January 4, 2026

Global Silver Market Analysis – January 2026

Price Overview and Recent Volatility

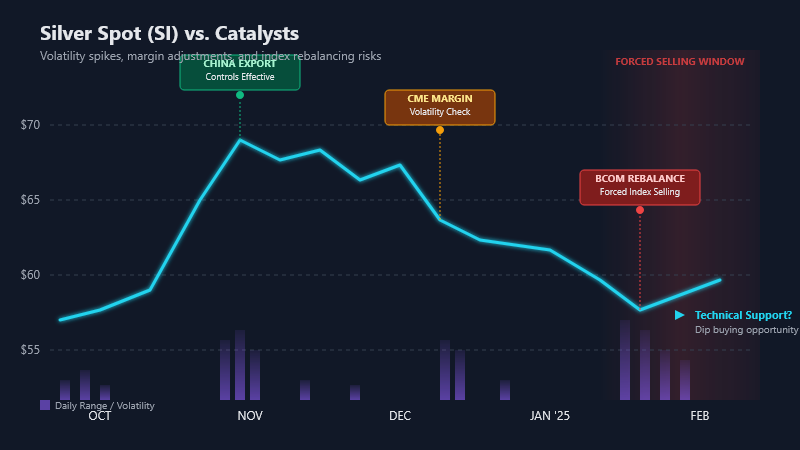

Silver prices enter 2026 at historically elevated levels after a spectacular rally in 2025. Front-month COMEX silver futures settled around $70.13/oz at year-end 2025, marking a 142% annual gain[1] – the strongest performance since 1979. In mid-October, silver broke out to a then-record $54.48/oz, and by late December it briefly spiked above $80–84/oz in thin trading. This was followed by one of silver’s largest intraday reversals on record: prices plunged back toward $60–70 within hours, as a wave of year-end profit-taking and margin-call driven liquidation hit the precious metals sector. The wild swings underscore how volatile and fast-moving the silver market has become – for example, in one session silver “flirted with $71.00 in early Asian trading” before cratering 18% to close below $60 during a liquidity crunch. Despite this turbulence, silver is still trading around the high-$60s per ounce in early January 2026, holding well above the long-term technical breakout zone and retaining the bulk of last year’s gains.

From a technical standpoint, silver’s surge has decisively broken above the long-term resistance in the $50 area. The $50–$54/oz region, which capped rallies for over 13 years (since the 2011 peak near $49), has now turned into a support base. Analysts note that maintaining weekly closes above ~$54 signals that silver has entered a new price discovery regime, with little historical resistance above. Upside technical targets from the multi-year consolidation pattern lie around $72/oz and $88/oz if the uptrend resumes, although near-term momentum has been damaged by the late-December flash crash. Key technical support levels to watch include the 50-day moving average (around the mid $50s), which was tested during the recent plunge. A sustained break back below the $50 level would be a bearish signal, while on the upside a move through the late-2025 highs (~$80+) could trigger another explosive leg higher. In sum, silver’s chart structure has dramatically improved after 2025’s breakout, but volatility remains extreme, so traders are braced for large swings around those pivotal price levels.

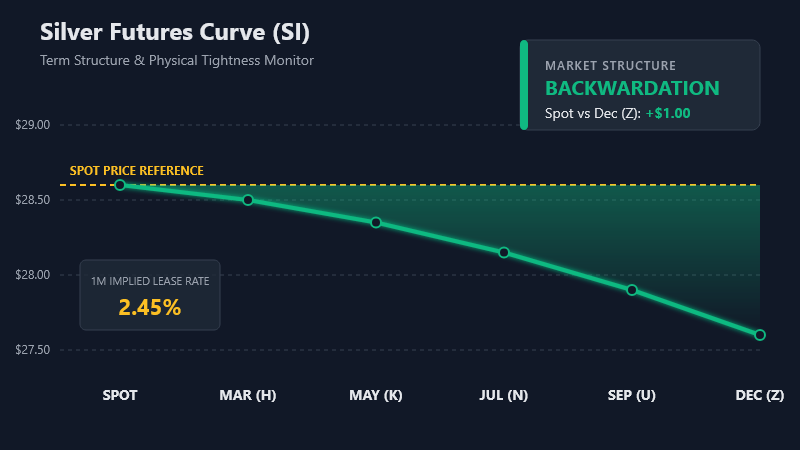

Several key drivers fueled silver’s price surge and will continue to influence the market. First, intense physical demand – both industrial and investment – created a squeeze in available supply. This was evidenced by a rare and persistent backwardation in the futures curve (spot prices trading above future prices), signaling buyers paying a premium for immediate delivery. Normally silver trades in contango (future > spot due to storage costs), but in late 2025 the situation flipped: at one point spot silver commanded about $2.88/oz higher than the futures – the largest such spread since the 1980s. Such backwardation is “the market flashing a red alert” that immediate demand has overwhelmed supply. Second, macroeconomic conditions have been favorable: a weaker U.S. dollar (down ~9.5% in 2025) and expectations of easier monetary policy have boosted precious metals as an inflation and currency hedge. Gold, the traditional safe haven, climbed ~60% last year, and silver – which often outpaces gold in bull markets – outperformed even that. Finally, technical and speculative factors kicked in: once silver broke long-term resistance and momentum funds piled in, the rally fed on itself until checked by year-end profit taking. Notably, the CME Group had to raise margin requirements repeatedly in Q4 2025 (over half a dozen hikes since late September) to tamp down volatility. Each standard COMEX silver contract (5,000 oz) was swinging by nearly $20,000 in value on volatile days, prompting 30%+ increases in collateral requirements. These margin hikes likely contributed to the late-December pullback by forcing some leveraged longs to liquidate, illustrating how exchange policies can swiftly impact short-term price action.

Market Structure: Paper vs. Physical Dynamics

The historic backwardation in silver highlights an important shift in market structure: physical demand is now driving price discovery, eclipsing the influence of “paper” trading. Typically, the vast volume of COMEX futures and OTC derivatives exerts a dominant influence on silver’s spot price, often allowing speculative short-sellers to pressure prices even amid strong fundamentals. However, in late 2025 this dynamic showed signs of breaking down. With spot prices rising faster than futures, futures were forced to follow the physical market’s lead. Analysts note that this is a pivotal change – it suggests real-world supply and demand are finally setting the tone, as opposed to leveraged paper positions. In other words, the “tail” of paper silver stopped wagging the “dog” of physical silver, at least for now. Each dollar of backwardation effectively marks a transfer of pricing power away from COMEX and towards the spot (physical) market, where shortages were acute.

A look at the futures curve confirms the unusual state of affairs. As of early January, the COMEX silver forward curve remains inverted in the near term, with prices for immediate or nearby delivery above those for later in 2026. At one stage, every COMEX contract through late 2026 was trading below the current spot price – an extraordinary scenario that signals expectations of prolonged physical tightness. (By contrast, in a normal contango market, each successive futures contract would be slightly more expensive, reflecting carrying costs.) Recently the curve has started to partially normalize as some short-term pressures eased – for instance, after the December delivery rush, the very far dated contracts moved back to a slight contango. But overall the structure is far flatter and more backwardated than at any time in recent decades. This backwardation has also been mirrored in the London market: one-month silver lease rates (the cost to borrow physical metal) spiked above 30–39% in October 2025 (versus a typical <1% rate), indicating extreme scarcity of available bullion. Such levels of leasing stress had not been seen since the Hunt Brothers’ cornering attempt in 1980.

Driving this shift is a clear disconnect between paper claims and physical supply. For years, critics pointed out that silver had a high paper leverage (many more ounces traded via contracts than exist in vaults). In 2025, that latent issue became very real. Exchange inventories were drawn down sharply as more traders demanded actual delivery instead of rolling their futures. At the COMEX (New York) vaults, a remarkable run occurred during the December contract delivery period: 47.6 million ounces were claimed for delivery in the first four trading days of December. This alone amounted to over 60% of all the registered (deliverable) silver in COMEX warehouses, an unprecedented depletion rate. (Registered silver refers to bars set aside with a warehouse warrant ready for delivery; there is additional “eligible” bullion in storage that isn’t currently backing a contract, but turning eligible into registered takes time and owner consent.) COMEX registered stocks have been falling since 2020, down more than 73% from their peak by the end of 2025. Total silver in COMEX approved vaults (registered + eligible) is now at multi-year lows, reflecting the steady drain from investors and industrial users pulling physical metal out of the system.

In London, which houses the largest global silver stockpiles, inventories have also tightened, though recent data show a slight uptick as some supply was repositioned to London late in the year. As of end-November 2025, the LBMA vaults held 27,187 tonnes of silver (about 873 million ounces). This was a 3.5% increase from the prior month, possibly due to last-minute stockpiling and inflows ahead of China’s export restrictions (discussed later). Even with that increase, London silver holdings remain well below their 2020 highs – a reflection of several years of deficits and demand. In fact, Shanghai’s exchange inventories collapsed to decade lows in 2025, as China became a net exporter of silver to meet global needs. The Shanghai stock drawdowns (down to ~446 tonnes, the lowest since 2016, after heavy exports) fed into Western markets and partially bolstered London, but could not prevent the overall squeeze. The net effect is that visible above-ground silver inventories (COMEX, LBMA, Shanghai) are much reduced compared to a few years ago – a stark backdrop for a market that saw explosive demand.

In summary, the paper vs. physical dynamic has tilted toward the physical side. Backwardation and soaring lease rates are clear evidence that immediate physical silver is valued more highly than promises of future delivery, a rarity that underscores the market’s tightness. This dynamic has emboldened some bullish analysts to suggest that the long era of price suppression via paper may be ending, as genuine scarcity forces a repricing of silver. However, it also introduces volatility: if the shortage eases even temporarily, the unwinding of backwardation can spur rapid price retreats (as seen with the volatile swings around year-end). Traders will be closely watching COMEX warehouse reports and delivery notices in the coming months – any further large offtakes or deposits could swing sentiment quickly.

Fundamental Supply and Demand Factors

Supply and demand fundamentals provide important context for silver’s current strength. The silver market has been in a structural deficit for several years, meaning consumption has exceeded new supply. 2025 marked the fifth consecutive annual deficit in the silver market. According to the Silver Institute’s estimates, total silver demand in 2025 reached ~1.12 billion ounces, exceeding total supply by about 95 million ounces. Although this deficit was slightly smaller than 2022–2024’s shortfalls (2024’s deficit was estimated near 148 Moz, and 2022 saw a record ~238 Moz deficit), it remains sizeable. Cumulatively from 2021–2025, the world consumed roughly 820 Moz more silver than was produced. Such persistent draws have significantly thinned above-ground inventories, explaining much of 2025’s market tightness. In effect, silver has been “eating into” existing stocks (from vaults, scraped jewelry, old coins, etc.) to satisfy demand – a situation that is unsustainable long-term without either demand destruction or new supply coming online.

On the supply side, silver mine output has been relatively stagnant. Global mine production in 2025 is estimated around 813 million ounces, flat compared to 2024. Incremental gains in top producer countries like Mexico and Russia were offset by declines elsewhere (e.g. Peru and Indonesia). Notably, primary silver mines (which account for only ~28% of silver output) showed only a minor increase, while a large portion of supply comes as a byproduct of mining other metals (gold, copper, lead/zinc). Therein lies a constraint: because much silver is a byproduct, higher silver prices do not immediately spur a lot of new mine investment – production is tied to the output of other metal mines. Indeed, industry experts project no significant new silver mine capacity until 2027–2028 at the earliest. Many existing mines are already at full tilt, and any big new projects (or major expansions) have long lead times. Thus, mine supply is not very responsive in the short run to the price spike. Meanwhile, recycling of silver has ticked up but is not a game changer. Silver recycling (from industrial scrap, jewelry scrap, etc.) rose ~1% in 2025 to a 13-year high, spurred by higher prices. Even so, recycling contributed only modest additional metal – far from enough to close a nearly 100 Moz gap. In essence, fresh supply (mining + recycling) is barely moving the needle, leaving deficits to be filled by drawing down inventories or dishoarding.

The demand side of the equation, however, remains robust and is evolving. Industrial demand is the single largest component, typically making up about half of total silver usage. In 2025, industrial offtake is estimated at 665 Moz. This was actually slightly lower (by ~2%) than the 2024 record, due in part to macroeconomic headwinds and significant thrifting efforts by manufacturers in response to high silver prices. For instance, the photovoltaic (solar panel) sector – a key growth driver for silver – saw record global solar installations in 2025, yet the silver used in PV actually declined by ~5% year-on-year. The reason: solar cell producers have been reducing the silver content per cell (innovating with thinner silver pastes, etc.) to cut costs. Even so, solar remains a massive source of demand, consuming on the order of 200+ million ounces of silver annually. In 2025, roughly 17–18% of all silver demand came just from solar panel production. Other industrial uses – electronics, semiconductors, batteries, medical devices, and the expanding field of electric vehicles (EVs) – continue to grow. EVs use approximately 2–3 times more silver per vehicle than traditional combustion cars, thanks to high-current electrical components. With EV sales climbing and no real substitute for silver’s conductivity in many applications, this is a secular source of demand increase. Similarly, the rollout of 5G networks and the enormous power infrastructure for AI data centers are structural demand tailwinds for silver. Industry analysts note that silver is becoming one of the few metals with a steepening demand curve each year – renewables, electrification, and electronics are accelerating consumption. Even though 2025’s industrial demand dipped 2% due to one-off factors (economic uncertainty, thrifting at record prices), this is expected to be temporary. Underlying trends point to renewed growth ahead in industrial use, especially if prices stabilize at levels that industry can plan around. In fact, some of the thrifting gains (like reduced PV silver per watt) could eventually plateau, meaning volume growth in end-products will resume driving net silver demand higher.

Investment demand for silver was the real standout in 2025. Faced with rising inflation, geopolitical risks, and doubts about fiat currencies, investors flocked to silver alongside gold. Exchange-Traded Products (ETPs) that hold physical silver saw major inflows. In the first half of 2025 alone, silver-backed ETPs (like iShares Silver Trust, etc.) absorbed about 95 Moz of silver, pushing total global ETP holdings to 1.13 billion ounces. (For context, 1.13 billion oz is over 7 months of global mine output locked away in vaults.) By November, total ETF holdings were up ~18% year-to-date, an increase of roughly 187 Moz – the largest annual rise in silver ETFs since 2020. Once silver is vaulted to back these ETP shares, it is effectively taken off the market (it cannot be easily lent out or used to deliver against futures), exacerbating the physical supply squeeze. Bar and coin demand, the more traditional form of retail investment, was a mixed picture in 2025. Bar/coin demand actually fell about 4% to 182 Moz, a seven-year low. This was largely due to the U.S. retail market, where many small investors sold into the price rally (taking profits or unloading high-premium silver Eagles, for example). In contrast, retail investors in India and Europe continued buying – in India, despite record-high local silver prices, buyers accumulated silver in anticipation of further upside. Overall, the slight dip in bar/coin demand was more than offset by the surge in ETF holdings, leaving total investment demand significantly higher on the year. Silver’s unique appeal is that it straddles the line between an industrial commodity and a monetary asset. In 2025, the “monetary metal” aspect shone, as safe-haven and diversification flows poured in amid concerns about stagflation, rising government debt, and even the Federal Reserve’s independence. The U.S. government’s decision to officially designate silver as a critical mineral in 2025 added to silver’s investment narrative, as many saw it as validation of silver’s strategic importance.

In summary, fundamental drivers of silver are strong: structural supply deficits, firm (and growing) industrial usage, and resurgent investor appetite have all converged. Even the segments of demand that softened in 2025 (such as jewelry, silverware, and U.S. retail coin purchases) did so largely because prices rose so much, not due to long-term weakness. Silver jewelry demand, for instance, fell ~4% in 2025 especially in price-sensitive markets like India – yet that could quickly reverse if prices dip or stabilize. With supply unable to grow much in the short term, the supply/demand balance remains tight and tilted toward shortage. This backdrop provides fundamental support for elevated prices, though as 2025 showed, short-term financial market swings can temporarily overwhelm fundamentals.

Policy and Regulatory Impacts

Recent policy and regulatory developments have had a meaningful impact on silver’s market and are important to monitor going forward. One of the most consequential changes came from China, the world’s largest silver refiner. Starting January 1, 2026, China has implemented a new export control regime for silver, effectively treating it as a strategic resource on par with rare earth metals[2]. Rather than an outright ban, Beijing is using a strict licensing system: only 44 approved companies are authorized to export silver in 2026–2027[2]. This move “formalizes” silver’s status as a strategic material and gives Chinese authorities broad discretion over how much silver can leave the country, when, and to whom[2]. The policy shift was foreshadowed in late 2024 and comes amidst U.S.-China trade tensions – silver appears to be “the next lever” after rare earths in Beijing’s resource strategy[3].

The implications are significant because China is a major player in the silver supply chain. In the first 11 months of 2025, China exported over 4,600 tonnes of silver (~148 Moz) while importing only ~220 tonnes. These exports (roughly 12–15% of annual global supply) provided a critical supply relief to global markets in 2025. By tightening export approvals, China is reducing the availability of silver on the international market. Effectively, a large chunk of global refined silver supply now falls under Chinese governmental control. This has raised concerns for industries reliant on silver: solar panel manufacturers, electronics firms, defense contractors, etc., especially in the U.S., Europe, and India, which import silver. Business leaders reacted immediately – for example, Tesla’s Elon Musk publicly criticized the export curbs, noting silver’s importance in EVs and batteries. Reports have emerged of aggressive buying as users try to secure supply ahead of potential bottlenecks: one Canadian mining company (Kuya Silver) said Chinese buyers offered $8/oz above market to get metal, and an Indian buyer then bid $10 above spot – clear signals of tightening supply and panic buying. In short, China’s policy has “elevated silver to strategic status” and put global supply chains on notice. It was one of the factors propelling silver’s late-2025 spike, as market participants anticipated shortages – indeed, silver prices more than doubled in 2025, briefly crossing $80, partly on this development. Going forward, the export controls could keep the market on edge: any further restrictions (or relaxations) by Beijing will influence expectations for physical supply. It also underscores the new era of resource nationalism, where geopolitical strategy can directly affect commodity availability. Countries that depend on imported silver may now seek to diversify sources or encourage domestic refining, but in the near term there are limited alternatives to Chinese supply.

Another major factor looming over the silver market in early 2026 is the annual index rebalancing of commodity benchmarks, especially the Bloomberg Commodity Index (BCOM). Because silver’s price skyrocketed in 2025, its weight in these indices rose far above target. As of the start of January, silver futures made up roughly 9% of the Bloomberg Commodity Index, versus a target weight just under 4%. This means index-tracking funds must sell down a substantial portion of their silver holdings to realign with the new 2026 weights. Analysts estimate that during the scheduled five-day roll period (beginning Jan 8, 2026), billions of dollars worth of silver contracts could be dumped onto the market. This anticipated flow has many traders cautious. After a “record-breaking rally” last year, silver and gold are facing near-term selling pressure from this index reweighting[4]. The rebalancing is largely mechanical, but its impact can be very real: essentially forced selling by passive funds. Some projections suggest on the order of 100+ million ounces of silver might be sold by index funds in early January (if $100+ billion tracks BCOM, a ~5% reduction in a 9% position equates to ~$5 billion in silver, which at ~$60/oz is ~83 Moz; at ~$70/oz is ~71 Moz – on the same order as a full year of U.S. silver Eagle coin demand). This wave of supply could temporarily pressure prices lower and widen spreads. Market participants have been bracing for this “index washout” – it likely contributed to some of the late-December volatility as well, with traders front-running the rebalance by unwinding positions. History shows that such index-related moves are usually short-lived and present buying opportunities once the forced selling is done. Nonetheless, the scale this year is unusually large; analysts warn of a potential “dramatic repricing lower” for silver in the first half of January as this technical selling plays out. Both gold and silver could see elevated volume and volatility during the roll period. By mid-January, once index funds have finished adjusting, the market may find more organic direction.

Changes in exchange regulations and requirements have also shaped trading conditions. We already discussed the CME margin hikes that occurred due to high volatility. For instance, on Dec 30, CME raised initial margin on silver futures by a further 30%, bringing it to $32,500 per 5,000 oz contract – more than double the margin from just a few months prior. Such moves increase the cost of carrying large positions and can lead to position liquidations (both among longs and shorts) to meet margin calls. Some in the market viewed the aggressive margin increases as a form of circuit-breaker or cooling measure, aiming to curb speculative frenzy. Indeed, open interest in silver futures did pull back late in the year, suggesting some leveraged players stepped aside. Going forward, the CME and other exchanges will likely stay vigilant – further margin adjustments could happen if volatility stays extreme. Traders must be mindful that regulatory changes (position limit enforcement, price limit expansions, etc.) could be implemented if a disorderly squeeze occurs. There has even been chatter (albeit speculative) that if COMEX inventories were in danger of exhaustion, the exchange might consider altering delivery rules or encouraging cash settlement in lieu of physical delivery, as a last resort. There is no evidence of that yet, but it remains a theoretical tail-risk in a runaway squeeze scenario.

Broader government policies can also indirectly impact silver. For example, several countries have adjusted import/export duties on precious metals: India, a large silver consumer, has in the past tweaked import tariffs and could do so again to manage domestic prices (high duties sometimes spur smuggling or dampen demand). Meanwhile, the U.S. Federal Government adding silver to the critical minerals list (in November 2025) is largely symbolic but could pave the way for incentives to boost domestic mining or recycling. It also reflects a policy bias toward securing supply chains for silver, given its importance in solar energy (aligning with clean energy policy goals) and defense technology. Any future legislation that subsidizes solar/EV adoption or infrastructure could indirectly lift silver demand further. Conversely, if governments removed subsidies or if there were technology shifts (for instance, a breakthrough in photovoltaic tech that uses less or no silver), that could alter demand – though no such substitute looks viable in the near term.

In summary, recent policy actions – China’s export controls and commodity index rebalancing – are near-term headwinds for silver’s supply-demand balance. The former tightens supply (bullish medium-term, though potentially dampening industrial usage if shortages occur), and the latter creates a transient surge of supply (bearish short-term technical pressure). Regulatory moves like margin hikes have already induced volatility and will continue to be a factor in how the market behaves. For silver market participants, staying attuned to these policy signals is crucial, as they can catalyze significant price moves independent of underlying fundamentals.

Geopolitical and Macro Factors

Silver’s fortunes are closely tied to the broader macroeconomic and geopolitical backdrop. As both an industrial commodity and a monetary metal, silver is influenced by factors ranging from interest rates and currency values to safe-haven flows during crises. Here we consider some of the key macro drivers as of early 2026:

- Monetary Policy and Interest Rates (Fed outlook): The U.S. Federal Reserve’s policy is perhaps the single biggest macro factor for precious metals. In 2025, the Fed shifted from aggressive tightening to an easing bias – amid signs of economic strain and lower inflation, the Fed cut rates in the second half of 2025 (after having raised them sharply in 2022–23). This turn toward easier monetary policy helped send real interest rates lower and weakened the dollar, which in turn boosted silver and gold. By year-end, markets were expecting the Fed to continue with a dovish tilt into 2026. Heavy U.S. government refinancing needs and rising debt servicing costs make it challenging for the Fed to be overly hawkish. Indeed, Fed officials have signaled concern about over-tightening given fragile growth pockets. The assumption baked into many silver bulls’ outlook is that rates will either plateau or fall in 2026, removing a major headwind (higher rates increase the opportunity cost of holding non-yielding assets like silver). However, there is a risk of surprise: if inflation reaccelerates or the labor market stays hotter than expected, the Fed could turn hawkish again. A sharp rise in real yields would likely cool off precious metals quickly – this is seen as a key downside risk for 2026. That said, absent a drastic hawkish shift, monetary conditions seem broadly supportive. It’s also worth noting that in a scenario where the Fed eases because of recession fears, silver might benefit from safe-haven demand even if its industrial demand outlook dims. The net effect of Fed policy on silver is a balance between rate-driven dollar moves and growth-driven industrial demand. Currently, the bias is toward policy helping silver (via a softer dollar and lower yields), but this will be watched closely – FOMC meetings, inflation reports, and employment data in early 2026 are all potential catalysts for silver via their impact on Fed expectations.

- U.S. Dollar and Currency Markets: Silver, like most commodities, is priced in U.S. dollars on global markets. A weaker dollar typically lifts silver prices (and vice versa) as it makes silver cheaper in other currencies and tends to coincide with investor rotation into hard assets. In 2025 the USD index (DXY) fell ~9–10%, its worst year since 2017. This was a tailwind for silver – some analysts argue that part of silver’s rally was investors hedging against dollar debasement and currency weakness. If the dollar continues to slide in 2026, that would likely support further silver strength. However, if the dollar finds a floor or rebounds (say due to global risk aversion or relatively stronger U.S. growth), it could act as a headwind. One interesting observation late in 2025 was that silver and gold rallied even as Bitcoin (often dubbed “digital gold”) underperformed – Bitcoin ended 2025 slightly down, failing to keep pace with gold’s rise. This suggests that in the face of currency and geopolitical concerns, investors preferred traditional hard assets like gold/silver over crypto as a hedge. Continued weakness in major fiat currencies (not just USD, but also any issues with the euro, yen, etc.) could channel more safe-haven flows into precious metals. Currency markets in 2026 will be influenced by relative central bank policies and global growth trends – silver bulls are essentially betting that the era of low real rates and mild USD weakness persists.

- Geopolitical Tensions and Safe-Haven Demand: Geopolitics had a significant influence throughout 2025 and remains a wild card. The past year saw episodes of heightened tensions – from war and conflict risks to trade disputes – which often benefited precious metals. For instance, ongoing Russia-Ukraine tensions and instability in other regions can spur safe-haven buying of gold and silver. In 2025, periodic flare-ups in the Middle East and concerns around great-power competition (US-China) kept a level of risk premium in commodities (oil spiked at times, and metals caught bids on bad news). Silver typically correlates with gold in risk-off moves, although its industrial nature can complicate the reaction (e.g. a severe geopolitical shock that threatens global growth might cause silver to dip initially, even as gold rises, though eventually monetary easing responses can lift both). The trade war and strategic rivalry between the U.S. and China directly touched silver via export controls, as discussed. This is part of a broader theme: supply chains are being weaponized. If geopolitical fragmentation intensifies in 2026, one could imagine scenarios like additional export restrictions (China could tighten the screws further on silver or other critical metals), or Western countries imposing tariffs or quotas. Each such move could disrupt the physical market and cause price volatility. Conversely, any major de-escalation or peace deals can sometimes reduce safe-haven interest. For example, if a resolution to a conflict is reached (hypothetically, a lasting peace agreement in Eastern Europe), some of the geopolitical risk premium might bleed out of gold and silver prices. In late 2025, there were also “surprise” positive geopolitical developments (the Schwab market commentary referenced “tense trade negotiations followed by an AI tech détente, and even a peace deal” in 2025). Such improvements in the global mood could contribute to corrections in precious metals, as investors rotate back to risk assets. Overall, silver’s role as a safe haven was evident in 2025’s climate of “inflation and political polarization” – it thrives when confidence in paper assets erodes. That theme is likely to persist as long as global headlines are uncertain. Investors will be monitoring elections (e.g. the U.S. 2026 mid-term climate), geopolitical flashpoints (Taiwan, Middle East, etc.), and global cooperation (or lack thereof) on issues like trade and climate – all factors that indirectly drive safe-haven flows into silver.

- Global Economic Growth and Industrial Cycle: While safe-haven demand supports silver in times of crisis, silver’s industrial side ties it to the economic cycle as well. Signs of a global slowdown or recession in 2026 could have a mixed impact. On one hand, a slowdown would likely prompt central banks to ease (which is bullish for metals), but on the other hand it could dampen industrial demand for silver in areas like electronics, autos, and solar (bearish for consumption). So far, the global economy in late 2025 showed resilience in some areas but weakness in others (“uneven pockets of growth” were noted). If 2026 were to see a sharper downturn (for instance, if high interest rates from earlier tightening finally bite or if there’s a credit event), base metals and industry-linked commodities might slump. Silver could initially get caught in such a downdraft, as part of a general commodity sell-off. However, unlike pure base metals (like copper), silver’s dual role means that monetary loosening and stimulus during a downturn could quickly rekindle investment demand. The COVID crash of 2020 is instructive: silver prices plummeted in the initial liquidity crunch, then staged a massive rally when unprecedented monetary and fiscal stimulus followed. In late December 2025, we saw a mini-version of this: a global equity sell-off caused a scramble for cash and even gold and silver were sold off heavily for a day, illustrating that in a severe liquidity crunch, no asset is immune. But that kind of selling can be short-lived. The forward-looking view is that if a recession or market stress occurs, central banks and governments will respond with easing measures, potentially setting the stage for another surge in safe-haven and inflation-hedge demand for silver. Conversely, if global growth accelerates more than expected (a “soft landing” scenario with strong industrial activity), that would boost the industrial demand for silver (more solar installations, more electronics sales, etc.), but it could also lead to higher interest rates or less urgency for monetary stimulus, which might cap the investment side. Thus, silver’s outlook straddles these macro outcomes – it tends to do well in inflationary or stagflationary environments, or periods of currency debasement, whereas a scenario of robust growth with rising real yields could be challenging.

In summary, macro/geopolitical conditions remain a two-edged sword for silver. The late 2025 environment – characterized by high inflation concern, falling real yields, a weaker dollar, and plentiful geopolitical risks – was nearly ideal for silver’s bull run. Going into 2026, many of those elements are still in play (moderating inflation but still above target, central banks leaning dovish, geopolitical undercurrents). However, the interplay of Fed policy vs. growth will be crucial. A cautious Fed and persistent global uncertainties point to continued safe-haven and diversification flows into silver, while any shocks (positive or negative) will create volatility. Investors in silver are effectively betting that the world in 2026 continues to be “inflationary, noisy, and structurally fragmented,” to borrow phrasing from one outlook – conditions under which silver tends to shine.

Forecasts and Risk Scenarios

Looking ahead, the consensus among many market analysts is that silver’s fundamental backdrop supports elevated prices into 2026, but the road will be volatile. Most major bank forecasts foresee silver consolidating at higher levels than in previous years. For instance, UBS recently raised its mid-2026 silver target to $55/oz (with the possibility of $60+ if conditions stay favorable). Bank of America is somewhat more bullish, expecting silver to approach $65/oz by 2026 (with an average around $56). These forecasts (mid-$50s to mid-$60s) suggest that institutions see the late-2025 price surge as at least partly sustainable. They are “conservative” relative to current prices in the high $60s, implying an expectation of some mean reversion or stabilization rather than endless ascent. However, there are also more bearish and cautious voices: Citi has projected that silver could pull back to the low $40s in the absence of new catalysts, essentially viewing the recent rally as overextended. Such a retracement could materialize if, for example, the physical tightness eases and investment flows cool (perhaps due to a more hawkish Fed or resolution of supply-chain issues). On the ultra-bullish end of the spectrum, some independent analysts and investors speculate about “triple-digit silver” in the coming years – for instance, one outlook from Incrementum AG argued that $100+ silver is a “certainty” eventually, given monetary trends. While mainstream forecasts do not assume such extreme outcomes without further catalysts, they do acknowledge the potential for higher prices. The Silver Institute noted that historically, when silver breaks previous highs (as it did in 2025), it has often gone on to double again in the ensuing bull cycle. Scenarios where silver pushes to $75, $80, or beyond in 2026 typically involve significant bullish catalysts: e.g., a major currency crisis, a new surge of inflation prompting negative real yields, or an exacerbation of supply shortages (a “run” on physical silver). On the other hand, a slide back to $40 would likely require a combination of bearish developments: perhaps a relatively quick resolution of the shortage (through demand reduction or a surge of supply from stockpiles), and a macro turn (rising real rates or a strong economic rebound reducing safe-haven interest).

Let us outline some key catalysts and risk scenarios for the short-term outlook (Q1 2026, especially January settlement):

- Index Rebalancing – Forced Selling (Near-Term Risk): As discussed, the imminent Bloomberg Commodity Index rebalance is expected to unleash a wave of forced selling of silver futures in early January. This is a known event, but its impact could still be jarring. There is a risk of a temporary price air-pocket where silver falls sharply in a short time as index funds unload positions. Some analysts have likened this to a “lagging anchor” on silver’s price as the new year begins. The base-case expectation is that silver could see additional downside pressure through the second week of January until the rebalance is done. Notably, some of this may already be priced in – the late-December drop in prices could partly reflect front-running. Nonetheless, traders are cautious that we could retest support levels (perhaps low-$60s or even high-$50s) during this period of artificial selling pressure. Volatility is likely to remain elevated while this plays out. For longer-term bulls, any index-driven dip might be viewed as a buying opportunity, since it is not due to fundamental weakness. Once this forced selling abates, the absence of that constant supply could allow prices to rebound if underlying demand stays firm.

- Physical Squeeze and Backwardation Scenarios: On the bullish side, one risk (to the upside) is that the physical silver squeeze intensifies again. The December COMEX episode showed how quickly the system can come under strain. Looking ahead to the March 2026 COMEX contract (a major delivery month), if we see another large wave of delivery demands, it could spark renewed backwardation and panic among short sellers scrambling for metal. There are rumors that some large entities (possibly a bullion bank or a consortium of industry users) might stand for delivery in size in March, aiming to test the exchange’s resolve. If COMEX registered inventories slide toward critically low levels (say, approaching only 20–30 Moz available), it could trigger a “run” on the bank mentality, where everyone rushes to grab physical while they still can. In such a scenario, silver prices could spike violently higher, potentially retesting the $80 level or more. The market is wary of the possibility of a self-reinforcing short squeeze: backwardation itself incentivizes immediate buying (why wait if it’s only getting more expensive to find metal later?), which can worsen the shortage. Signs to watch: the COMEX daily inventory reports, LBMA vault data (with a month lag), lease rates, and spot-premium over futures. If backwardation starts widening again (e.g. spot $1+ over futures consistently), it’s a clue that a second squeeze may be unfolding. This is a low-probability but high-impact risk – effectively the “silver squeeze 2.0” scenario – which could propel prices to uncharted territory (some bulls throw out targets like $100 in a blow-off). The flip side risk is if backwardation resolves quickly (through an influx of supply or softening demand), prices might languish.

- Supply Chain Shock or Disruption: Another risk factor is a supply shock in the silver market – this could be positive or negative for price depending on direction. A negative price shock could occur if, for example, a large holder (such as a sovereign or a major ETF) decides to unload physical silver into the market. While unlikely in current conditions, one could imagine a scenario where, say, some central entity (maybe a country that has a strategic stockpile) sells silver to stabilize prices or raise cash. Conversely, a positive shock (price-bullish) could happen if a major source of silver suddenly goes offline. For instance, if political instability or strikes in a key mining country like Mexico or Peru disrupt production significantly, or if logistical issues impair the refining and delivery of silver (as happened during COVID lockdowns), the supply crunch could worsen. We’ve already seen a policy-driven supply shock with China’s export control – if that is further tightened (e.g., China could reduce export quotas mid-year if internal demand rises or as retaliation in trade disputes), it would remove even more metal from the global pool. Additionally, we should consider the time lag of current high prices on supply: high prices can flush out some extra supply in the short term (through more scrap recycling or producers hedging and selling forward more silver). If silver stabilizes around $60–70, some scrap that was previously uneconomic to collect may enter the market (jewelry melting, etc.), and some miners might increase hedging (locking in these high prices for future output, effectively adding selling pressure in the forward market). These factors could temporarily augment supply and cap prices – a “supply response” risk to the rally. So far, recycling upticks have been modest, but if silver stays at multi-decade highs, that response could grow.

- Passive Investment Flows (beyond BCOM): Apart from the commodity index rebalance, there is the question of ETF flows and other passive investment. In 2025, ETFs added a lot of silver; a risk is that in 2026 we could see the opposite if sentiment sours. For example, if silver’s price momentum stalls or reverses, momentum-focused funds or trend-following strategies might start unwinding positions, leading to outflows from silver ETFs (which would then sell physical silver). There’s also the risk of profit-taking by large investors – some hedge funds or family offices that accumulated silver under $30 might decide that $60+ is a good exit and sell their holdings or metal. A particular concern is if any leveraged speculative players built up sizable longs during 2025 – should they get forced out (by margin hikes or losses elsewhere), it could exacerbate downswings (the Dec 29 crash was partly attributed to investors liquidating metals to cover stock losses). Essentially, after a parabolic rise, the market is more fragile to any wave of selling. This is a near-term risk for Q1.

- Macroeconomic Swings: From a broader lens, certain macro scenarios present risks. A faster-than-expected economic rebound (contrary to many forecasts) could lead to higher yields and a stronger dollar, pressuring silver. Alternatively, a significant recession or deflationary shock could initially hurt industrial demand more than it helps safe-haven demand, at least until policy responses kick in. We also have to watch inflation itself – if inflation in 2026 drops back to very low levels (say below 2% sustainably) and inflation expectations recede, the urgency to hold precious metals might diminish among some investors. Many allocators increased precious metals in 2025 as an inflation hedge; if that narrative fades, some of those flows could reverse.

Considering all the above, what is a reasonable short-term outlook for January 2026? Most analysts expect continued consolidation with high volatility. The price may trade in a wide range – possibly something like $\$$55–$75 – as the market searches for a new equilibrium after the dramatic year-end moves. In the bearish short-term case, the index rebalance and any residual deleveraging could knock silver back into the $50s before strong buying interest re-emerges. In the bullish short-term case, any sign that the selling is absorbed and physical tightness persists (e.g. stable or rising premiums) could quickly send silver back above $70. It’s notable that even after the late-Dec sell-off, silver largely held above the high-$40s support that was noted by the Silver Institute as a sign of underlying strength. That suggests solid buying on dips.

Several potential catalysts in January deserve attention: the U.S. CPI inflation report (due mid-month) which could sway Fed expectations; the Fed’s late-January FOMC meeting, where any commentary on the rate path will move markets; and any fresh data on COMEX deliveries or Asian demand around the Lunar New Year (Chinese New Year in Feb can sometimes boost precious metal buying in Asia). Also, keep an eye on industry purchasing – if electronics or solar firms see the price dip due to financial flows, they might seize the chance to lock in supply, effectively supporting the market.

Conclusion and Outlook for Silver in January 2026

In conclusion, the global silver market as of January 2026 is defined by high prices, tight supplies, and cross-currents of opposing forces. On one side, strong fundamentals – multi-year supply deficits, robust industrial demand (from the likes of solar and EVs), and eager investment buying – provide a solid foundation that pushed silver to all-time highs in late 2025. Exchange inventories are depleted and the market has periodically flipped into backwardation, indicating that physical silver is in short supply. Policy actions like China’s export controls only reinforce the supply constraints, potentially setting the stage for continued tightness. Meanwhile, macro tailwinds – a softer dollar, lower interest rates, and geopolitical uncertainty – continue to support safe-haven demand for silver alongside gold. These factors suggest that silver will retain a bid on dips and that the medium-term bias remains upward. Indeed, major forecasters see prices averaging in the mid-$50s or higher this year, above any level sustained in the 2010s.

On the other side, near-term headwinds and risks could inject volatility and possibly spur corrections. The most immediate is the forced selling by index-rebalancing funds in early January, which could lead to a transient oversupply on paper markets. Additionally, the sheer magnitude of silver’s 2025 rally – +128% by one measure – invites the possibility of further profit-taking or technical pullbacks. The market has also become more fragile to liquidity events, as shown by the late-December flash crash when a rush for cash caused even precious metals to plummet briefly. Such episodes remind investors that silver’s notorious volatility cuts both ways. Furthermore, any shift in the macro narrative (e.g. a hawkish Fed surprise or rapid improvement in risk sentiment that lessens safe-haven interest) could temper silver’s ascent.

Our outlook for January 2026 is cautiously optimistic, with an expectation of choppy, range-bound trading in the short term before the bullish fundamentals reassert. The first half of January may see silver under pressure, potentially testing lower support levels, as the market digests the BCOM index rebalance and lingering year-end positioning effects. Once that selling is absorbed (by mid-January), we anticipate that physical demand and bargain-hunting will likely shore up prices. Any price dip toward the $50-$55 zone is likely to be met with strong buying interest from both industrial users (locking in cheaper material) and investors who missed the initial rally. Conversely, upside moves toward $75+ might be self-limiting in the very near term, as producers could take the opportunity to hedge and some investors might trim positions. Thus, a wide trading band could prevail in the coming weeks.

By the end of January (and looking into the first quarter), the direction of the next significant move will hinge on fresh information: Is the physical market still tightening (e.g. continued drawdowns, high lease rates) or has it calmed? What signals are coming from the Fed meeting? And has the bulk of index-related selling finished without breaking the market’s uptrend? Given the current evidence, the base case is that silver will emerge from the January volatility still well-supported, with prices likely settling in a higher equilibrium than pre-2025. In other words, even if silver doesn’t immediately resume its meteoric rise, the market seems to have “repriced” to a new range reflecting the structural deficits and strategic value of the metal.

In summary, silver enters 2026 in a position of strength, albeit with a bumpy road in the short run. The market is undergoing a kind of tug-of-war: paper-driven corrections versus physical-driven rallies. Our analysis suggests that after some consolidation, the bullish forces (supply tightness, strong demand, investor diversification, and accommodative macro policy) are likely to prevail over the course of the year, barring any major policy reversal or economic shock. Market participants should brace for continued high volatility and monitor the key indicators and events highlighted above. By keeping an eye on inventory levels, futures spreads, and macro signals, one can get a gauge of whether the next move is a breakout to the upside or a deeper corrective dip.

Outlook: For January 2026, we expect silver to remain volatile but generally elevated, with a bias that any near-term dips will be relatively short-lived. Once the transitory selling pressures abate, silver could stabilize and begin a recovery towards the mid-$60s or higher later in the month, especially if safe-haven flows resume. The balance of risks includes further sharp swings, but with fundamentals on silver’s side, the metal is poised to continue being one of the most closely watched (and potentially rewarding) assets in the commodity space as 2026 unfolds. In the words of one commodity desk, “silver has finally awoken” – and despite the rough and tumble start to the year, its prospects remain bright in this new regime for precious metals.

Sources: Silver Institute, World Silver Survey 2025; Reuters (Dec 30, 2025); Seeking Alpha News (Jan 3, 2026)[4]; Charles Schwab Market Commentary (Jan 2, 2026); IG Commodities Outlook 2026; Moneycontrol (Jan 2, 2026); Copygram trading blog (Dec 2025); Mining.com/Bloomberg (Dec 31, 2025); Texas Precious Metals report (Dec 29, 2025); GoldSilver.com forecasts; LBMA vault data; Investing.com analysis (Oct 2025).

[1] Comex Silver Ends the Year 142.34% Higher at $70.134 — Data Talk

[2] [3] Silver is the new rare earth: What China’s export controls really change

[4] Silver and gold facing near-term selling pressure (XAGUSD:CUR) | Seeking Alpha