January 18, 2026

Micron Technology: Financial Performance, New York Megafab, and Memory Market Outlook

Recent Financial Performance and Stock Trends

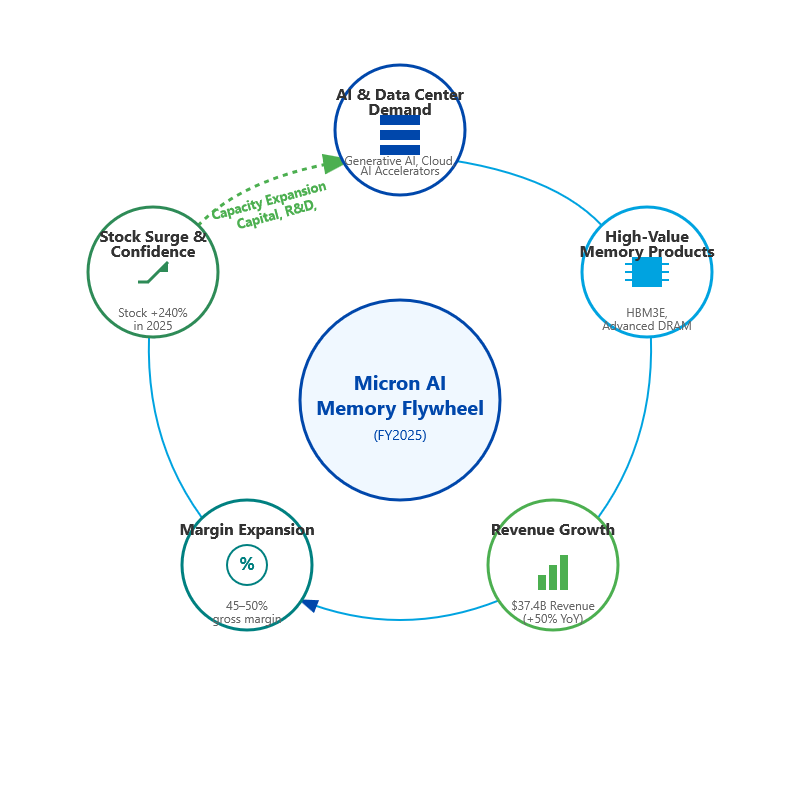

Micron Technology (NASDAQ: MU) delivered record financial results in fiscal 2025, rebounding sharply from the prior year’s downturn. Full-year 2025 revenue reached $37.38 billion, a 50% jump from $25.11 billion in 2024[1][2]. Profits surged accordingly – Micron’s GAAP net income was $8.54 billion for 2025 (versus just $0.78 billion in 2024)[3][4]. The fourth quarter alone saw revenue of $11.32 billion, up from $7.75 billion in the year-ago quarter[5]. Micron’s gross margins expanded to ~45–50% by late 2025 thanks to higher memory prices and an improved product mix[6][7]. CEO Sanjay Mehrotra touted the “record-breaking fiscal year” and noted Micron’s strong position as “the only U.S.-based memory manufacturer” positioned to capitalize on booming AI-driven demand[8].

Micron’s stock price surged dramatically in 2025 on the back of these results and optimism around AI. The stock more than tripled in value during 2025, rising over 240% as investors bet on Micron as a key supplier for AI infrastructure[9][10]. By late 2025, Micron’s share price was approaching all-time highs (near the $300–$400 range) after an unprecedented rally[11][12]. Wall Street took note – analysts upgraded the stock and raised price targets, citing Micron’s strong earnings and expectation that the memory “supercycle” could continue. For example, Bank of America analysts lifted their target to $300, predicting “much higher earnings” ahead as the AI-driven memory upcycle endures[13]. Retail investors were similarly bullish, with some comparing Micron’s trajectory to past tech high-flyers[11]. This optimism reflects Micron’s recent growth drivers, notably the explosion in demand for advanced memory chips.

Key growth drivers for Micron include the booming demand for AI and data center memory, new high-value products, and broad end-market strength. In 2025, cloud service providers and enterprise customers raced to deploy generative AI, which requires massive amounts of memory (DRAM and high-bandwidth memory) in servers and AI accelerators[14][15]. Micron’s focus on cutting-edge chips like HBM3E (high-bandwidth memory) paid off – HBM revenues reached a >$6 billion annual run-rate and are expected to hit $10 billion by end of 2025[14]. The company has locked in long-term supply agreements for its newest HBM products into 2026, underscoring insatiable AI-driven demand[16][17]. Other growth engines include increased memory content in automotive and industrial electronics and the transition to 5G and edge computing, which boost memory requirements in smartphones, IoT devices, and infrastructure[18][19]. In short, Micron’s strategic pivot toward high-value, next-gen memory – and a broadening array of use cases from data centers to cars – is fueling its top-line momentum.

New York Megafab: Status, Capabilities, and Strategic Importance

Project timeline – Micron’s New York expansion is a long-term endeavor. Initial site preparation began in 2023, and while construction was originally expected to start by 2024, the project saw some delays due to permitting and planning[26][27]. The official groundbreaking took place on January 16, 2026, marking the transition “from promise to progress” according to New York officials[26][27]. Micron’s first phase investment (approximately $20 billion) is planned by the end of this decade, with production output ramping in the latter half of the 2020s[24][28]. In other words, initial chip manufacturing in New York should come online around 2028–2030, gradually scaling up thereafter in line with industry demand. Even with an aggressive schedule, Micron acknowledges that building a modern fab is a multi-year process – from construction to tool installation, equipment tuning, and full production qualification[29][30]. Thus, the New York megafab will start contributing meaningfully to supply towards the end of the decade, helping meet future demand growth.

Funding and incentives – To finance this colossal project, Micron is leveraging a combination of its own capital spending and substantial government incentives. New York State has offered up to $5.5 billion in Green CHIPS subsidies over the life of the project[31][32], recognizing the economic importance. On the federal side, the project is expected to benefit from the 2022 CHIPS and Science Act: Micron can tap into federal grants and a 25% investment tax credit (AMIC) for semiconductor manufacturing. In fact, Micron anticipates up to $6.4 billion in direct federal funding (under the CHIPS Act) to support construction of this New York fab (as well as new fabs in Idaho and an expansion in Virginia)[31][33]. Micron’s CEO specifically credited the CHIPS Act and bipartisan political support as “critical to make this investment possible.”[34][35] Local authorities are also contributing – the Town of Clay and Onondaga County are providing infrastructure and services to support the site[36]. In short, Micron’s New York venture is a public-private partnership on an unprecedented scale, with government incentives offsetting a chunk of the cost in order to establish a secure domestic supply of memory chips.

Economic impact and strategic importance – Micron’s megafab is a game-changer for Upstate New York’s economy and for U.S. tech self-reliance. The project is expected to create nearly 50,000 jobs in New York, including about 9,000 high-paying Micron jobs directly at the fab, plus tens of thousands of additional jobs in construction, suppliers, and the broader community[37][38]. It is hailed as a “transformational” initiative that will turn the Syracuse/Central NY region into an advanced manufacturing hub[21][39]. Leaders note that beyond building a state-of-the-art chip plant with the nation’s largest clean room, Micron is “building opportunity for generations” in the region[39]. Strategically, the New York fab will strengthen America’s semiconductor supply chain and national security by ensuring cutting-edge memory can be produced on U.S. soil[40][21]. This reduces dependence on overseas fabs and adds resiliency, especially as memory is a vital component for everything from smartphones to cloud servers to defense systems. Industry CEOs (from NVIDIA, Google, Apple, Microsoft and others) applauded Micron’s U.S. expansion, emphasizing that advanced memory manufacturing is essential for the AI era and will support innovation across the tech ecosystem[41][42]. Micron’s New York megafab is not only a huge capacity boost for the company in coming years, but also a strategically important investment for U.S. technological leadership and economic growth.

Global RAM Shortages: Causes and Effects on Micron

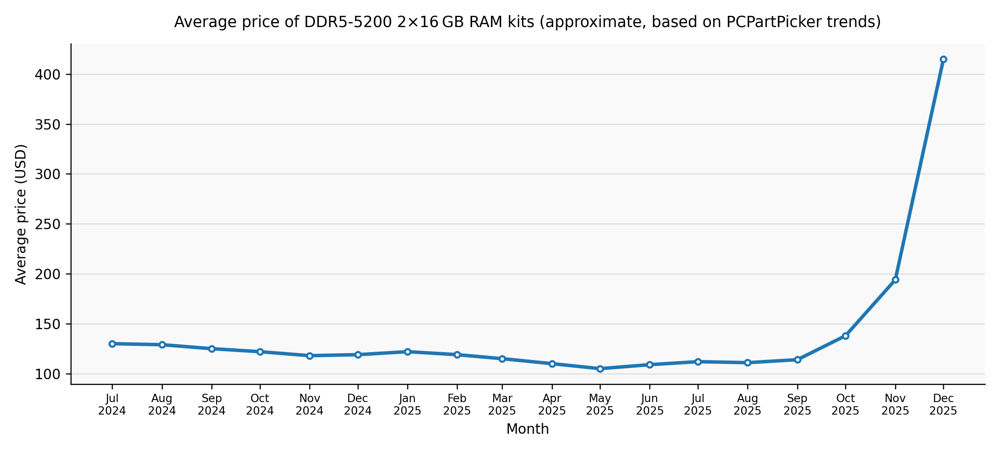

Starting in 2024, the semiconductor industry has been grappling with a global memory chip shortage – a stark reversal from the oversupply a couple of years prior. Unlike the earlier 2020–2022 chip crunch (which was driven by pandemic disruptions), this new “RAMageddon” shortage is largely structural, stemming from skyrocketing demand and shifts in production allocation[43][44]. Memory prices have accordingly shot up to multi-year highs as supply lags behind demand. By late 2025, DRAM prices were nearly triple their level a year earlier, and some DDR5 and DDR4 modules doubled in price just during the second half of 2025[45][46]. PC builders and consumers felt the pinch as a memory kit that cost $1 in early 2025 could cost $2 or more by year-end[47][48]. Major hardware OEMs like Dell and HP described the cost surge as “unprecedented,” warning that such escalating memory costs were squeezing their margins[49][50].

Key causes of the recent RAM shortages include:

- Explosion in AI-Driven Demand: The rise of generative AI and large-scale cloud computing has dramatically increased the need for memory chips. Training and running AI models (e.g. in data centers) requires enormous amounts of DRAM and specialized high-bandwidth memory (HBM) for GPUs[51][52]. Tech giants like Google, Amazon, Meta, Microsoft, and OpenAI are collectively pouring hundreds of billions into AI infrastructure, driving insatiable demand for memory[51][53]. Notably, OpenAI’s massive AI project is projected to alone consume up to 40% of the world’s DRAM supply, as it deploys roughly 900,000 wafers per month of memory – a staggering figure that underscores how AI workloads are gobbling up chips[54][55].

- Shift to High-Bandwidth Memory (HBM): Memory manufacturers (Micron, Samsung, SK Hynix) have been reallocating a huge chunk of their fab capacity to produce high-margin HBM for AI, at the expense of traditional PC and mobile RAM. HBM chips use far more silicon per bit than standard DDR4/DDR5 DRAM[56][57]. In industry terms, every wafer devoted to HBM yields fewer total gigabytes, effectively displacing supply that would have gone to commodity RAM. For example, Samsung ramped up a new HBM4 line in 2025 that diverted tens of thousands of wafers per month away from consumer DRAM production[58][59]. Micron and others likewise pivoted aggressively to meet lucrative AI memory contracts. This “die penalty” – sacrificing ~3 bits of standard DRAM for each 1 bit of HBM – created a silent squeeze in the PC/smartphone RAM market[60][61]. By late 2025, server DRAM prices had soared over 300% year-on-year as a result[60][62].

- Geopolitical and Trade Factors: U.S.–China tech tensions have also tightened supply. In 2025, major suppliers like Samsung and SK Hynix halted sales of certain chipmaking equipment to China under pressure from U.S. export controls[63][64]. This effectively capped China’s ability to expand memory production. Additionally, the U.S. considered new tariffs on semiconductors, prompting panic orders and supply chain shifts (e.g. Apple accelerating moves to source iPhone memory outside China)[64][65]. These factors introduced friction and uncertainty, contributing to the global supply constraint.

- Legacy Node Capacity and NAND Constraints: In the NAND flash market, manufacturers have prioritized newer, higher-density products (like enterprise SSDs for data centers) and retired older production lines. This meant reduced output of older-gen chips still used in many devices. In late 2025, some NAND flash contract prices spiked >60% in a single month as legacy capacity was phased out faster than expected[66][67]. Similarly for DRAM, many suppliers began phasing out DDR4 and older mobile DRAM in 2024–2025 to concentrate on DDR5 and LPDDR5 for new platforms[68][69]. The deliberate winding down of older generation memory production led to acute shortages of DDR4 (still widely needed by PCs, servers, etc.), to the point that by 2025 DDR4 prices caught up to the newer DDR5[70][71].

- Shrinking Inventories and Stockpiling: The memory industry entered 2024 with a glut of inventory (after the 2022–23 downturn). But manufacturers slashed output through 2024 and sold off excess stock. By Q4 2025, the average DRAM inventory had plunged to ~8 weeks, down from ~17 weeks a year prior and over 30 weeks at the peak of oversupply in 2023[72][73]. In other words, the huge buffer of unsold chips was largely absorbed, leaving little slack in the supply chain. As a result, device makers no longer had a cushion and some engaged in double-ordering and hoarding in 2025 – placing extra orders and building their own stockpiles to hedge against shortages[74][75]. For instance, Lenovo’s CFO said their memory inventory was 50% above normal levels to lock in supply ahead of further price hikes[76][50]. This precautionary buying only intensified the crunch, as panic orders pulled more chips out of the market.

- Average DDR5 memory kit prices skyrocketed in late 2025, reflecting the severe supply-demand imbalance. The net effect of these factors was a historic memory squeeze in 2025. DRAM contract prices leapt roughly 45–50% in just Q4 2025, and were projected to climb another ~60% in early 2026[60][61]. Retail RAM prices similarly spiked – as shown above, the average price of a 32GB DDR5 kit nearly quadrupled from mid-2025 to December 2025[47][77]. In markets like Japan, retailers even started limiting how many memory modules each customer could buy to prevent hoarding, as popular DDR5 models sold for more than double their spring 2025 prices[78][79]. Major PC OEMs responded by raising computer prices and offering lower default RAM configurations to cope with the cost increases[80][81]. All of this underscores how profoundly the AI-driven memory shortage has disrupted the tech supply chain, rippling from component suppliers to manufacturers to end consumers.

Impact on Micron’s supply chain and pricing – As one of the three dominant memory suppliers, Micron has been directly impacted by – and in many ways, benefited from – the global RAM shortage. With demand outstripping supply, Micron gained significant pricing power in 2024–2025. The company implemented multiple rounds of price hikes (20%, 30%, or more) on DRAM products as the market tightened[82][83]. In September 2025, Micron took the unusual step of suspending all new price quotes for its memory products and even canceling previously agreed contract prices[84][85]. This drastic move signaled that Micron was essentially “sold out” of inventory and would reprice its output higher. By pausing quotes for a week and withholding supply, Micron aimed to reassess its inventory and reset pricing at a more favorable equilibrium amid the shortage[86][87]. The company also became hesitant to lock into long-term contracts at old prices – a clear indication that it foresaw continued tightness and wanted flexibility to charge market rates going forward[88][87]. For buyers, these hardball tactics from Micron (and peers) meant scrambling to secure allocations and little room to negotiate; many OEMs were forced to accept higher prices or risk no supply[89].

Micron’s own supply chain operations have been running at full tilt to meet demand. After cutting production in 2023 during the glut, Micron and other manufacturers ramped utilization back up in 2024. Yet the pivot to HBM and advanced chips means capacity for standard memory remains constrained. By the end of 2025, Micron confirmed that its production of high-bandwidth memory was fully booked through 2026 – essentially every HBM chip it could produce had a buyer lined up[90][91]. This “effectively sold out” status initially sent Micron’s stock soaring further[92][93]. It also means Micron has had to allocate supply carefully among customers. The company even decided to exit its consumer-oriented Crucial memory business (which sold retail RAM and SSDs) in late 2025 in order to focus on supplying larger strategic customers[94][95]. This retreat from low-margin consumer sales was a strategic move to free up inventory for data center and OEM clients who urgently need memory for AI and are willing to pay premium prices. Additionally, some big customers like Apple had preemptively secured long-term DRAM supply agreements through early 2026[96], which helped insulate them but locked in portions of Micron’s capacity. Overall, Micron’s challenge has been managing allocation in a zero-sum environment – the company prioritized fulfilling contracts for key partners (and lucrative AI players) even as smaller buyers were left short.

In terms of inventory, Micron and the industry have largely worked down the excess stock from the prior downturn. Micron ended fiscal 2025 with healthier inventory levels and strong cash flow (it generated $3.9 billion in free cash flow in one quarter amid the boom)[97][98]. The industry-wide buffer is now minimal: as noted, average DRAM inventories fell to only a couple months’ worth of supply by late 2025[74]. Micron’s own inventory is likely lean, with most new output immediately shipped to satisfy backlog orders. In fact, Micron’s supply chain is under such pressure that the company warned the shortage may persist for years. In January 2026, Micron stated that global DRAM supply will likely remain tight “in any meaningful way before 2028”, even with new fabs on the way[99][100]. The process of adding capacity is slow, and much of the new capacity (e.g. Micron’s upcoming Idaho and New York fabs) is earmarked for advanced chips rather than relieving consumer markets[101][30]. This frank outlook underscores that Micron foresees multiple years of a sellers’ market in memory.

Micron’s strategies to mitigate the shortages involve both short-term actions and long-term investments. In the near term, Micron has been maximizing output of its most in-demand products (like ramping HBM3E and high-density DDR5) and optimizing its product mix toward higher-margin segments[102][103]. The company’s decision to pivot production lines to HBM4 in 2025, even at the cost of standard DRAM volume, was one tactical response to capture the AI opportunity (and it contributed to the broader DDR shortage)[90][91]. Micron also aggressively raised capital expenditures – planning a $20 billion CapEx in FY2026 – to fund expansions and technology transitions[104][105]. This includes speeding up projects like the new fabs in Boise, Idaho and Central New York, which, once operational, will increase supply (though not immediately). The company is counting on government incentives (CHIPS Act support) to help accelerate these capacity additions[31][32]. Furthermore, Micron is working closely with key customers to manage the supply crunch. For example, it is entering long-term supply agreements (ensuring guaranteed supply for strategic partners) and focusing support on segments like cloud, automotive, and enterprise where demand is strongest. By exiting the low-end retail market and concentrating on core enterprise and OEM clients, Micron can better allocate its limited output to those who value it most (and reduce the number of customers it has to serve during shortages). Finally, Micron continues to innovate on technology – investing in next-gen memory like HBM4, DDR6, and advanced 3D NAND – which over time will improve bit output per wafer and ease some pressure[106][107]. These R&D efforts, while not an immediate fix, are crucial to mitigate future shortages by boosting efficiency and capacity with new tech. In summary, Micron is leveraging a mix of pricing power, selective supply allocation, expansion projects, and strategic focus to navigate and capitalize on the current memory supply crisis.

Investor Outlook: Risks and Opportunities

For investors in Micron, the developments above present a landscape of significant opportunities balanced by notable risks. Micron’s fortunes have always been tied to the notoriously cyclical memory chip market, but the current cycle has unique aspects driven by AI. Here is a summary of key opportunities and risks for Micron investors:

- Opportunity – AI Supercycle and High Demand: The surge in AI and data center demand for memory is a major tailwind for Micron. The company is experiencing what some call an “AI memory supercycle,” with an order book that is essentially sold out for cutting-edge products. Micron’s revenue and margins have expanded dramatically as it dictates pricing in a seller’s market[108][109]. If AI adoption continues to grow exponentially (requiring ever more DRAM and HBM for GPUs and servers), Micron stands to benefit from sustained demand growth well beyond a typical cycle[15][110]. Its strategic focus on high-performance memory (HBM3E, HBM4, etc.) positions Micron to capture a large share of this lucrative segment – analysts estimate the HBM market could exceed $80 billion by 2027[16][111]. In short, Micron could enjoy an extended period of elevated sales and profit if the AI-driven shortage persists.

- Opportunity – Strong Financial Position and Expansion: Micron enters this upcycle from a position of financial strength. The company has a solid balance sheet (current ratio ~2.5, moderate debt)[112][113] and generated robust cash flows in 2025. It has resumed returning capital to shareholders (e.g. dividends) as profits recovered[114]. This financial health enables Micron to invest aggressively in new capacity and R&D without jeopardizing stability. Indeed, Micron is expanding its manufacturing footprint: besides the New York megafab, it is building new fabs in Idaho and upgrading its existing facilities[31][32]. These investments, supported by government incentives, should boost Micron’s output and technological capabilities in coming years – potentially allowing it to gain market share (especially as the only U.S.-based memory maker). If executed well, Micron’s expansions could pay off in the form of higher long-term growth and a stronger competitive position.

- Opportunity – Diverse End Markets and Innovation: Micron’s business is spread across several end markets (data center, PC, mobile, automotive, industrial, etc.), which provides some resilience. Newer segments like automotive memory (for ADAS, infotainment) and industrial/IoT are growing steadily and add a layer of stable demand[110]. The push for smarter vehicles and edge devices means even outside of big data centers, memory content per device is rising – a trend Micron can capitalize on. Additionally, Micron’s commitment to innovation in memory technology can yield opportunity. It is at the forefront of developing next-gen DRAM and NAND (e.g. transitioning to new process nodes, 3D packaging, computational memory), which could give it a cost or performance edge. If Micron can be first-to-market with new memory architectures that competitors struggle with, it might command premium pricing or win strategic contracts. This innovation is also defensive, ensuring Micron remains relevant as tech evolves (for example, if new memory forms like MRAM or others emerge, Micron’s R&D could pivot accordingly).

- Opportunity – Favorable Valuation (if cycle holds): Despite the stock’s huge run-up, some analysts argue Micron remains attractively valued relative to its earnings potential. With Wall Street forecasting strong earnings in FY2026 (Micron itself guided for ~$13–$15 EPS in FY26)[115][116], the stock’s forward P/E is not excessive for a tech leader. One analysis noted Micron trading around ~13× FY2026 earnings with ~57% growth predicted, suggesting it “appears undervalued” if the upcycle sustains[117]. Should memory prices remain high or climb further, Micron could deliver earnings well above previous peaks, possibly justifying even higher share prices. In essence, if investors believe “this time is different” and the AI megatrend will prolong the cycle, Micron’s stock may yet have room to run.

On the other hand, investors must heed the risks that come with Micron’s cyclicality and external uncertainties:

- Risk – Cyclical Downturn and Oversupply: The biggest risk is that the memory market eventually flips back into oversupply, causing prices to collapse. Historically, every memory boom (no matter how strong) has sown the seeds of its bust – as high prices spur overinvestment by manufacturers, leading to a glut. There are early signs of this classic pattern: Micron and rivals are sharply increasing CapEx (Micron’s planned $20 billion FY26 spend is a record)[118], and new fabs across the globe will come online in the next 1–3 years. If these capacity additions overshoot demand (for instance, if AI hardware demand slows or proves overhyped), the market could swing to excess supply by 2027 or 2028, driving memory prices down. Some analysts already warn that Micron’s aggressive spending signals the “top of the cycle”, reminiscent of prior peaks in 2018 and 2022[104][105]. A glut would hurt Micron’s revenues and margins – potentially severely, given how fast memory prices can fall. Investors thus face the risk of a volatile earnings rollercoaster if the current supercycle succumbs to the old boom-bust logic.

- Risk – Intense Competition: Micron operates in a highly competitive oligopoly with South Korea’s Samsung Electronics and SK Hynix, both of whom are determined to maintain or grow share. These giants often outspend Micron on capital and can endure downturns due to diversified businesses. Competition is especially heating up in the lucrative HBM (AI memory) segment – all three are racing to develop the highest-capacity, fastest HBM4/5 offerings. If Samsung or Hynix pull ahead technologically or capacity-wise, Micron could lose its newfound pricing power and see market share pressure[119][106]. Furthermore, any mis-execution by Micron (delays in ramping a new node, yield issues on new chips) could be quickly exploited by rivals. There’s also the looming possibility of new entrants in memory – for instance, Chinese companies (with government backing) attempting to break into advanced DRAM. While they currently lag, a successful new competitor in a few years could upset the supply balance. Overall, competition remains a persistent risk to Micron’s margins and growth, as memory is largely a commoditized market where scale and tech leadership are critical[120][121].

- Risk – Geopolitical and Regulatory: Micron is exposed to global geopolitical risk, particularly involving China. In 2023, China restricted the use of Micron’s chips in certain infrastructure systems (citing security), which hurt Micron’s sales in that market. More broadly, U.S.–China trade tensions pose a threat: Micron could be caught in tit-for-tat sanctions, supply chain disruptions, or loss of access to the Chinese customer base (which has historically been a significant portion of memory demand). Conversely, U.S. export controls on chip tech could hamper Micron’s ability to operate in China or serve Chinese clients, potentially ceding some business to non-U.S. players. Additionally, Micron must navigate government policies like the CHIPS Act requirements, trade tariffs, and export license rules. Any adverse regulatory changes – e.g. stricter export bans, higher duties on tech components – could impact Micron’s global operations and market access[122]. Geopolitical events (Taiwan Strait tensions, etc.) also carry tail risk for the semiconductor supply chain that investors can’t ignore.

- Risk – Supply Chain and Execution: Ramping multiple mega-projects (New York, Idaho, etc.) simultaneously is an execution challenge. There’s a risk of construction delays, cost overruns, or slower yield ramp-up than planned, which could tie up capital and delay the expected capacity benefits. If, for example, Micron’s New York fab comes online late or significantly over budget, it might miss the window of peak demand or struggle to achieve intended cost efficiencies. Moreover, Micron’s reliance on external equipment and materials means it could face supply chain hiccups (e.g. if ASML or other tool providers cannot deliver lithography machines on time, or shortages of substrates occur). The memory production process is complex, and any supply chain disruptions (natural disasters, shortages of chemicals, etc.) can constrain Micron’s output[123][124]. As Micron stretches to fulfill record demand, it must expertly manage its supply chain to avoid bottlenecks – a risk if any weak link appears.

- Risk – Technological Transitions: The semiconductor industry evolves rapidly, and Micron must continuously invest in R&D to keep up. There is a risk that new memory technologies (or paradigm shifts in computing) could diminish demand for conventional DRAM/NAND. For instance, advancements in memory architectures (like persistent memory, new non-volatile technologies) or shifts to chip designs that use less memory could, in the long run, alter the demand landscape. Micron needs to successfully develop next-generation nodes (e.g. move to smaller lithographies for DRAM, more layers for NAND) to stay cost-competitive. If it falls behind technologically, it would lose its edge. The company’s future also hinges on HBM4/HBM5 and beyond – delivering those on schedule is crucial as AI workloads grow. Any hiccup in Micron’s tech roadmap could allow competitors to outflank it. Thus, there’s an ongoing innovation risk inherent in this business[125][126].

Micron Technology today sits at the center of a memory chip boom, with tremendous momentum from the AI revolution and strategic expansions on the horizon. The company’s latest financial performance has been stellar, and its bold bet on a New York megafab underscores a commitment to growth and supply chain resilience. Investors have much to be optimistic about: Micron is riding a wave of demand that has dramatically boosted pricing and profits, and it enjoys strong support to expand capacity. However, one must remain cognizant of memory market cyclicality and external risks that could reverse the trend. Micron’s stock, having soared in 2025, now essentially prices in the continuation of an extraordinary cycle. Whether Micron proves to be a sustained AI-era winner or succumbs again to the traditional boom-bust pattern will be the key question moving forward. Prudent investors will weigh the company’s unique opportunities – leadership in a critical tech segment, government-backed expansion, and AI-driven demand – against the age-old risks of competition and cyclicality that have defined the memory industry. Micron’s journey in the coming years will likely be dynamic, offering both potential reward and volatility as it navigates this new chapter of growth.

Sources:

- Micron Investor Relations – FY2025 Financial Results[5][1]

- Bloomberg News – Micron’s AI-Fueled Forecast and Stock Rally[127]

- Stocktwits/Benzinga – Micron Stock Triples in 2025 on AI Demand[9][128]

- Investing.com – Micron SWOT and Financial Highlights[112][16]

- Micron Press Release – New $100B New York Megafab Announcement[22][23]

- NY Governor’s Office – Micron New York Groundbreaking Release[21][39]

- Wikipedia – 2024–2026 Global Memory Shortage (Background & Causes)[56][78]

- Reuters – AI Frenzy Driving Memory Chip Supply Crisis[53][129]

- Tom’s Hardware – RAM Pricing Crisis and HBM Capacity[130][131]

- Proactive Investors – Micron says Memory Tightness to Persist[100][132]

- Sourceability – Memory Market Tightens under AI Demand[82][88]

- CNY Central News – Micron New York Project Timeline[25]

- MarketBeat/Times-Online – Great Memory Debate of 2026[60][90]

- Bacloud Blog – Memory Market Outlook 2024–2026[74][73]

- Investing.com – Micron Future Growth Drivers & Risks[133][134]