October 21, 2025

ASML Holding N.V. – Long-Term Investment Analysis

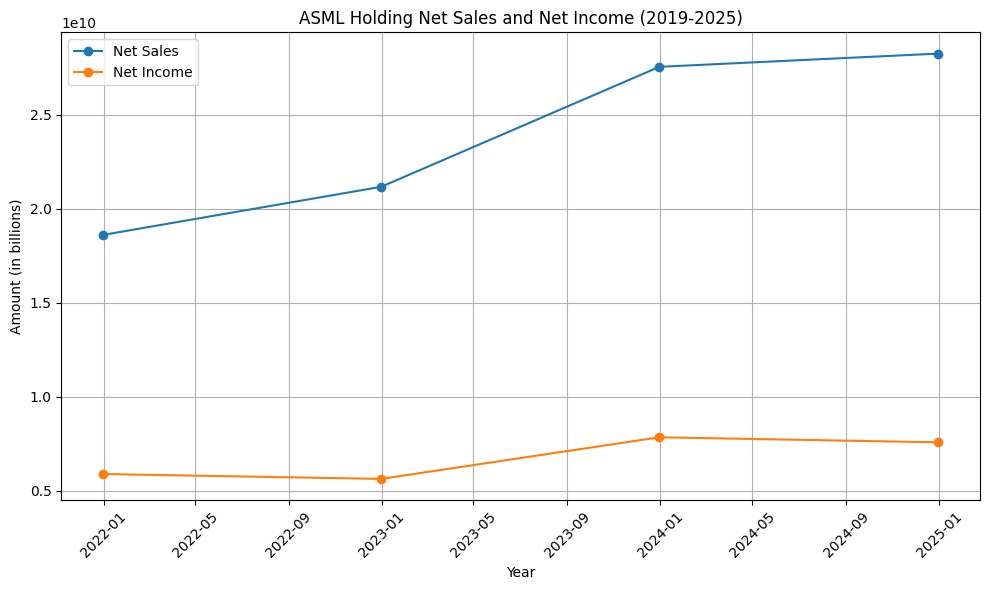

ASML’s net sales and net income from 2019 to 2023 (in € billions). The company’s revenue has climbed impressively over the past five years, reaching a record €27.6 billion in 2023[1] – more than double its 2019 sales of €11.8 billion[2]. Net profit has risen in tandem, from €3.6 billion in 2020 to about €7.6 billion by 2023, reflecting robust profitability[3][4].

ASML has delivered strong growth and solid financial metrics over the last five years. Revenue expanded from €11.8 billion in 2019 to €27.6 billion in 2023[1][2], a compounded annual growth rate of roughly 23%. This growth was not linear – sales jumped notably in 2021 (+33% YoY) and 2023 (+30% YoY) amid surging demand for semiconductor equipment[5][1]. Even 2022, a year of industry cyclicality, saw record sales of ~€21.2 billion (up ~14% YoY)[6]. On the earnings side, net income grew from €2.6 billion in 2019 to approximately €7.6 billion in 2023, with net profit margins improving to the high-20s%[7][4]. For example, 2021 benefited from higher operating leverage – net income reached €5.9 billion (≈32% net margin)[8] – while 2022 margins dipped slightly before rebounding in 2023 as profitability improved again[9][4].

Profitability and margins: ASML’s gross margins have strengthened into the ~50%+ range in recent years. Gross margin rose from 44.7% in 2019 to 52.7% in 2021 as product mix and volume improved[7][10]. In 2022, gross margin moderated to ~50.5%[11], then ticked up to 51.3% in 2023 on higher EUV volume and easing supply constraints[1]. Operating margins have similarly been healthy (30–35% range in recent years), underpinned by strong pricing and high demand for leading-edge tools. ASML converted this into high earnings per share, which nearly doubled from €8.49 in 2020 to about €19.91 by 2023[9][12], reflecting both profit growth and share buybacks. The company has also steadily returned capital to shareholders (e.g. €3.3 billion via dividends and buybacks in 2023) while maintaining a robust balance sheet[13].

R&D investment has grown substantially as ASML reinvests to sustain technology leadership. Annual research and development spending doubled from roughly €2.0 billion in 2019 to €4.0 billion in 2023[14]. This represents about 14–15% of sales devoted to R&D, a reflection of the technological intensity of ASML’s business. Notably, 2023’s R&D spend (€4.0 billion) was 102% higher than 2019’s level[14], with major projects including next-generation EUV (High-NA) and continued DUV improvements. This high R&D commitment supports ASML’s long-term growth by ensuring a pipeline of cutting-edge products. Meanwhile, capital expenditures have also risen to expand manufacturing capacity and support growth. Capex was around €0.9 billion in 2021[15] but increased to over €2 billion by 2023[16] as ASML built out production capability (e.g. to produce more EUV machines). Despite these investments, ASML continued to generate positive free cash flow (≈€3.2 billion in 2023)[4], highlighting a strong cash-generative business even while spending for future growth. Overall, the last five years show a company combining rapid revenue growth (sales more than doubled since 2018) with high margins and reinvestment, a profile that has bolstered its financial position going into the future.

| Key financial metrics (US GAAP) | 2019 | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|---|

| Net Sales (€ billions)[2][1] | 11.8 | 14.0 | 18.6 | 21.2 | 27.6 |

| YoY Sales Growth | – | +18% | +33% | +14% | +30% |

| Gross Margin[7][1] | 44.7% | 48.6% | 52.7% | ~50.5% | 51.3% |

| Net Income (€ billions)[7][12] | 2.59 | 3.55 | 5.90 | ~5.6 | 7.60 |

| R&D Expenses (€ billions)[17][14] | ~2.0 | ~2.2 | 2.5 | 3.3 | 4.0 |

| Capital Expenditures (€ billions)[15][16] | ~0.8 | 0.96 | 0.90 | 1.28 | 2.16 |

(Figures for 2019–2022 are rounded; 2022 net income is approximate. Source data from ASML annual reports and press releases.)

Position in the Semiconductor Equipment Industry

ASML occupies a unique and dominant position in the semiconductor equipment landscape. It is the leading (and only) supplier of cutting-edge lithography systems, especially in advanced photolithography. In fact, ASML has a near-monopoly in extreme ultraviolet (EUV) lithography tools – a critical technology for manufacturing the most advanced chips – with no direct competitors in EUV. Its only competition in lithography comes from two Japanese firms, Canon and Nikon, in the older deep ultraviolet (DUV) segment[18]. Even there, ASML is far ahead: Canon holds about 8% of the overall lithography equipment market and Nikon about 6%, versus ASML’s commanding share (over 85%)[18]. Neither Canon nor Nikon has been able to commercialize EUV, leaving ASML as the exclusive provider of EUV scanners for leading-edge chip fabrication[19]. This technological lead has made ASML an essential supplier to top chipmakers. For perspective, ASML’s EUV machines (priced ~$150–200 million each) are so critical that they enabled ASML to win a 30-year race for EUV dominance, granting it a virtual monopoly in that space[20]. Canon and Nikon continue to supply DUV lithography tools (e.g. for mature process nodes), but they cater to niches and trailing-edge needs. Canon is experimenting with an alternative nanoimprint lithography approach to potentially compete in certain markets[21][22], but this technology is still in early stages and not a mainstream threat to ASML’s EUV/DUV portfolio. Overall, in the core arena of lithography, ASML is by far the industry leader, with a wide moat around its EUV technology.

Beyond lithography, it’s useful to compare ASML with other major semiconductor equipment companies that specialize in different process areas. Applied Materials (AMAT) and Tokyo Electron (TEL) are two such peers often considered alongside ASML, even though they do not compete with ASML in lithography directly. Applied Materials is the largest semiconductor equipment vendor by broad revenue, offering equipment for deposition, etching, chemical-mechanical polishing and more. In fiscal 2023, Applied Materials had record revenue of $26.52 billion (≈€24 billion)[23], comparable to ASML’s size. Applied holds roughly 20% of the overall wafer-fab equipment market, making it a versatile one-stop supplier for chip fabs[24]. Its strength lies in covering many steps of chip manufacturing (thin-film deposition, etch, etc.), whereas ASML focuses on lithography. Tokyo Electron, based in Japan, is another top-tier equipment maker with a broad portfolio (plasma etch, deposition, cleaning, and specialty tools). TEL’s revenue was around ¥2.2 trillion in 2023 (~$14 billion)[25]. It ranks roughly #4 globally among chip equipment firms by sales, alongside ASML, Applied Materials, and Lam Research[26]. Importantly, Tokyo Electron is also a key partner to ASML – it supplies lithography coater/developer systems that work in tandem with ASML scanners. TEL dominates the coater/developer market with ~90% share and provides the track systems that are integrated with ASML’s EUV/DUV tools[27][28]. This close partnership (ASML and TEL often coordinate their tools for customers) creates a barrier to entry for others[28]. In essence, ASML, Applied Materials, Lam Research, Tokyo Electron, and KLA constitute the top five, controlling ~75% of the semiconductor production equipment market[26]. Each has its specialization: ASML in lithography, Applied in deposition/etch, Lam in etch and deposition, TEL in multiple areas (esp. coater/etch), and KLA in inspection/metrology.

Despite their large size, Applied Materials and Tokyo Electron are more complementary than directly competitive to ASML. They do not sell lithography systems; instead, they compete among themselves in other segments (etch, deposition, etc.) and depend on lithography advances (often provided by ASML) to enable next-generation chips. From an investor perspective, ASML’s competitive moat is distinct: it holds unrivaled intellectual property and know-how in high-end lithography (including patents, proprietary technologies in optics and light sources, and a 30+ year development lead in EUV[20]). This has made ASML an indispensable supplier to chipmakers like TSMC, Samsung, and Intel – to the point that those companies’ ability to progress to next process nodes depends on ASML’s machines. Competitors like Canon and Nikon remain active mostly in less advanced or specialty lithography markets (for example, Canon’s tools are used for older node production or in niche applications like flash memory patterning via nanoimprint)[19][22]. Given ASML’s technology edge, its competitive position is very strong. It’s effectively a one-of-a-kind provider in the most critical segment of chip manufacturing equipment. Its relationships with customers are more collaborative than adversarial (customers often pre-pay or co-invest in R&D for new ASML tools), and even its “competitors” (like TEL) are often partners in delivering integrated solutions. This unique standing within the semiconductor equipment industry underpins ASML’s long-term growth potential and pricing power.

Technological Leadership: EUV, DUV and Innovation Drivers

ASML’s long-term growth is fundamentally supported by its technological leadership in lithography, especially in EUV (extreme ultraviolet) and advanced DUV (deep ultraviolet) lithography. Lithography is the process of printing tiny circuit patterns onto silicon wafers using light, and it largely determines how small and powerful chips can become. In this domain, ASML has consistently pushed the frontier of what is technologically possible, creating a virtuous cycle of innovation fueling its growth.

EUV Lithography – a game-changer: ASML’s crown jewel is its EUV lithography platform, which uses 13.5 nm wavelength light to etch extremely fine features on chips. ASML was the first (and so far only) company to commercialize EUV tools, after decades of research and close collaboration with partners (like Zeiss for optics). EUV started contributing to chip production in the late 2010s, and by 2021 ASML’s customers had produced over 59 million wafers using EUV systems (up from 26 million a year prior)[29], illustrating rapid adoption. Today, EUV is indispensable for leading-edge semiconductor nodes (e.g. 5 nm, 3 nm processes used in high-end processors and memory chips). ASML’s EUV machines (the “NXE” series) enabled chipmakers to continue shrinking transistors per Moore’s Law when older optical methods reached their limits. A single EUV scanner can cost over $150 million, but it replaces multiple DUV patterning steps, making it both technically and economically critical for advanced chip fabrication. ASML has continuously improved EUV tool performance – for instance, the current NXE:3600D system can expose ~160 wafers/hour with high reliability. In 2023, ASML shipped the first modules of its next-generation High-NA EUV system (EXE:5000 series)[30]. “High-NA” EUV increases the numerical aperture of the optics from 0.33 to 0.55, a major innovation that will enable even smaller chip features into the latter half of this decade[30]. The EXE:5000 (High-NA EUV) is slated for pilot use in ~2025 and is a key part of ASML’s roadmap to extend lithography to 2 nm and beyond. Successfully deploying High-NA EUV will further cement ASML’s technological lead and provide a new growth engine as customers invest in these cutting-edge tools for future node development. ASML’s dominance in EUV is a huge long-term growth driver – as long as demand for more powerful, efficient chips (for AI, data centers, smartphones, etc.) keeps rising, chipmakers will need ASML’s EUV systems to manufacture those chips at the smallest geometries.

DUV Lithography – continuing advancement: In addition to EUV, ASML also leads in deep ultraviolet lithography (using 193 nm light), which remains workhorse technology for many chip layers and for mainstream chip fabrication. ASML produces immersion DUV scanners (TWINSCAN NXT series) that are state-of-the-art for non-EUV lithography. The company hasn’t stood still in DUV: it introduced the TWINSCAN NXT:2100i in 2022, a new high-throughput immersion scanner for critical DUV layers[31]. In 2023, ASML rolled out further DUV improvements – for example, the NXT:1980Fi immersion system to boost productivity on mid-critical layers, and the NXT:400M dry lithography system for the i-line segment (mature processes) with improved throughput[32]. ASML is also developing next-generation immersion tools like the NXT:2150i, indicating that DUV will continue to evolve alongside EUV[32]. These DUV innovations are important because many chips (analog, sensors, power chips, legacy nodes) will still be made with DUV for years, and even at advanced nodes, DUV and EUV are used together (multiple patterning, less critical layers, etc.). By continuously improving DUV lithography (higher wafers per hour, better overlay accuracy, etc.), ASML ensures it retains a strong market across all segments of lithography, not just the extreme leading edge. This broad portfolio approach – serving both cutting-edge EUV needs and high-volume DUV needs – supports ASML’s long-term growth by capturing a wide range of customer requirements.

Holistic lithography and other technologies: ASML also emphasizes a “holistic lithography” strategy – complementing scanners with software and metrology to maximize chipmakers’ yield and performance. It sells computational lithography software (from its acquisition of Brion) that helps optimize mask designs and simulate lithography outcomes, and metrology/inspection systems that measure patterns for errors. For instance, ASML introduced the YieldStar 500 optical metrology tool in 2023, offering improved overlay and focus measurement accuracy for advanced nodes[33]. ASML’s subsidiary HMI supplies e-beam inspection systems, and the company is investing in multi-beam e-beam metrology to address future process control challenges[34]. In 2023, ASML noted progress in its high-voltage e-beam systems, moving them closer to production use[35]. By developing these side technologies, ASML deepens its engagement with customers – not only providing the exposure tools, but also the means to fine-tune and verify the results, which is increasingly valuable as chips become more complex. The synergy between scanners, metrology, and simulation software creates a high value-add ecosystem that competitors find hard to match. It also provides ASML with additional revenue streams (services, software, and options sales now contribute significantly to sales[36]).

Innovation pipeline: ASML’s hefty R&D spending (over €4 billion in 2023) is focused on several core areas: advancing EUV for high-volume manufacturing (e.g. source power increases, uptime improvements), developing High-NA EUV for next-gen lithography, improving DUV throughput and accuracy, and exploring new applications (like adjacent markets in inspection). The company has explicitly stated that its most significant R&D investments are directed to EUV (including High-NA) and to supporting its holistic lithography solutions[37]. This constant innovation supports long-term growth by ensuring ASML’s tools remain indispensable. For example, as AI and high-performance computing drive demand for chips with billions more transistors, ASML’s future tools (High-NA EUV) will be what makes those chips possible – creating a pipeline of future revenue. Additionally, ASML is exploring concepts beyond traditional lithography – from new light source technologies to collaborating on alternative patterning techniques – to make sure it stays ahead of any potential disruptive shifts. So far, no viable alternative to optical lithography has emerged at scale; technologies like nanoimprint or directed self-assembly are being researched (Canon’s nanoimprint is one example[21]), but they complement rather than replace mainstream lithography at present. ASML’s track record of execution on complex engineering feats (bringing EUV from theory to factory floor) suggests it is well positioned to maintain its technology leadership. In summary, ASML’s core technologies – EUV lithography leadership, continual DUV innovation, and a holistic approach with metrology/software – form the backbone of its long-term growth strategy. These give ASML both a competitive moat and a clear runway as the semiconductor industry is expected to keep expanding (driven by megatrends like AI, 5G, automotive electronics, etc., which all require more advanced chips)[38][39].

Key Risk Factors and Long-Term Considerations

While ASML’s prospects are strong, investors should be mindful of several risk factors that could impact the company’s long-term performance. The semiconductor industry is dynamic and not without uncertainties. For ASML, the most significant risks include geopolitical dependencies, supply chain vulnerabilities, customer concentration/cyclicality, and regulatory constraints, among others.

- Geopolitical and Export Control Risks: ASML sits in the crossfire of global trade and geopolitical tensions because of its critical technology. Notably, export restrictions (primarily driven by US-China tensions) have already affected ASML’s business with China. The Dutch government – under pressure from the US – has since 2019 imposed tightening limits on ASML’s ability to ship its most advanced tools to China[40]. ASML has never been allowed to sell EUV systems to China, and as of 2023 even certain high-end DUV immersion tools require export licenses. In early 2024, ASML confirmed it had to cancel some China-bound DUV shipments due to new Dutch export rules[41]. China has been a significant market for ASML’s less advanced tools (in 2022–2023, Chinese customers rushed to order DUV machines before new curbs; ASML expects China could account for over 25% of its sales in 2025 if unrestricted)[42]. Losing access to Chinese customers – whether through stricter Western export bans or Chinese efforts to localize tools – poses a risk to ASML’s revenue growth[42]. In the near term, export controls mean ASML’s growth is capped in China, and the company must depend more on other regions. Geopolitically, Taiwan and South Korea (home to TSMC, Samsung) are also crucial – any instability (e.g. a China-Taiwan conflict) could disrupt the entire chip supply chain and, by extension, ASML’s orders. Geopolitical pressures thus represent a structural risk: they likely won’t derail ASML’s dominance (since its tech is still unmatched), but they can limit its accessible market and complicate its supply chain. Furthermore, China is investing heavily in developing its own lithography equipment to reduce reliance on ASML. While replicating ASML’s EUV tech is a monumental task, state-backed Chinese firms (like SMEE) could, over time, narrow the gap in older lithography generations[43]. This could eventually create low-end competition or erode some service business in China. In summary, geopolitical risk is the biggest external uncertainty for ASML – it is not existential (ASML’s tech lead is secure for now), but it introduces demand variability and constraints that investors must watch.

- Supply Chain and Single-Source Dependencies: ASML’s products are extraordinarily complex, and the company relies on a global network of specialized suppliers for critical components. This can create vulnerabilities if those suppliers face disruptions. A notable example is ASML’s dependence on Carl Zeiss SMT for the precision optical lenses and mirrors in its lithography systems. Zeiss is essentially the sole provider of the ultra-high-end optics needed for ASML’s scanners. This “single-source dependency” means any hiccup at Zeiss (capacity issues, technical problems, geopolitical restrictions on optical technology) could delay ASML’s production – a clear supply chain vulnerability[44]. Similarly, ASML’s EUV light source technology comes from Cymer (a company ASML acquired), and critical sub-components come from niche suppliers around the world (for instance, mirror blanks from Japan, specialized lasers from the US, etc.). The COVID-19 pandemic illustrated these risks: in 2021–2022 ASML struggled with component shortages and logistics delays, which limited how fast it could ship machines[38]. The company had a significant backlog as supply bottlenecks constrained output[38]. Although those constraints eased in 2023, any future global supply shocks (natural disasters, trade wars affecting a supplier’s country, etc.) could similarly impact ASML. The fragility of the EUV supply chain is well-noted – EUV tools require hundreds of thousands of parts and extremely precise manufacturing, so there are only a few qualified suppliers for many parts[45][44]. ASML is mitigating this by working closely with suppliers (it sometimes helps fund supplier expansions or holds strategic inventory)[46]. Nevertheless, investors should realize that ASML’s output (and margins) could be hurt by supply chain issues outside its direct control. In short, ASML’s success is intertwined with a robust supply chain; any weakness or concentration in that chain (like the Zeiss optics bottleneck) poses a risk to executing customer orders on time.

- Customer Concentration and Industry Cyclicality: ASML’s customer base is relatively small and highly concentrated – essentially all the leading semiconductor manufacturers. Its top customers include TSMC, Samsung, Intel (for logic), and memory makers like SK Hynix and Micron. In 2024, ASML’s top two customers accounted for 31% of revenue[47] (likely TSMC and Samsung). This concentration means ASML’s fortunes are tied to the capital spending cycles of a few large chipmakers. The semiconductor industry is known to be cyclical – periods of high demand and fab expansions are often followed by downturns where capacity is underutilized and chipmakers cut equipment orders. ASML is not immune to these cycles. For example, if a major customer like Intel or a memory manufacturer sharply reduces its capex in a given year (due to oversupply or a drop in chip prices), ASML’s order intake and revenue can dip. We saw this in the early 2010s with lithography slowdowns and more recently in 2019 when a memory downturn cooled equipment demand. The 2023–2024 period saw some softness in memory sector orders and inventory digestion in certain segments, though ASML managed to offset some impact by filling orders from other regions (like China)[48]. The key point is ASML’s revenues can fluctuate with chip demand cycles: when chip demand cools, customers may delay purchases (ASML’s sales fell ~10% in 2019 during a memory downturn, for instance). That said, ASML tends to be more resilient than many peers in downturns – leading-edge logic players often continue investing (or delay rather than cancel orders), and the secular trend (more chips needed in the long run) has meant backlogs eventually translate to revenue[49][50]. Nonetheless, investors should expect periodic volatility. The concentrated customer base also raises a strategic risk: if one of ASML’s top customers (say Intel) were to significantly fall behind or reduce dependence on ASML’s tools (e.g. via alternative patterning), ASML would feel the loss. Mitigant: The competitive necessity of ASML’s technology often means customers cannot cut lithography spend without sacrificing their roadmap – which is why even in downturns, ASML often sees orders merely deferred. Still, customer concentration and cyclicality remain real concerns for long-term investors[51][47].

- Regulatory and Legal Risks: Besides export controls, ASML faces other regulatory and compliance risks. Antitrust issues are not prominent (ASML’s monopoly in EUV is because of technological superiority, and governments actually want to support its capacity, not break it up), but sanctions or trade policy changes can affect it (e.g. new rules on exporting to certain countries, or tariffs on components). There’s also intellectual property risk – ASML was subject to IP theft in the past (a 2021 incident where a Chinese firm allegedly stole some ASML software IP). While this didn’t materially hurt ASML, it underscores that ASML must safeguard its proprietary technology. On the regulatory front, ASML also must navigate tech sovereignty policies – for instance, the U.S. CHIPS Act and EU chips initiatives aim to localize some semiconductor capabilities. If governments demand local tool production or set heavy local content rules, ASML might need to adjust operations or supply chains. Additionally, environmental regulations could impose costs: ASML’s tools consume a lot of power and exotic materials (EUV uses tin droplets, etc.), so increased environmental compliance or carbon emissions rules for its operations (or those of its suppliers) could raise costs. However, ASML has robust sustainability programs and targets (net zero by 2040 for its operations)[52][53], indicating it is proactively managing this.

- Execution and Technology Transitions: A more company-specific risk is execution risk in developing next-generation technology. ASML’s future growth relies on successfully rolling out complex new machines like High-NA EUV. These systems are at the frontier of physics and engineering, with extremely tight tolerances and new architectures. There’s a risk that technical hurdles (e.g. achieving expected throughput or yield stability) could cause delays or performance shortfalls in High-NA EUV[54]. If, for instance, High-NA EUV deployment slips by a couple of years, chipmakers might delay some capacity expansion or rely more on multiple-patterning with existing tools – potentially affecting ASML’s revenue timing or allowing a competitor more time to catch up. Moreover, each new generation of tools is more costly and complex than the last; R&D and production costs are rising exponentially for ASML[55]. If ASML fails to manage this well, its margins could be pressured (e.g. spending too much on a technology that takes longer to monetize). Thus far, ASML has proven adept, but the margin for error is shrinking as tools get more complex. Customers also need to be convinced of the value – if High-NA EUV’s cost vs. benefit doesn’t meet expectations, chipmakers might be slow to adopt it (hesitating to invest ~$400 million per tool)[56][57]. This would impact ASML’s long-term sales growth. However, it’s worth noting that ASML currently has no real rival close to its capabilities[58]. This gives it some breathing room to resolve issues. Execution risk also extends to scaling manufacturing – ASML has to ramp production (possibly to ~90 EUV tools/year by mid-decade) to meet demand. Any operational misstep could create backlogs or disappointed customers. Investors should monitor ASML’s progress on new product milestones (e.g. first High-NA prototype deliveries, performance specs achieved, etc.).

- Market Saturation or Slower Industry Growth: ASML’s long-range outlook assumes continued high demand for advanced chips (logic and memory). If end-market demand were to structurally slow (for example, if the pace of smartphone or PC innovation stagnated, or AI chip demand cycles through), chipmakers might reduce capital investment plans. ASML’s own 2022 Investor Day scenarios project annual revenue could range widely by 2030 (€44 billion to €60 billion) depending on market growth[59]. This shows there’s uncertainty – if the lower-end scenario plays out (perhaps due to global recessions, overcapacity, etc.), ASML’s growth would be more modest. Additionally, geopolitical fragmentation could lead to regional fabs that are smaller or less efficient (duplicate capacity in US/EU), which might affect tool demand patterns. It’s also conceivable (though not currently likely) that a disruptive technology could emerge in the long term – for instance, if a novel method of chipmaking (like quantum lithography or some radical equipment innovation) appeared, ASML would have to adapt. At present, no such alternative is on the horizon; ASML’s own technologies are the enablers of chip roadmaps for at least the next decade.

In summary, ASML’s risk profile includes external factors (geopolitics, trade policy, economic cycles) and internal challenges (executing bleeding-edge innovation, scaling production). Geopolitical tensions and export controls stand out as a prominent risk that could cap growth or shift where revenue comes from[51][40]. Supply chain fragility and reliance on key partners like Zeiss pose operational risks[44]. The cyclical nature of chip demand means investors should expect ups and downs, even if the long-term trend is upward[47]. And while ASML has a wide moat, it must continue to innovate flawlessly to maintain its lead – the complexity of that task is itself a risk if mismanaged[57][55]. Importantly, none of these risks suggest an imminent threat to ASML’s dominance; rather, they are factors to monitor as they could influence growth rates or cause periodic volatility in an otherwise strong long-term trajectory. ASML’s management is aware of these challenges – for example, they diversify supplier sourcing where possible and engage with governments on export issues – but investors should keep them in mind. Despite the risks, ASML’s deep integration with customers and decades of know-how give it resilience[49]. Its tools are mission-critical, and that provides a degree of stability even when facing headwinds. For a long-term retail investor, the takeaway is to remain cognizant of these risk factors, but also to recognize that ASML’s fundamental position – as the enabler of next-generation semiconductors – grants it strategic importance that can help navigate such challenges[60][61].

Conclusion – Long-Term Investor Perspective

For a long-term retail investor, ASML represents a unique franchise at the heart of the semiconductor industry. Over the past five years, the company has demonstrated exceptional financial performance (strong growth, high margins) backed by relentless innovation. It dominates a critical niche (lithography equipment) with high barriers to entry and has deep partnerships across the chip ecosystem. Looking ahead, ASML’s growth will be driven by secular trends – the world’s increasing need for computing power (AI, cloud, 5G, IoT, automotive intelligence, etc.) translates to continued demand for advanced chips, which in turn requires ASML’s machines. The company’s own scenarios foresee substantial revenue expansion by 2025–2030 as it supplies the tools for these new chips[59]. Crucially, ASML’s technological roadmap (EUV, High-NA EUV, improved DUV) aligns with its customers’ needs to keep shrinking feature sizes and improving chip efficiency, anchoring its long-term relevance.

Investors should weigh the risks – particularly geopolitical factors that could influence where and how ASML does business, and the ever-present cyclicality in tech – but these must be viewed in context. ASML’s position as a de facto monopolist in bleeding-edge lithography gives it pricing power, a robust order backlog, and a degree of insulation (e.g. competitors can’t easily poach its market). It also means governments and customers alike have a stake in ASML’s stability (for instance, countries are investing in local fabs that will ultimately need ASML tools). While export controls might limit some sales, they also underscore how strategically essential ASML’s technology is – a status that few companies in the world share.

From a long-term perspective, ASML offers a compelling story of high-margin growth supported by technological indispensability. It has been balancing growth investments with shareholder returns, and its financial stewardship has remained prudent (strong free cash flow, increasing dividends, and buybacks in recent years). The next decade will see ASML enabling new innovations in computing – from 2 nm chips to potentially 1 nm and beyond – which suggests a continued runway for growth. Investors should keep an eye on how ASML navigates export regulations and ramps High-NA EUV, as these will be key to hitting its optimistic scenarios. However, given ASML’s track record and deep industry integration, many analysts view it as one of the most strategically critical companies in tech hardware[49] – effectively a cornerstone of modern digital infrastructure. For a retail investor with a long-term horizon, ASML presents a rare combination: a dominant market position in a high-growth industry, sustained by both engineering excellence and favorable demand fundamentals. As long as the world keeps demanding faster, more efficient semiconductors, ASML is poised to be a prime beneficiary – albeit one that must skillfully manage the complexities that come with its success.

Sources: Official ASML annual reports and filings[1][5][3], ASML Investor Day presentations, company press releases, and industry analyses. The financial data and growth figures are drawn from ASML’s 2019–2023 reports[7][14]. Competitive landscape information references market share and revenue figures from industry research[26][18]. Discussions on technology and strategy are based on ASML’s own disclosures and credible industry commentary[30][62]. Risk factor analysis incorporates insights from financial analysts and ASML’s statements on export controls and supply chain risks[40][44]. This comprehensive review aims to provide a balanced, up-to-date overview for investors.

[1] [14] [30] [32] [33] [34] [35] [36] [37] [38] [39] [48] [52] [53] [59] [62] 2023 Annual Report | ASML

[2] Highlights – Annual Report 2019 | ASML

[3] [7] [9] ASML reports €14.0 billion net sales and €3.6 billion net income in 2020

[4] [12] [16] 2024 Annual Report based on US GAAP

[5] [8] [10] [15] [29] Highlights – Annual Report 2021 | ASML

[6] [17] [31] Highlights – Annual Report 2022 | ASML

[11] Gross Profit Margin For ASML Holding NV ADR (ASML) – Finbox

[13] [PDF] asml annual report 2023

[18] [19] [21] [22] [24] ASML Competitors and Alternatives: Expert Market Analysis Guide

[20] Tracing the Emergence of Extreme Ultraviolet Lithography – CSET

Tracing the Emergence of Extreme Ultraviolet Lithography

[23] Applied Materials Announces Fourth Quarter and Fiscal Year 2023 …

[25] Tokyo Electron’s Place in Global Semiconductor Manufacturing

[26] [27] [28] Tokyo Electron Deep Dive – Part 1 – by Moore Morris

[40] [41] [42] [43] [47] [49] [50] [51] [54] [55] [56] [57] [58] [60] [61] What Could Go Wrong for ASML Stock? 3 Risks Long-Term Investors Should Watch | Nasdaq

[44] [45] EUV Lithography and Its Implications for Supply Chain Logistics

[46] EUV Lithography and the Fragility of Innovation | by Zander Deutch