00). At the moment of assignment, they have an immediate unrealized profit of ($192.00 – $191.50) x 100 = $50. They now hold a long-term position in a company they believe in, acquired at a strategically chosen price.

Outcome C: Managing a Losing Position (The Stock Declines Sharply)

- Condition: Due to unexpected negative market news, on July 18, 2025, AAPL stock has fallen significantly and closes at $185.00 per share. This is well below both the strike price and the breakeven point.

- Result: The option is deep in-the-money and is assigned. The investor buys 100 shares of AAPL at $195 per share.

- Financial Outcome: The investor owns 100 shares of AAPL with a cost basis of $191.50. With the current market price at $185.00, they have an unrealized loss of ($191.50 – $185.00) x 100 = $650.

- Analysis: This scenario highlights the primary risk of the strategy. The investor is now holding a depreciated asset. However, it is crucial to note that their loss is $350 less than it would have been if they had simply placed a limit order to buy the stock at $195, which would have resulted in an unrealized loss of $1,000. The premium acts as a buffer, mitigating the downside.6 Because the investor’s initial thesis was based on a willingness to own AAPL for the long term, they can now hold the shares and wait for a price recovery or proceed to the next phase of an advanced strategy like the Wheel.

Advanced Management: The Concept of “Rolling” the Position

If, as expiration approaches, the stock is trading near the strike price (e.g., $194.50) and the investor prefers to avoid assignment and continue generating income, they can “roll” the position. This involves a single transaction to:

- Buy to Close the existing July $195 put.

- Sell to Open a new put with a later expiration (e.g., August 15) and often a lower strike price (e.g., $190).

Frequently, this can be done for a net credit, meaning the investor receives more premium for the new put than they pay to close the old one. This allows them to effectively extend the trade, collect more income, and lower their potential purchase price, all while avoiding immediate assignment.9

| AAPL Price at Expiration | Option Action | Gross Stock Cost | Premium Kept | Net Cost / Profit | Unrealized P/L on Stock (if Assigned) |

| $210.00 | Expires Worthless | $0 | $350 | $350 Profit | N/A |

| $196.00 | Expires Worthless | $0 | $350 | $350 Profit | N/A |

| $194.00 | Assigned | $19,500 | $350 | $19,150 Net Cost | -$150 |

| $191.50 (Breakeven) | Assigned | $19,500 | $350 | $19,150 Net Cost | $0 |

| $190.00 | Assigned | $19,500 | $350 | $19,150 Net Cost | +$150 |

| $185.00 | Assigned | $19,500 | $350 | $19,150 Net Cost | +$650 |

Advanced Application: The “Wheel” Strategy

The cash-secured put is not only a powerful standalone strategy but also the foundational first step in a more comprehensive, cyclical income-generating system known as the “Wheel” strategy.20 The Wheel is the logical continuation for an investor who has been assigned shares from a cash-secured put and wishes to continue using their new asset to produce income.

Introduction to the Wheel: A Cyclical Income Engine

The Wheel strategy is a systematic process that involves continuously selling options to generate premium. It begins with selling cash-secured puts on a desired stock. If the puts expire worthless, the process is repeated. If the puts are assigned, the investor takes ownership of the stock and immediately begins selling covered calls against those shares. If the covered calls result in the shares being “called away” (sold), the investor is back to a cash position and can restart the entire cycle by selling puts again.33 The objective is to constantly collect premium, whether the investor is holding cash (via short puts) or stock (via short calls).

From Cash-Secured Put to Covered Call: Completing the Cycle

Using the AAPL case study as a starting point, the Wheel strategy unfolds as follows:

- Sell a Cash-Secured Put: The investor sells the July $195 AAPL put and collects $350.

- Get Assigned: The stock price falls, and the investor is assigned 100 shares of AAPL at $195. Their effective cost basis is $191.50.

- Sell a Covered Call: Now owning 100 shares, the investor immediately sells a covered call. They might choose an August 15 expiration with a $200 strike price, collecting an additional premium of, for instance, $2.50 per share ($250 total). The strike is chosen above their cost basis to ensure a profit if the shares are sold.

- Evaluate the Covered Call Outcome:

- Scenario A: AAPL closes below $200. The call option expires worthless. The investor keeps the $250 premium and their 100 shares of AAPL. They have now collected a total of $350 (from the put) + $250 (from the call) = $600 in premium. This reduces their net cost basis on the stock to $191.50 – $2.50 = $189.00. They can then repeat Step 3 by selling another covered call for a future month.

- Scenario B: AAPL closes above $200. The call option is exercised, and the investor’s 100 shares are called away, meaning they are sold at the strike price of $200 per share.

- Restart the Wheel: The investor is now back to a full cash position. Their total profit from the entire cycle is the sum of the capital gain on the stock plus the premiums from both the put and the call.

- Capital Gain: ($200.00 Sale Price – $191.50 Cost Basis) x 100 = $850

- Call Premium: $250

- Total Profit (excluding the initial put premium): $850 + $250 = $1,100. The full cycle profit is $1,100 + $350 = $1,450.The investor can now return to Step 1 and sell a new cash-secured put on AAPL or another desired stock, keeping the “wheel” in motion.

The power of the Wheel strategy over the long term lies not just in the discrete income payments, but in its systematic ability to reduce the cost basis of a stock holding.20 Each premium collected, from both the initial put and any subsequent covered calls, chips away at the net capital invested in the position. This creates a powerful financial and psychological advantage, as it steadily lowers the price at which the stock can be sold for a profit. This continuous reduction of the cost basis is the true engine of the Wheel, shifting the investor’s focus from short-term price fluctuations to the long-term management of their net investment in a quality asset.

Tax Implications for the U.S. Investor

The tax treatment of options can be complex, and it is crucial for investors to understand the implications of each potential outcome of a cash-secured put strategy. The guiding principle is that the premium received upon selling the put is not considered taxable income at the moment of the transaction. Instead, its tax treatment is deferred until the position is terminated through expiration, assignment, or a closing purchase.

Tax Treatment of the Premium: Expiration vs. Assignment

The tax consequences depend entirely on how the put option contract is resolved:

- If the Put Expires Worthless: When an out-of-the-money put option expires, the seller’s obligation ends. The entire premium they initially received is then realized as a short-term capital gain. This is true regardless of how long the option contract was held (e.g., 30 days or 9 months). The gain is reported in the tax year in which the option expires.38

- If the Put is Assigned: When the put option is exercised and the seller is obligated to buy the underlying stock, there is no immediate taxable event. The premium received is not reported as a gain. Instead, the premium is used to reduce the cost basis of the newly acquired shares. This lower cost basis will affect the calculation of capital gains or losses when the stock is eventually sold.

Establishing Cost Basis and Holding Period Upon Assignment

Upon assignment, two critical factors are established for tax purposes:

- Cost Basis: As described above, the cost basis of the stock purchased is the strike price minus the premium received per share. In the AAPL case study, assignment at the $195 strike after collecting a $3.50 premium results in a tax cost basis of $191.50 per share.

- Holding Period: The holding period for the acquired stock begins on the day after the assignment occurs. It does not relate back to the date the put option was originally sold.38 This is a vital detail, as it determines whether the eventual sale of the stock will be classified as a short-term (held one year or less) or long-term (held more than one year) capital gain or loss, which are taxed at different rates.

Tax Consequences of Closing the Position Early

If an investor decides to exit the position before expiration by buying back the same put option they sold (a “buy-to-close” order), a taxable event is triggered. The resulting gain or loss is calculated as the difference between the premium originally received and the cost to buy back the option. This transaction is always treated as a short-term capital gain or loss.

The following table summarizes the tax treatment for each scenario.

| Scenario | Taxable Event? | Tax Treatment |

| 1. Put Expires Worthless | Yes, at expiration. | The full premium received is a short-term capital gain. |

| 2. Put is Assigned (Stock Purchased) | No, not at assignment. | The premium reduces the cost basis of the acquired stock. |

| 3. Position is Closed via Buy-to-Close | Yes, at closing. | (Premium Received – Cost to Close) = Short-term capital gain or loss. |

| 4. Assigned Stock is Later Sold (≤ 1 Year) | Yes, at sale. | (Sale Price – Reduced Cost Basis) = Short-term capital gain or loss. |

| 5. Assigned Stock is Later Sold (> 1 Year) | Yes, at sale. | (Sale Price – Reduced Cost Basis) = Long-term capital gain or loss. |

Conclusion

The cash-secured put is a robust and conservative options strategy that offers a disciplined framework for both income generation and strategic stock acquisition. Its strength lies not in speculative potential but in its methodical approach to achieving predefined financial objectives. By selling a put option fully collateralized by cash, an investor makes a conscious decision to accept one of two favorable outcomes: earning a premium as a return on capital or purchasing a quality asset at an effective price below the current market. This dual-purpose nature makes it a valuable tool for investors seeking to enhance portfolio returns while managing risk in a deliberate manner.

The success of the strategy is fundamentally tied to the investor’s mindset and preparation. The foundational principle is that assignment should not be viewed as a failure but as the successful execution of an acquisition plan. This requires diligent research into the underlying asset and a commitment to only sell puts on companies the investor would be content to own for the long term. The strategic selection of the strike price and expiration date, informed by factors like implied volatility and the option Greeks, allows investors to tailor each trade to their specific goals, whether maximizing income or increasing the probability of acquiring shares.

When compared to alternatives, the cash-secured put demonstrates clear advantages. It provides an income stream that a simple limit order cannot, and it operates with a fundamentally more conservative risk profile than a naked put. Its synthetic equivalence to the covered call positions it as a cornerstone of income-focused options trading, naturally leading to advanced applications like the perpetual income cycle of the Wheel strategy. By understanding the mechanics, the risk-reward calculus, and the critical tax implications, the intermediate investor can effectively elevate the cash-secured put from a theoretical concept to a practical and powerful component of a sophisticated investment portfolio.

Before implementing this or any options strategy, investors should perform thorough due diligence. Options trading entails significant risk and is not appropriate for all investors. The information presented in this report is for educational purposes only. It is strongly recommended to consult with a qualified financial advisor and a tax professional to determine the suitability of this strategy for one’s individual financial situation and objectives.43