January 19, 2026

Seagate Technology: A Key Player in the Data and AI Storage Economy

Executive Summary:

– Leading HDD Maker in a Data-Driven World: Seagate Technology (NASDAQ: STX) is one of the world’s top hard disk drive (HDD) manufacturers, supplying critical storage hardware for cloud data centers, enterprises, and consumers. Founded over 45 years ago, Seagate has shipped over 4 billion terabytes of storage and offers a full portfolio of devices, systems, and services from edge to cloud[1]. Its core business today centers on mass-capacity HDDs – high-capacity drives that handle the explosion of data generated by cloud computing and artificial intelligence (AI) applications.

– Booming Demand from AI and Cloud: The rapid adoption of AI in the cloud is fuelling an incredible surge in data storage needs[2]. Hyperscale cloud providers and enterprises are storing unprecedented volumes of data for AI model training, analytics, and services. This has led to a supply shortage and rising prices for storage products[2], creating a favorable environment for Seagate. In fact, AI-driven demand for Seagate’s highest-capacity drives is so strong that the company’s production for 2026 is nearly sold out, with long-term customer agreements providing visibility through 2027[3].

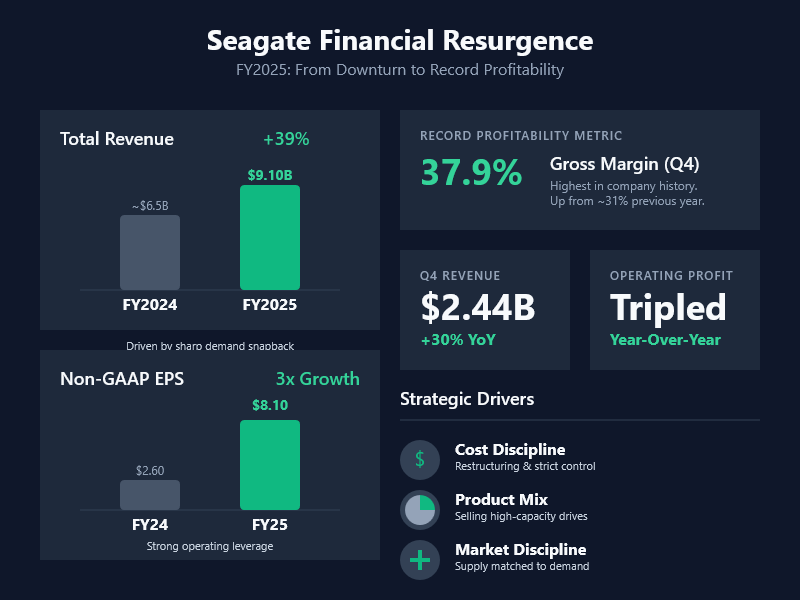

– Record Financial Performance: After a cyclical downturn in 2023, Seagate’s financials rebounded sharply in 2024–2025. In fiscal 2025, revenue jumped 39% year-over-year to $9.1 billion, with Q4 FY25 revenue up 30% YoY[4]. Gross margins hit record highs (~37–38% non-GAAP)[5], and earnings surged, driven by a healthier supply/demand balance and richer product mix. The company has strung together nine consecutive quarters of margin improvement[6]. This turnaround – powered by cloud demand for high-capacity drives – sent Seagate’s stock soaring over 200% in 2025[7], outperforming even marquee AI stocks.

– HAMR Technology & Competitive Edge: Seagate is first-to-market with HAMR (Heat-Assisted Magnetic Recording) HDD technology, which uses laser heating to vastly increase data density. HAMR drives (branded “Mozaic”) allow 30+ terabyte capacities today, on track to 40TB and beyond – leapfrogging rival Western Digital’s 24TB (28TB with SMR) drives[8][9]. By innovating on HDD areal density, Seagate aims to maintain a cost-per-terabyte advantage over flash memory and extend HDD relevance in the age of AI. Over 1 million HAMR-based drives have already shipped as of late 2025[10], and Seagate expects HAMR to make up the majority of its nearline (data center) HDD shipments by 2027[11]. This technological lead is a key differentiator against competitors.

– Bull vs. Bear View: Bullish investors see Seagate as a critical “picks and shovels” play for the AI era – a company enabling the data boom with a near-duopoly position in an essential component (HDDs). The bull case cites secular growth in data (IDC projects a 5× increase in global data generation from 2020 to 2028[12]), strong cloud demand, improving profitability, and shareholder returns (dividends and a new $5 billion buyback authorization[13][14]). Bears caution that Seagate’s recent surge may be front-loading growth: management itself guides revenue growth slowing to the low-to-mid teens CAGR after the current spike[15]. They point to potential risks like rapid SSD technological gains eroding HDD demand, the historically cyclical nature of storage spending, and an elevated valuation after the stock’s 220%+ rally[16].

Company Overview & Business Model

What Seagate Does: Seagate Technology is a leading provider of data storage hardware, best known for its hard disk drives. HDDs are electromechanical devices that store digital data on spinning magnetic platters – a workhorse technology for bulk data storage due to their low cost per terabyte. Seagate’s product portfolio ranges from small-form-factor drives for PCs and gaming, to high-capacity enterprise and cloud data center drives (up to 30+ TB each), as well as external storage solutions and storage systems. It also offers some solid-state drives (SSDs) and services (like the Lyve Cloud storage service), but HDDs account for the vast majority of its revenue. In fact, Seagate’s “Mass Capacity” storage business – largely nearline HDDs for data centers – now generates ~80% of its revenues[17][18]. The remaining ~20% comes from legacy markets (PC, consumer electronics, and mission-critical drives), which have been declining as flash-based SSDs replace HDDs in many client applications. Seagate’s strategic focus in recent years has squarely been on high-capacity drives for cloud and enterprise customers, where HDDs still hold a cost advantage and demand is growing.

How Seagate Makes Money: Seagate’s business model is centered on designing, manufacturing, and selling storage devices at scale. Revenue is earned by selling drives in large volumes to OEMs, cloud service providers, distributors, and retail channels. Key customer segments include: hyperscale cloud providers (like Amazon AWS, Google, Microsoft Azure, etc.), who buy nearline HDDs in bulk for their data centers; enterprise server and storage OEMs (such as Dell, HPE, NetApp) that integrate Seagate drives into storage arrays and servers; small businesses and consumers (buying external drives, NAS drives, and PC drives); and edge device manufacturers (for DVRs, security systems, etc.). Seagate competes primarily on cost-per-capacity, reliability, and innovation – continuously driving down the dollars per terabyte to entice customers who need to store ever-expanding data affordably. It operates in what is effectively a duopoly with Western Digital (and to a smaller extent Toshiba) in the HDD market, which means each player generally has significant scale and bargaining power. This industry structure, while competitive, has rationalized after decades of consolidation, allowing Seagate to maintain decent margins and align supply with demand.

In the global data storage ecosystem, Seagate occupies a crucial upstream role: it supplies the fundamental storage media that underpins cloud and enterprise infrastructure. Its HDDs fill the massive data centers that power cloud computing, streaming services, social networks, AI model training datasets, and more. For example, when a cloud provider builds out a new data lake or an archival storage cluster, it will often deploy tens of thousands of Seagate or WD drives in racks. Seagate’s drives serve as the backbone of “cold” and “warm” storage tiers – where large volumes of data are stored more economically (albeit with slower access than flash). In total, Seagate has shipped over 4 zettabytes (4 billion terabytes) of storage capacity in its history, reflecting its foundational role in storing the world’s data[1]. As data generation accelerates in the modern economy, Seagate’s mission is to provide the scalable, low-cost storage needed to hold that data, whether it’s in cloud data centers, at the network edge, or in consumers’ hands.

Business Model Characteristics: The HDD business tends to be capital-intensive (fabs and factories for heads, media, and drive assembly) but benefits from economies of scale – unit costs drop as volumes rise. Seagate’s profitability depends on managing its supply chain and utilization efficiently, aligning output with demand (to avoid gluts that depress pricing). In recent years, Seagate has implemented structural changes to its model such as build-to-order agreements with major customers to extend demand visibility and avoid inventory build-ups[19]. This has helped stabilize pricing and margins in what used to be a more boom-bust industry. The company also returns a significant portion of cash to shareholders (historically via dividends, and now via buybacks as well), reflecting strong cash flows in upcycles. Overall, Seagate’s business today is about being the leading provider of mass-capacity storage to a data-hungry world – essentially selling the “shovels” in the gold rush of the digital era.

Industry & Market Trends

Explosive Data Growth: The overarching trend driving Seagate’s market is the exponential growth of digital data. We are in an era where cloud computing, IoT sensors, high-resolution video, and especially AI applications are creating data at unprecedented rates. Market researchers estimate that global data generation could increase more than 5× from 2020 to 2028, reaching hundreds of zettabytes per year[12]. Every time an AI model is trained on massive datasets, or a billion users upload content to the cloud, or autonomous systems record sensor data, it feeds this data explosion. AI and machine learning are particularly data-intensive, requiring massive datasets for training and then generating new data inferences[20][21]. This tsunami of data directly benefits storage providers: IDC projects that the need for data center storage will more than double from 2024 to 2028, expanding Seagate’s addressable market from ~$13 billion to ~$23 billion[12]. In short, data is the new oil, and it has to be stored somewhere – which has created a secular tailwind for companies like Seagate that supply cost-effective storage capacity.

Cloud & Hyperscaler Demand: A significant portion of data growth is concentrated in hyperscale cloud data centers (run by the likes of Amazon, Google, Microsoft, Meta, etc.). These companies are both major customers and bellwethers for storage demand. Recent trends indicate hyperscalers have been rapidly expanding their storage capacity to support AI services and cloud applications. Seagate noted that global cloud demand for nearline HDDs is exceptionally strong, with orders essentially filling its production capacity[3]. Management has shifted to a build-to-order model where capacity is largely pre-booked through mid-2026, giving confidence that demand will remain robust[22][23]. The CEO Dave Mosley highlighted that contracts with cloud customers extend into 2027, reinforcing the view of sustained favorable demand[3]. Another angle is geographic: Western Digital cited a surge in China’s cloud demand as well, with nearline revenue in China doubling sequentially in late 2023[24][25] – suggesting a global phenomenon of cloud buildout.

Importantly, AI workloads at hyperscalers are a key driver in the current cycle. Training large AI models (like GPT-style models) requires storing petabytes of training data (often on relatively slower but huge-capacity drives), and then feeding subsets of data quickly to GPUs (often from faster SSDs). This dynamic creates complementary roles for HDDs and SSDs in the data center. Seagate’s high-capacity HDDs are ideal for the “data lakes” – the vast repositories of raw data that AI models ingest. As Western Digital’s CEO put it, “clearly, HDD plays a big role in the AI storage life cycle… all of the big data lakes and raw datasets are going to be stored on HDD. It’s just the economics of where you store that data.”[26]. After initial processing, critical subsets might be moved to SSD, but the bulk storage and archival remains an HDD domain for cost reasons. This symbiosis means that as hyperscalers invest in AI, they’re investing in both flash and disk – leading to what WD calls a “rising tide lifting all boats” scenario where it’s “about growth and not substitution” between HDDs and SSDs[27]. Indeed, data centers will continue to use HDDs where they can, and SSDs where they must (for speed)[28].

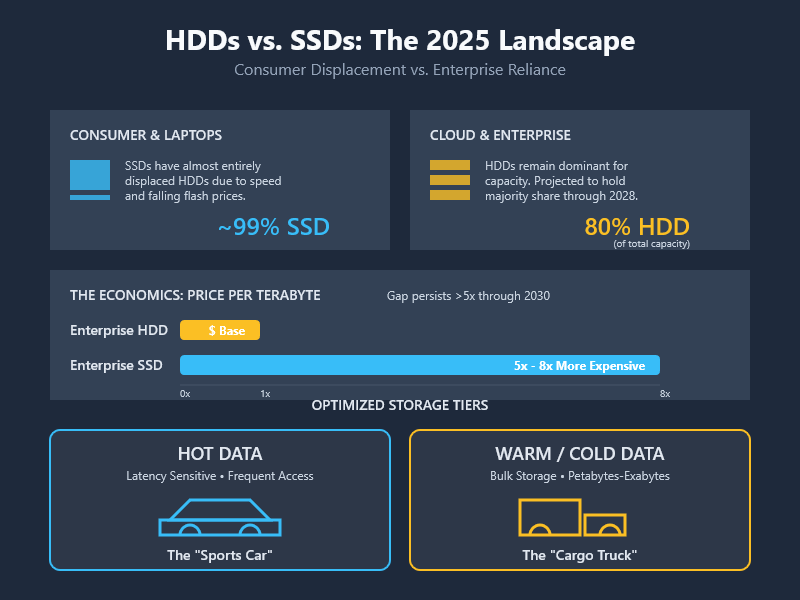

HDDs vs. SSDs (2025–2026): The balance between HDDs and SSDs is a pivotal industry topic. In consumer devices and laptops, SSDs have almost entirely displaced HDDs by 2025 due to speed and falling flash prices[29]. But in enterprise and cloud storage, the picture is more nuanced. Hard disks remain the dominant medium for “cold” data storage – estimates say HDDs will still make up nearly 80% of storage capacity in cloud data centers through 2028[30]. The reason is simple: cost at scale. While SSD prices have dropped, enterprise SSDs still cost 5–8× more per terabyte than enterprise HDDs[31], and that cost gap is projected to persist (remaining >5× through the next five years). For storing petabytes-exabytes of data that isn’t frequently accessed, HDDs offer dramatically lower Total Cost of Ownership (TCO). Large cloud customers actually optimize their storage tiers by use case – using expensive flash only for hot, latency-sensitive data, and HDDs for the vast warm and cold data that doesn’t need instant access[32][33]. This tiered approach is akin to using a fleet of trucks (HDDs) to haul bulk cargo, versus sports cars (SSDs) for quick deliveries – each has a place based on economics and performance[34][33].

That said, industry trends also show HDD technology evolving to stay relevant, and SSD technology racing to encroach on high-capacity use cases. On one hand, HDD makers are pushing techniques like shingled recording (SMR) and now HAMR to keep increasing capacities (Seagate and WD both have roadmaps into the 30–40 TB range in the next couple of years)[35][9]. On the other hand, flash memory vendors are introducing ultra-high capacity SSDs aimed at data center storage – for example, 128 TB QLC SSDs have emerged, with 256 TB and 512 TB drives on the horizon in the next 3–5 years[36]. If those materialize affordably, they could store far more data per drive than HDDs (the article notes by the time HDDs hit 100 TB, SSDs may reach 1 petabyte)[36]. Moreover, SSDs inherently provide higher throughput and lower latency, which is attractive for AI and big data workflows. Some hyperscalers are reportedly exploring all-flash or flash-heavy architectures for AI despite cost, prioritizing performance, power efficiency, and density[37][38]. For now, the economics still favor HDDs for bulk storage – when considering $/TB, power per TB, and reliability, flash hasn’t fully closed the gap in cost-effectiveness[31][39]. For example, a 24 TB HDD might use more power and space than a 128 TB SSD, but that SSD currently costs many times more; large data centers calculate TCO carefully and often conclude a mix of media is optimal[31][40].

In 2025–2026, HDDs and SSDs are best seen as complementary in modern IT infrastructure. Both are essential: HDDs provide the capacity backbone for backups, archives, and big data lakes, while SSDs provide the speed layer for active datasets and AI training caches[41][21]. The rise of AI has actually highlighted this complementary need – AI systems need lots of data (favoring cheap storage) and fast access to slices of it (favoring flash). The net effect has been an uplift in demand for both types of storage. As Western Digital said about AI impact, “it’s literally like a rising tide lifting all boats… the more data generated, the more data will need to be stored.”[27]. For Seagate, the key trend is that mass-capacity storage demand is in a structural growth phase, not just a temporary spike. Industry forecasts call for mid-20% annual exabyte growth in nearline HDD demand over the medium term[42]. Hyperscalers, cloud service providers, and even AI startups are investing in expanding storage. The fact that Seagate’s nearline drive shipments were up 52% year-on-year in the latest quarter[43] underscores this trend.

AI, Hyperscalers & Seagate’s Outlook: The AI boom of 2023–2025 has been a game-changer for storage. Seagate’s executives noted that traditional compute workloads and “increasingly AI-supported applications” are driving data growth that aligns with their new high-capacity drives[44]. On an earnings call, Seagate’s CFO observed “demand is strong, it’s above supply,” with any constraints being more about production ramp timing than lack of orders[45]. This has allowed the company to be more selective and even raise prices modestly on new contracts (negotiating slight price increases on like-for-like deals)[46]. Indeed, industry reports show storage pricing has firmed up – contract prices of HDDs rose ~4% in Q4 2025 amid the tight supply[47]. Such a pricing environment is a notable departure from the past (when storage prices mostly declined year after year) and speaks to how exceptional the current demand cycle is.

Looking ahead, market trends to watch include: the pace of hyperscaler capacity expansions (will they continue unabated or digest after an AI-driven surge?), the trajectory of NAND flash pricing and high-capacity SSD introductions, and any technological breakthroughs (e.g., new storage mediums or improvements in tape or optical archives, which could carve out niches). But for the next few years, consensus is that data is growing so fast that all storage mediums will be pressed to keep up. Seagate’s market – large-scale data storage – is expected to enjoy strong tailwinds from cloud services, AI, video, and edge data growth. Even if individual end markets (PCs, etc.) are mature or declining, the mass-capacity segment appears to have transitioned to a structural growth story rather than a purely cyclical one[42].

Technology & Competitive Advantage

HAMR Technology – A Game Changer: Seagate’s flagship technology initiative is HAMR (Heat-Assisted Magnetic Recording), which represents the next big leap in HDD capacity. In simple terms, HAMR uses a tiny laser diode on the drive head to momentarily heat the disk surface at the write point, allowing the use of a media coating that can store data bits much more densely (because the heat overcomes the medium’s coercivity for writing). This enables a dramatic increase in areal density (bits per square inch on the platter) beyond the limits of current perpendicular magnetic recording (PMR). Why does this matter? It’s the most cost-efficient way to scale drive capacities going forward[48]. With HAMR, Seagate has demonstrated drives with 3+ terabytes per platter, and is targeting 5–10 TB per platter over the next few generations[49][13]. Most of Seagate’s HDDs have up to 10 platters, so this implies eventual drive capacities of 30 TB, 50 TB, even 100 TB down the road. In fact, Seagate launched the industry’s first HAMR-based nearline drives in 2023–2024 (around 30 TB capacity) and is on track to ramp 30+ TB drives (e.g. 32 TB) in high volume, with 40 TB-class drives (4 TB/platter) targeted in 1H 2026[22]. By comparison, traditional PMR technology (even with energy-assist) tops out in the mid-20TB range per drive today. Thus, HAMR gives Seagate a capacity leadership edge. At an Analyst Day presentation, management showed that Mozaic HAMR drives can hit 40 TB vs ~24 TB for PMR drives, using far fewer drives to achieve 1 exabyte deployment, which saves space and power[50][51] – a 40% improvement in TCO by one estimate for large-scale deployments using next-gen HAMR drives.

Seagate has spent over a decade developing HAMR, and being first-to-market and first-to-scale with this technology is a central competitive advantage[52][53]. The company has proprietary IP around the drive head’s laser system, media, and drive architecture that rivals are only now trying to match[54]. As of mid-2025, Seagate had shipped roughly 1 million HAMR drives (cumulatively since Q1 FY2024) to customers for qualification and initial deployment[10]. They report that three major cloud service providers have qualified HAMR-based drives and broader qualifications are ongoing[22]. This early mover status means Seagate and its customers are gaining real-world experience with HAMR. Management expects HAMR drives to become the majority of nearline HDD volume by the first half of FY2027[11]. Crucially, as HAMR scales, it should also be a tailwind for profitability – higher-capacity drives carry higher ASPs and often better margins (and fewer drives need to be shipped for a given number of exabytes, lowering unit production costs). Seagate’s plan is that by FY2028, with HAMR fully adopted, it can hit a non-GAAP gross margin of ~40% (up from ~30% in recent years)[55][56]. In short, HAMR is Seagate’s bet to extend HDD technology’s relevance well into the late 2020s and to differentiate itself as the supplier of the highest-capacity drives on the market.

R&D and Product Roadmap: Beyond HAMR, Seagate’s R&D focuses on a few key areas: increasing areal density (which HAMR addresses), improving drive energy efficiency and reliability, and lowering the cost per TB through design innovation. The product roadmap unveiled in 2025 shows a “clear path from Mozaic 3+ TB/disk to 10 TB/disk” in the coming years[57][58]. This likely involves successive generations of HAMR (sometimes referred to as HAMR 2.0, etc.), possibly new media compounds or layering techniques, and maybe multi-actuator drives to boost performance. Seagate has already experimented with dual-actuator drives (brand name “Mach.2”) which effectively double IOPS by using two independent read/write heads inside one drive – this can be a way to improve performance for large drives so they can be accessed faster. Additionally, Seagate integrates technologies like SMR (shingled magnetic recording) in some models to squeeze more data (SMR overlaps write tracks for higher density, used in archival scenarios). However, Seagate’s strategy appears to prioritize getting HAMR out broadly rather than relying heavily on SMR – in contrast, Western Digital leaned on UltraSMR (a form of SMR plus flash caching) to bump capacities to 28 TB while delaying HAMR.

One notable strength is Seagate’s vertical integration and manufacturing expertise in HDDs. The company designs and makes critical components in-house (heads, media, the new laser units for HAMR, etc.), which has enabled it to solve complex engineering challenges like bonding lasers onto millions of recording heads. This vertical integration helps in scaling HAMR production cost-effectively[54][52]. Seagate executives have expressed confidence that their proprietary laser on slider manufacturing is ready for high-volume and that yields and reliability are meeting expectations[52]. If true, this is a significant barrier for competitors to overcome, as HAMR requires mastering a new set of technologies beyond conventional HDD manufacturing.

Competitive Landscape: Seagate’s primary direct competitor in HDDs is Western Digital (WDC), which holds roughly similar market share. Western Digital differentiates itself by being a broader storage company – it has both a HDD division and a NAND flash memory division (stemming from its SanDisk acquisition). This means WD competes in HDDs and sells SSDs (client and enterprise). In contrast, Seagate is almost purely focused on HDDs, especially high-capacity enterprise drives[59]. Each approach has pros and cons: WD’s portfolio diversification means it can offer customers a one-stop-shop (e.g. selling hybrid storage solutions, or hedging bets if one technology falls out of favor). However, running two very different businesses (HDD and flash) also adds complexity, and WD has even considered separating the divisions. In fact, WD announced plans to split its HDD and flash businesses into separate units[60], highlighting the different dynamics in each. From a technology standpoint, Western Digital has not yet shipped HAMR drives in 2025. WD invested in MAMR (Microwave-Assisted Magnetic Recording) research as an alternative, and in the interim has been using energy-assisted PMR plus their OptiNAND tech (adding a flash cache and metadata on each drive) and SMR to keep increasing capacity. Their largest announced drives by late 2023 were 24 TB CMR (conventional magnetic recording) and 28 TB SMR[8]. WD’s CEO claimed their “leading ePMR + UltraSMR platform” offers the best TCO for customers until their own HAMR is ready[61][9]. WD expects to introduce HAMR in the next couple of years, but in a staged approach. In a recent call, WD outlined that over the “next several years” they plan multiple generations of nearline drives combining ePMR, OptiNAND, and SMR “in the 30 to upper-30 TB range” for high volume, “followed by… transition from ePMR to HAMR” when it’s cost-effective[9]. In other words, WD is initially achieving ~30+ TB with refined traditional tech, then will move to HAMR a bit later, presumably to ensure the technology is mature and profitable.

For now, Seagate holds the capacity crown – it has announced and started shipping 30 TB and 32 TB HAMR drives, beating WD’s max capacities[8]. This could give Seagate an edge among customers who truly need the densest drives (e.g. to minimize space/power). However, WD’s strategy might yield slightly lower near-term tech risk and potentially better initial margins (since HAMR drives likely cost more to produce initially). Another competitor, Toshiba, is a smaller third player in HDDs (market share in the teens) and also pursuing energy-assisted PMR and some HAMR R&D, but with far less scale.

Indirectly, Seagate also competes with flash memory providers (Samsung, SK Hynix, Micron, etc.) insofar as enterprise SSDs can replace some HDD slots. The battle is really about which storage medium captures the growth in data storage. Seagate’s competitive advantage here is cost leadership in $/GB for large-scale storage. As long as HDDs are significantly cheaper per terabyte, they will retain a sizable niche. Seagate’s HAMR innovation extends that cost advantage runway, because it can keep bumping up HDD capacity (thus lowering $/TB) faster than the cost of flash is declining, at least for the next few cycles. Moreover, HDD production is effectively a duopoly, whereas flash memory is a more fragmented industry with more aggressive pricing cycles – this arguably makes the HDD space more disciplined.

Key Competitive Factors: – Technology Leadership: Seagate’s head start in HAMR vs. WD’s cautious approach is a central differentiator. If Seagate’s HAMR drives prove reliable and cost-effective, it can capture outsized share of high-capacity drive sales and possibly charge a premium or enjoy better economies of scale. However, if HAMR faces issues (e.g. durability problems or delays), WD could catch up or customers might hold off. So far, Seagate reports smooth progress and even record nearline sales thanks to its 20TB+ HAMR and PMR drives[62]. – Customer Relationships: Both Seagate and WD sell to the same pool of hyperscalers and OEMs. It’s known that these large buyers multi-source and also negotiate hard on pricing. Any account wins or losses can swing share. For example, WD indicated it gained traction with UltraSMR drives and was broadening adoption to a “third cloud titan” in the U.S. in 2024[63]. Seagate’s BTO contracts suggest they have secured long-term deals with key customers. Maintaining preferred-supplier status through each technology transition is critical. – Product Breadth: Seagate’s portfolio is a bit less diversified (mostly HDD). Western Digital can bundle SSDs and HDDs, which might appeal to some customers or for certain solutions (e.g. hybrid storage arrays). However, Seagate’s singular focus might also allow it to be more agile and specialized in the HDD domain. Interestingly, Seagate has dabbled in enterprise SSDs (often rebranding others’ NAND) but it’s not a major part of revenue. – Financial Strength and Scale: Both companies are similar in annual revenue (WD is larger when including flash, but in HDD-specific revenue they’re close). WD’s dual business means its financial performance also hinges on NAND market conditions (which can be very volatile – e.g. NAND had a glut and price crash in 2022–2023, hurting WD’s results). Seagate, being pure-play, is fully leveraged to HDD market conditions – this hurt it during the downturn but has supercharged it during the upturn. In 2025, Seagate’s operating margins and cash flow have rebounded strongly, arguably surpassing WD’s on the HDD side[64][24]. – Innovation Pipeline: Beyond HAMR, both companies will explore further tech. Seagate has mentioned “granular media on glass substrates” and even “future photonics” as longer-term innovations[65]. Western Digital talks about PLC (5-bit) flash and advanced SSD architectures on the flash side, and eventually its own HAMR. In essence, competition is a continual race of innovation balanced with cost. For now, Seagate’s years of R&D are paying off in a tangible lead in shipping next-gen drives, which the company believes will yield a “profitability tailwind” in the coming years[11][66].

Financial Performance

Recent Financial Results: Seagate’s financial performance has swung dramatically in the past two years. The company went through a downturn in FY2023 (amid a broader tech hardware slump and inventory correction), but FY2025 marked a roaring comeback. In the fiscal year ended June 2025, Seagate reported revenue of $9.10 billion, up 39% from FY2024[67][68]. This is a huge jump for a relatively mature company, indicating how sharp the demand snapback was. The June quarter (FQ4 2025) alone saw revenue of $2.44 B (+30% YoY) and record profitability metrics[4]. Gross margins expanded to 37.9% (non-GAAP) in that quarter – the highest in Seagate’s history – compared to ~31% a year prior[5]. Non-GAAP EPS for FY25 was $8.10, versus ~$2.60 in FY24[69][4], reflecting strong operating leverage as sales rebounded. CEO Dave Mosley highlighted that FY25 was “one of the most profitable years in the company’s history”, with gross profit dollars nearly doubling and operating profit more than tripling year-over-year[6]. This was achieved through a combination of strict cost discipline (including prior restructuring), supply-demand alignment, and richer product mix (selling more high-capacity drives at better pricing)[6][4]. It’s worth noting that Seagate also benefited from industry consolidation – with only two major suppliers, the market adjusted output to avoid the kind of oversupply that wrecks margins.

The momentum continued into early FY2026. In FQ1 2026 (quarter ending October 2025), Seagate delivered $2.63 B revenue (+21% YoY) and a non-GAAP operating margin of ~29% (up ~9 percentage points year-on-year)[70]. Earnings per share jumped 65% YoY to $2.61 for that quarter[71]. Free cash flow generation also improved significantly with the upturn; in FY25 Seagate generated $818 M FCF[67] and this is expected to grow in FY26 given higher profitability and relatively stable capex (~5% of revenue target). The company maintained its quarterly dividend of $0.70–0.72/share, returning ~$600 M to shareholders via dividends in FY25[67]. Now with profits rising, Seagate has even resumed share repurchases (which had been paused during the downturn) – management announced buybacks would restart in late 2025 and the board authorized a fresh $5 billion repurchase program[72][14]. This signals confidence in future cash flows.

Drivers of Recent Outperformance: The dramatic improvement in Seagate’s financials can be attributed to the favorable cycle in the mass-capacity storage market, largely driven by cloud and AI demand. Essentially, a supply glut and demand pause in 2022 led the industry to cut production and costs; by 2024, demand came roaring back just as supply was tight – a perfect recipe for rising sales and margins. Key drivers include: (1) Surging volume shipments – Seagate’s total HDD exabyte shipments hit record levels. In Q4 FY25, Seagate shipped 163 exabytes of disk capacity, up from 144 EB in the prior quarter[43][73]. Nearline (enterprise) drives were 91% of those shipments (137 EB, +52% YoY)[43][62], showing how the mix has shifted to high-capacity units. (2) Improved pricing environment – unlike the historical trend of per-GB prices dropping, the sheer demand and controlled supply allowed Seagate to hold or even raise pricing slightly. CFO Gianluca Romano noted that “like-for-like pricing will continue to slightly increase every time we negotiate a new lead-to-order”[46]. Industry reports of a ~4% HDD price uptick in late 2025 confirm a positive pricing trend[47]. (3) Cost/mix improvements – as the product mix skewed to large drives (16TB, 20TB, 20+TB HAMR etc.), average selling prices per drive climbed. Meanwhile, prior restructuring (including some workforce reduction and a facility divestiture in 2023) took costs out, and manufacturing efficiencies improved with higher utilization. The net effect was a jump in gross margin from ~30% to upper-30s%, and operating margin from mid-teens to mid-20s (non-GAAP) in one year[5][74]. Seagate management described this as the result of “structural enhancements to our business model and ongoing demand strength from cloud customers”[4].

Stock Performance: These strong results and the excitement around AI-driven demand have been reflected in Seagate’s stock price. Over the one-year period through 2025, STX shares rocketed roughly 225%[7]. For perspective, Seagate’s stock went from a 52-week low around ~$63 to all-time highs above $300 by late 2025[75]. This far outpaced the broader market and even many high-flying AI names (Nvidia, for instance, was up ~39% in 2025, whereas Seagate quietly gained ~225% over the same period)[7]. By January 2026, Seagate’s market capitalization was around $70 billion[76][77], making it a newly minted large-cap tech stock (and reportedly gaining inclusion in the Nasdaq-100 index). The market has essentially re-rated Seagate from a value/cyclical stock to something of a growth story given the new secular demand narrative. Even after this rally, some analysts note the stock isn’t obviously overpriced relative to growth – at ~$320/share it was trading around 25× forward earnings, roughly in line with the Nasdaq-100 average multiple[78]. And with earnings expected to continue rising (consensus foresaw 40%+ EPS growth in FY2026)[79], the forward PEG ratio could be reasonable. Of course, this assumes Seagate hits those growth estimates.

Cyclicality vs. Structural Growth: A key question for financial performance is whether Seagate’s recent growth is sustainable or largely cyclical. Historically, the storage industry has been highly cyclical – periods of heavy enterprise spending or new product upgrade cycles followed by lulls and price wars. We saw a cycle bottom in late 2022/early 2023, and a sharp up-cycle through 2024–25. There is evidence that some of this growth is structural: the mass-capacity segment (drives for cloud/data center) now constitutes the bulk of Seagate’s business and is underpinned by secular data growth trends. Management asserts that this shift reduces seasonality and cyclicality, as demand is more consistently driven by data growth rather than PC refresh cycles[42][80]. They project a “mid-20s exabyte CAGR” and low-teens revenue CAGR through FY2028[42], which suggests more steady growth rather than boom-bust. Additionally, the build-to-order model and long-term agreements provide better visibility and smoother production planning than the old days of building on spec.

However, it would be premature to say cycles are gone entirely. Even cloud spending can have digestion periods – for instance, after a massive build-out in one year, hyperscalers might moderate orders the next. Seagate’s own guidance acknowledges “near-term lumpiness” in exabyte shipment growth[81]. The company expects growth to temper to more “normalized” levels after the current surge[15]. So we might view FY2025’s 39% revenue jump as partly a catch-up from the prior downturn and an exceptional AI-related surge. Going forward, analysts expect more moderate (but still healthy) growth and are watching for signs of any over-ordering or inventory build at customers. Another cyclical factor is the memory/storage pricing cycle: right now it’s favorable (short supply), but if supply catches up or demand pauses, pricing power could evaporate, pressuring margins again. This dynamic often plays out over 2–3 year intervals in the memory industry, and HDDs could follow a similar pattern albeit with fewer players.

Bottom Line: Seagate’s current financial position is strong – revenues growing, margins at record highs, and robust free cash flow generation. The balance sheet is solid; the company has been reducing debt (it paid down ~$500 M in early 2025)[82] and carries a manageable net debt load relative to EBITDA. With the resumption of buybacks, Seagate is returning most of its free cash (they target >75% of FCF returned)[83][84], which shareholders appreciate. The key for sustaining performance will be executing on the HAMR ramp (to justify those margin targets) and navigating whatever twists the demand cycle might take. For now, investors have been rewarded by one of the best 12-month periods in Seagate’s history, enabled by the confluence of AI, cloud, and successful strategy shifts by management.

Investment Narrative

From an investment perspective, Seagate has transformed into a hot stock in the tech hardware space, thanks to the AI and data boom. Below we break down the Bull Case vs. Bear Case narratives surrounding the company:

Bull Case: Why Investors are Excited

- Picks-and-Shovels AI Play: Seagate is viewed as a “silent winner” of the AI revolution – not making AI chips or software, but selling the critical infrastructure (storage) that every AI and cloud company needs. As AI adoption soars, data storage demand explodes, and Seagate, with ~50% share in HDDs, is in a prime position to capitalize. The stock’s 220%+ surge in 2025 reflects belated recognition that Seagate is an enabler of AI’s data needs[16]. Investors see a secular growth angle: more AI, more cloud, more data = more drives sold. Unlike some AI plays, Seagate has tangible earnings and cash flow to back it up, making it an attractive way to play the data economy theme.

- Mass-Capacity Dominance & High Entry Barriers: In the realm of mass storage, there are effectively only two major suppliers (Seagate and Western Digital), and Seagate is laser-focused on this area. Such an oligopoly structure tends to be financially rewarding if managed properly – it curbs price wars and allows rational capacity investment. Seagate’s move to secure long-term deals (BTO contracts) with hyperscalers suggests a stable base of business locked in[22][23]. Furthermore, technical barriers to entry are enormous – HDD manufacturing is complex and IP-heavy, which is why no new competitor has successfully entered in decades. This gives Seagate a wide moat in its niche. Even as flash tries to encroach, the HDD duopoly is likely to capture the bulk of zettabyte-scale storage needs at least through this decade[30].

- Technology Leadership with HAMR: The bull case applauds Seagate’s innovation edge. Being first with HAMR drives means Seagate can offer the highest-capacity drives on the market, which many cloud customers want for efficiency. This should allow Seagate to gain market share at the high end and potentially even command better pricing for bleeding-edge products (at least until competitors catch up). HAMR also positions Seagate for longer-term relevance: it extends the life of HDD technology by leaps, suggesting that even by 2030, HDDs could still scale in capacity significantly. In short, Seagate is not resting on legacy tech – it’s pushing the frontier, which bodes well for staying indispensable to customers. The company’s claim that Mozaic HAMR drives deliver 40% TCO improvement for big deployments[50][51] is a selling point – if customers get more density and lower cost per GB, they’ll buy more. This tech leadership also creates an interesting profit story: as HAMR adoption increases, Seagate expects a tailwind to margins and revenue growth, driving a low-to-mid teens revenue CAGR through FY2028[11][55] (robust for a “legacy” hardware firm).

- Strong Financials and Shareholder Returns: Bulls point out that Seagate is now a cash machine. With ~37–40% gross margins and ~25–30% operating margins, the company is generating substantial earnings (analysts estimate ~$11–12 EPS in FY26, up ~42%[85]). Free cash flow is likewise improving. Management has a shareholder-friendly capital allocation: a decent dividend (currently yielding ~1% after the stock’s rise, but still ~$2.88/year payout) and an aggressive buyback plan ($5B authorized, which is ~7% of the market cap at recent prices). In FY2025, over 75% of free cash flow was returned to shareholders[83][84]. Such returns will continue if business stays strong, effectively letting investors directly benefit from the company’s success. Additionally, Seagate’s inclusion in major indices (like Nasdaq-100) and improved growth profile could attract more institutional investors.

- Secular Tailwinds, Not Just Cycles: The bull narrative emphasizes that we’re in a new era of data growth where storage isn’t a zero-sum or replacement game but a rising tide. As noted, even if SSDs grow, total data stored is growing so fast that HDDs can also grow in absolute terms[27]. For instance, an autonomous car or an AI IoT network might generate exabytes of data that need long-term storage (cold archives) – HDDs will serve that need. Cloud companies are building multi-tiered storage with both SSD and HDD, meaning HDD shipments can keep expanding. This dynamic is seen as structural (driven by AI, IoT, cloud) rather than a one-time bump. The bull case often cites IDC or company projections that global storage demand will keep rising ~20%+ annually[42], implying a solid growth runway for Seagate’s core business.

- Improved Discipline and Business Model: Seagate’s management gets credit for restructuring and adopting a more disciplined operating model. They’ve cut costs, optimized inventory, and use long-term contracts to smooth out volatility[86]. This has resulted in expanding margins and more resilience. Unlike in past cycles, Seagate didn’t chase unprofitable market share during the downturn – they focused on higher-margin products and aligning production to true demand. The outcome is one of the best earnings trajectories the company has seen. Bulls believe this is the “new Seagate” – a leaner, more focused entity capable of delivering consistent profits even in a challenging macro environment. If they can sustain ~40% gross margins and ~10% of revenue in capex, the free cash yield could be very attractive.

- Valuation Upside: Despite the big rally, some bulls argue the stock still has upside given earnings growth. At ~25× forward earnings (in line with the Nasdaq average)[78], Seagate doesn’t look expensive considering its EPS might grow ~40% this year and double-digit thereafter[85]. If the market comes to view Seagate as a secular growth story rather than a cyclical, it could even award a higher multiple. For instance, one analysis posited that if Seagate hits ~$15 EPS in a couple years and gets a 30× P/E (for its above-average growth), the stock could approach $450 (versus ~$320 now)[87][88]. While that may be optimistic, it illustrates that continued execution could reward investors further. In the meantime, shareholders enjoy dividends and buybacks as they wait.

Bear Case: Risks, Threats, and Skepticism

- SSD (Flash) Encroachment Risk: The biggest strategic threat to Seagate is the relentless improvement of solid-state storage. Bears warn that HDDs could face an accelerated decline if flash memory breakthroughs continue. We’re already seeing 3D NAND roadmaps that envision 200+ TB SSDs within a few years[36][89]. As manufacturing scales, the cost per bit of flash is coming down. The bear case scenario: sometime late this decade, SSDs reach a tipping point where their TCO (considering power, cooling, speed) beats HDDs even for bulk storage[90][91]. Especially for AI infrastructure, where performance and energy matter, large hyperscalers may opt to gradually replace HDD arrays with high-density SSDs despite higher upfront cost[37][38]. The article “HDDs Can’t Compete with the Shift to SSDs in AI” articulates this view: for AI clusters needing fast throughput and efficiency, HDDs become bottlenecks, and with SSD capacities skyrocketing (128TB now, 256TB/512TB soon), the case for HDDs in cutting-edge data centers could erode[36][92]. It even argues that by the time HDD hits 100TB, SSDs might be at 1PB, and new architectures (like NVMe-over-fabrics, computational storage, etc.) will favor solid-state[92][93]. If this vision holds, HDD demand could peak and then secularly decline sooner than expected, leaving Seagate’s long-term growth in jeopardy. In short, the bear case sees HDDs as a stop-gap technology in an AI age that ultimately demands silicon-based storage.

- Cyclical Downturn / Saturation Concerns: Skeptics point out that Seagate is coming off a cyclical high, and extrapolating current growth into the future could be dangerous. Hyperscalers may have been on an unusually large buying spree in 2024–25 (partly catching up from pandemic delays and fueling AI projects). Once they build out sufficient capacity, orders might slow (“digestion period”). There are already hints: Seagate’s management expects growth to moderate to low-to-mid teens CAGR instead of the 30-40% spike seen in the past year[81]. Any sign of inventory build-up at customers or a pause in cloud capex could hit Seagate’s revenues hard (as happened in prior cycles). Storage remains a cyclical industry tied to capital spending patterns – it’s not immune to macro recessions either. If the global economy weakens or if cloud providers optimize their existing storage usage (through compression, better data management), the rapid sales growth could stall. Bears recall that just a couple years ago, in 2022, Seagate’s quarterly revenue plunged below $1.7B and the company had to cut jobs and costs. The volatility hasn’t necessarily disappeared, it’s just masked by the current upswing. A related risk is pricing reversion: the current ability to raise prices may not last. As supply catches up (Seagate and WD both ramping production, plus any inventory builds), pricing could revert to its deflationary trend, squeezing margins again.

- Valuation and Expectations: After a 200%+ stock run, Seagate’s valuation now embeds a lot of optimism. The stock trades around 23–25× earnings and ~23× free cash flow[94], which is historically high for Seagate (a company that used to trade at low-teens multiples as a slow-growth cyclical). If growth indeed slows to teens and the storage cycle normalizes, that multiple could compress. Some analysts have flagged that at these levels, the risk/reward is less favorable – any hiccup in execution or guidance could send the stock down. For instance, Seeking Alpha’s quant models or some fund managers have recently rated STX a Hold after its rally, citing an elevated valuation and potential ~20% downside if the market re-rates it closer to peers[95]. In essence, the “AI storage” story is well known now – future gains require delivering on high expectations. If, say, cloud AI demand disappoints or Seagate’s margin expansion stalls, the stock could correct. Moreover, as a hardware supplier, Seagate doesn’t have the software-like sticky revenues that command premium multiples; it remains vulnerable to commoditization concerns longer-term.

- Technological Execution Risks: While Seagate is ahead on HAMR, bears note that new technologies can bring growing pains. Potential issues include: lower initial manufacturing yields (raising costs), reliability problems in the field (HAMR drives use lasers and run hotter – will they meet the 5+ year longevity requirements without higher failure rates?), and customer hesitation to adopt too quickly (some cloud players might wait for second-gen HAMR or demand steep discounts for early units). If any such issues arise, Seagate could face delays or extra expenses. Western Digital, though behind, could leapfrog if Seagate encounters trouble – or WD’s interim UltraSMR strategy might grab more share if HAMR supply is constrained. In short, being first is not a guarantee of smooth sailing; execution is critical. Additionally, Seagate’s heavy focus on one technology (HAMR) means it has a lot riding on it. For example, if a competing method (like Microwave-Assisted or some yet unknown tech) proved superior or if flash costs drop faster than HAMR can keep up, Seagate’s R&D bet might not pay off as expected. The bears highlight that Seagate lacks diversification – unlike WD, it has no significant presence in flash memory. If HDD technology’s limits are eventually reached or its market shrinks, Seagate can’t fall back on another division. This single-track focus amplifies risk in a long-term sense.

- Customer Concentration & Competitive Pressure: A few large cloud companies constitute a significant portion of Seagate’s sales. This concentration poses risk: these savvy customers exert pricing pressure and also dual-source between Seagate and WD to keep deals competitive. If one major hyperscaler (say, Amazon or Google) decided to shift more business to WD (perhaps preferring their drives or negotiating a better bundle deal including SSDs), Seagate could lose share. Competition between Seagate and Western Digital can at times lead to price competition – for instance, if one has excess inventory or aggressively cuts price to win a big cloud account, the other may have to follow, impacting industry margins. Also, if Toshiba or a new entrant (maybe a Chinese company) were to make technological advances, they could nibble at the market (though currently this threat is minimal). All told, while the duopoly is generally favorable, there’s always the risk of “irrational competition” or a big account loss that dents profitability.

- Sustainability of AI Demand: The current narrative heavily leans on AI as a perpetual growth engine for storage. Bears question whether this is somewhat hype-driven and potentially transient. It’s possible that after the initial wave of AI model training (which involved storing enormous datasets), future efficiency improvements could reduce storage intensity. For example, techniques like data pruning, better simulation (reducing the need to store so much raw data), or simply that once foundational models are trained, incremental data needs might level off. If AI investment goes through its own cycle (a burst of spending followed by a plateau), storage demand might reflect that. Additionally, enterprises might not store everything – data lifecycle management could improve, meaning companies delete or archive data to tape/cloud archive rather than keep buying new nearline drives. There’s also the scenario that some AI workloads might shift to real-time data generation (simulated data) that doesn’t need long-term storage. In summary, the “AI will keep storage demand skyrocketing” thesis may face nuances; any sign of AI spending slowdown could temper the enthusiasm around Seagate.

- Macro and Other Risks: Broader risks include the cyclical nature of tech spending (discussed), but also geopolitical and regulatory factors. For instance, Seagate ran afoul of U.S. export regulations by shipping drives to Huawei, resulting in a $300 M fine in 2023[96]. While that issue is resolved (with Seagate paying the penalty over time), it highlights the complexities of global tech supply chains. Trade restrictions, tariffs, or export bans (e.g. on selling to certain Chinese cloud companies) could impact Seagate’s revenue in those markets. Conversely, China has an initiative to reduce dependence on foreign tech – if they invest in domestic HDD or alternative storage tech, that could eventually increase competition. Another risk is the physical nature of Seagate’s products: HDD manufacturing relies on components (motors, heads, substrates) that could face supply chain issues or cost inflation, and shipping drives around the world is a logistics effort that could be disrupted by events (natural disasters, etc. – recall floods in Thailand in 2011 severely affected HDD industry). While these are not front-of-mind daily concerns for investors, they are part of the risk mosaic.

The bear case contends that Seagate, despite riding a high, still faces significant challenges. It must navigate a potential normalization of demand, keep innovating to stave off SSDs, and justify its newly rich valuation. If anything goes wrong – whether a tech hiccup or a macro slowdown – the stock could pull back. From $300+ levels, there isn’t much margin for error in execution.

Risks & Challenges

Expanding on some of the risks discussed, here are the key challenges Seagate faces as it looks ahead:

- Technological Disruption: The threat of storage technology disruption looms large. The most immediate is the rise of NAND flash and SSDs encroaching on high-capacity roles. While HDDs still win on cost/GB, the gap is shrinking when factoring in power, cooling, and density. As noted, enterprise SSDs could be 5× faster and eventually approach similar $/TB when fully loaded with data[97][98]. There are also emerging storage techs (still experimental) like DNA storage, optical storage, or improved tape systems that could long-term present alternatives for archival storage. Seagate has to continuously innovate (e.g. HAMR now, possibly next-gen HAMR or other energy-assisted methods later) to avoid being leapfrogged. If the company misses a key tech inflection or if HAMR under-delivers (e.g., plateauing at some capacity that flash then overtakes), Seagate’s core business could erode quickly. Essentially, the company is in a race to keep HDDs “good enough, cheap enough” before solid-state storage eats more of the pie. This is a fundamental strategic risk.

- Market Cyclicality: Despite structural growth factors, Seagate’s business is still exposed to boom-bust cycles in capital spending. A significant portion of sales is tied to a handful of big buyers whose ordering patterns can swing quarter to quarter. History shows that after periods of expansion, the storage industry often hits overcapacity or demand pauses that lead to sharp price declines and volume drops. For example, if hyperscalers decide in 2026 to slow down data center expansions (maybe because they invested a ton in 2024–25, or macroeconomic pressures), Seagate could see a rapid deceleration in orders. This cyclicality is compounded by inventory management – if customers over-order and build inventory, they might suddenly cut purchases to burn off stock, hitting Seagate’s revenue. The company has tried to mitigate this with BTO contracts (which give some guaranteed off-take), but contracts can sometimes be deferred or renegotiated if demand really falls short. Additionally, as a manufacturer, Seagate has high fixed costs; a drop in volume can quickly compress margins if factories aren’t filled. The challenge for Seagate is to manage production and expenses prudently so that it can weather the down cycles without too much pain. Nonetheless, investors must recognize that volatility is inherent – results can swing significantly with the cycle (as seen in the ~$6.5B revenue in FY2024 to $9.1B in FY2025 swing).

- Competitive Pressure: Although only a few competitors exist, the competition between them is intense. Western Digital in particular will not cede market share easily. We can expect WD to push aggressive pricing or promotion of its drives (like SMR drives boasting higher effective capacity) to win deals. If WD successfully convinces more customers to adopt UltraSMR or if their forthcoming HAMR drives perform well, Seagate could face pressure on its sales growth or be forced to price-match. There’s also a scenario of pricing competition if, say, the market slows – both Seagate and WD might cut prices to chase limited demand, hurting margins. Moreover, WD’s integration of HDD and flash means they could offer bundle deals (e.g., selling a package of SSDs + HDDs to a cloud client at a discount), something Seagate can’t directly do. Competitive risk also includes Toshiba increasing its play in nearline drives or technology licensing (imagine if a big customer like Amazon funded a new entrant or internal project to develop HDDs – unlikely but not impossible if they ever view the duopoly as too restricting). In short, Seagate must execute better than its rivals to keep its edge – any slip and customers have alternatives.

- Sustainability of AI Demand: One current risk is that the hype around AI could overshoot actual long-term needs. Cloud providers are spending heavily on AI infrastructure now, but if ROI doesn’t meet expectations or if end-user demand for AI services plateaus, there might be a pullback. AI training datasets won’t grow infinitely large; there are practical limits and diminishing returns. If we reach those or if the industry shifts to focusing on quality of data over sheer quantity, the exponential storage demand could level off. Another aspect: AI companies are also working on techniques to reduce data requirements (like synthetic data generation to augment smaller real datasets, or more efficient algorithms that don’t need trillions of examples). Regulatory or societal limits on data collection (privacy laws, etc.) could also curb some data hoarding. So while AI is a boon now, it’s worth monitoring whether this is a multi-year secular trend or something that normalizes. If AI-related demand were to unexpectedly cool, Seagate’s growth rate might revert to the low single digits typical of a mature industry, disappointing investors who priced it as a high-growth stock.

- Execution & Operational Challenges: On a day-to-day basis, Seagate faces execution challenges. Ramping a new technology like HAMR involves hitting yield targets, scaling component supply (e.g., lasers, new media), and avoiding quality issues. If, for example, a manufacturing bottleneck occurs (say the laser supplier can’t meet volume or a cleanroom issue reduces head output), Seagate might have trouble fulfilling orders – especially problematic given they’ve committed capacity to customers. They also must manage the transition from PMR to HAMR carefully – too slow, and they might lag demand for bigger drives; too fast, and they risk having excess cost or obsoleting existing inventory. Supply chain management is another issue: HDDs have many parts, and disruption in any (motors, IC controllers, etc.) could pinch production. The company’s global operations (with manufacturing in countries like Thailand, Malaysia, China, US) expose it to logistical and geopolitical risks as well. Cost inflation in components or labor could nibble at margins unless offset. And concurrently, Seagate needs to continue developing future technologies (like HAMR generations, possibly HAMR+SMR combinations, or other tricks) – R&D execution is key; a misstep could let competitors catch up or alternative storage solutions gain ground.

- Regulatory and Geopolitical Risks: As noted, Seagate had a run-in with U.S. export authorities for selling drives to a blacklisted entity (Huawei) and paid a hefty fine[96]. This underscores that as a global supplier, Seagate must navigate trade restrictions carefully. U.S.-China tensions remain a backdrop; HDDs aren’t high-tech chips, but they still fall under certain export rules if they contain U.S. technology. Future sanctions or export controls could limit sales to certain countries or customers (for instance, if more Chinese cloud firms were restricted, Seagate could lose business there, although currently it’s still allowed to sell broadly). Conversely, China might push for domestic alternatives (there have been reports of China investing in its own HDD R&D, but it’s a steep hill given Seagate/WD’s decades of IP). Another regulatory aspect is antitrust – unlikely against a duopoly that’s existed for long, but if Seagate and WD are seen as too cozy, there’s theoretical risk of regulators scrutinizing pricing practices (no signs of that currently; the market is competitive enough and customers like cloud giants have negotiating power). Finally, macro issues like currency fluctuations (Seagate reports in USD but sells globally), interest rates (affecting tech spending budgets), and global economic growth all feed into demand for storage.

Seagate’s management has to stay ahead of the curve on technology, keep a tight ship operationally, and adapt to market swings, all while facing a future where the ground could shift if solid-state storage makes bigger inroads. These risks are not lost on investors – they form the basis of the cautious view on Seagate even amid the current optimism.

Forward-Looking Outlook

So, what does the road ahead look like for Seagate, and what key catalysts and uncertainties should investors watch?

Key Catalysts to Watch:

– New Product Launches (High-Capacity Drives): In the near term, a major catalyst will be Seagate’s introduction of its next-gen HAMR drives. Management has guided for a 4 TB/platter HAMR platform ramping in H1 2026[99], which likely means a flagship drive around 40 TB. Successful launch and customer uptake of these 32TB–40TB drives will be an important validation of Seagate’s technology leadership. Each bump in capacity could spur a replacement cycle as cloud providers upgrade to denser drives to save space/power. Additionally, Seagate’s roadmap mentions a path to 10 TB per disk (which implies 80–100 TB drives eventually)[57] – any concrete progress or prototypes shown of, say, a 50TB+ drive would generate excitement and press. On the flip side, competitor product news is also crucial: if Western Digital announces its own HAMR timeline or releases a 30+TB drive (e.g., with SMR or a surprise HAMR entry), that could be a catalyst affecting the competitive balance. Keeping an eye on industry trade shows and announcements (like the Open Compute Project summit or Flash Memory Summit, where storage advances are often revealed) will be useful.

- Hyperscaler Capex and AI Investment: Another catalyst is the continuation (or not) of heavy cloud capex for AI and storage. Watch the earnings and capex guidance of major cloud players (Amazon, Microsoft, Google, Meta) – if they signal ongoing large investments in data centers, that bodes well for Seagate’s nearline drive demand. For instance, Meta’s commentary in 2023 about increasing AI capacity indirectly pointed to more storage purchases. If in 2026–2027 we see announcements of new data center regions, expanded cloud offerings, or AI initiatives (like bigger models, more GPU clusters), that implies more storage needed to support them. Conversely, if these companies start talking about efficiency, cost cuts, or slowing buildouts (perhaps due to achieving capacity or macro pressures), it could foreshadow an order slowdown. Cloud demand visibility currently is good through mid-2026 by Seagate’s account[22], and they see visibility building into late 2026 – but beyond that, the trajectory will be telling.

- Pricing Environment & Supply Dynamics: Keep watch on industry pricing trends for both HDD and NAND flash. Right now, tight supply has allowed some HDD price increases[47]. A catalyst that could further boost Seagate is if supply remains constrained (perhaps due to cautious capex or any production hiccups) while demand stays strong – this could allow additional pricing gains or at least stable pricing, directly aiding margins. However, if WD and Seagate both ramp output significantly in 2026 to chase demand, we might return to overcapacity. Also, NAND flash price trends matter: if flash prices suddenly spike (say due to a supply disruption or a surge in demand for SSDs), that could indirectly benefit HDDs as a cheaper alternative. Alternatively, if flash enters another glut and becomes ultra-cheap, some customers might choose SSDs for slightly colder data, potentially cannibalizing a bit of HDD demand at the margins. Analysts and industry publications (like TrendFocus, IDC, or TrendForce) often provide updates on exabyte shipments and pricing – those will be good forward indicators.

- Financial Milestones: On the financial side, upcoming earnings reports and guidance will be catalysts. If Seagate continues to post strong growth and beats estimates (like its big Q1 FY26 beat that sent shares up double digits[100]), that momentum could drive the stock higher. Particularly, watch if Seagate reaches or exceeds certain targets: e.g., hitting that 40% gross margin goal ahead of FY2028[56], or crossing $3B in quarterly revenue (their incremental margin target of ~50% kicks in at $2.6B/quarter[101][56]). Also, any increase in shareholder returns (like dividend hikes or accelerated buybacks) could boost investor sentiment. The company’s execution against its new FY2028 financial model (low-teens CAGR, 40% GM, 10% OpEx) will be a barometer of how well reality matches the Analyst Day optimism.

- Corporate Actions and Industry Moves: Potential catalysts beyond Seagate’s direct control include strategic moves in the industry. For instance, Western Digital’s deliberations on splitting off its flash business – if that happens, how will it impact the HDD unit’s strategy? Some speculate that a separated WD HDD business could potentially consider closer alignment or even a merger with Seagate (though regulatory hurdles would be high for a full merger). Even short of that, any consolidation or collaboration could alter industry dynamics. Another angle: M&A or partnerships – Seagate might look to acquire technologies or companies (perhaps in areas like cloud services, or specialized storage software) to augment its offerings, which could be viewed positively if it fills a strategic gap. Additionally, if major customers initiate long-term agreements (for example, a multi-year supply agreement with prepayments, similar to what some chipmakers did with foundries), that could be a catalyst by de-risking future revenue.

Major Uncertainties:

– Pace of Technology Transition: A key uncertainty is how fast HAMR will be adopted and perform. Seagate’s entire growth and margin expansion plan hinges on HAMR ramping smoothly. Will customers transition quickly to buying mostly HAMR drives by 2026–2027? Or will they be cautious, sticking with known PMR tech longer (especially if WD offers 30TB SMR drives without needing HAMR)? The speed at which Seagate can convert its product line to HAMR and retire older platforms will affect costs and average selling prices. Also uncertain is how competitors’ tech roadmaps play out – WD’s timeline for HAMR and any alternate tech (e.g., if they surprise with a breakthrough) could change the landscape.

- Long-Term Demand Elasticity: While data growth seems inexorable, the rate of growth and storage intensity per unit of data is uncertain. We have forecasts (mid-20s% exabyte CAGR[42]), but these could be off if, for example, data compression or better data management improves. Another question: to what extent will enterprises continue to store data on-premise vs. cloud vs. delete? The mix of storage spending could shift – if more organizations decide to archive data in ultra-cheap cold storage (even tape or glacier-like services) rather than keep spinning disks, nearline HDD demand might be slightly less. The balance of hot vs cold data could also shift with AI: if real-time analytics become crucial, more investment might go to fast storage relative to bulk storage. In summary, there’s uncertainty around how the data will be stored, not just how much data there is.

- Macro-Economic Factors: The broader economic environment is always an uncertainty. In times of tight IT budgets or economic downturn, expansions can be delayed. Conversely, if the economy is strong, companies might invest more in digital infrastructure. Interest rates and cost of capital can influence large capex decisions (building a data center is capital intensive, so higher rates could make companies more cautious). Currency fluctuations are another factor (Seagate sells globally, and a strong dollar can impact international sales). While these aren’t unique to Seagate, they overlay uncertainty on its forward outlook.

- Regulatory/Government Policy: As touched on, government actions can introduce uncertainty. Export controls could limit some market access, or government incentives could bolster a competitor (e.g., if a national program in China heavily subsidized a local HDD developer – not likely to immediately succeed, but a long-term wildcard). Environmental regulations are an emerging area: data centers consume a lot of energy, and there’s growing scrutiny on making them greener. HDDs use more power per TB than tape or even some flash configurations; if policies or customer CSR goals push for lower carbon footprint storage, it might influence buying patterns (for instance, favoring fewer, larger HAMR drives since they are more energy-efficient per TB, which could actually help Seagate if it leads in capacity).

- Long-Term Relevance in an Exploding Data World: Looking out to the far horizon, the question is how relevant Seagate will remain if the world’s data truly explodes to zettabytes per year. On one hand, one could argue Seagate’s opportunity is essentially limitless as long as it keeps innovating – there will always be demand for cost-effective storage, and Seagate can be a key supplier for the foreseeable future. The company itself is confident it can “lead the next era of storage in today’s data-driven world” with the right technology and strategy[102][19]. On the other hand, if we think 10+ years out, we must consider a world where storage might be predominantly solid-state (if flash or successor technologies become extremely cheap and dense) and perhaps where cloud architectures change (for example, more distributed edge storage or new memory/storage hierarchies could lessen the use of spinning disks). Seagate’s long-term relevance will depend on its ability to adapt – perhaps even diversifying beyond spinning media if needed. They’ve begun branding as a “mass-data storage” company, not just an HDD maker, which is a nod to staying relevant no matter the medium (devices, systems, services from edge to cloud[1]). Whether that means eventually embracing non-HDD tech or doubling down on making HDDs unbeatable in cost is a strategic choice.

So in conclusion, Seagate’s outlook in the next 2–3 years looks positive barring a major surprise: demand drivers are intact, and the company is executing well on its technology and financial plans. Key things to watch are execution of the HAMR ramp (product and cost), the sustainability of hyperscaler orders, and any signals of tech transition in the industry. The long-term vision sees Seagate playing a pivotal role in storing the ever-growing sea of data – but the exact shape of that role will be determined by how well the company navigates the challenges and uncertainties above. For tech investors, Seagate represents a fascinating case of an “old” technology company that has reinvented itself to ride some of the most cutting-edge trends in AI and cloud. The coming years will reveal if it can continue to balance innovation with discipline, and remain a cornerstone of the data economy or if the rapid shifts in tech will require yet another evolution of its business.

最终,Seagate的故事反映出这样一个事实:在数据爆炸的时代,即使是传统的存储公司,也可以通过技术创新和战略转型,在现代AI经济中扮演关键角色。投资者将密切关注其下一步动作,因为这不仅涉及一家公司股票的涨跌,更关乎我们如何存储和管理未来海量的数据洪流。

Sources: Recent Seagate earnings reports and analyst event materials; Western Digital and industry reports on HDD vs SSD trends; Motley Fool, Seeking Alpha, and other tech-investing commentary for stock performance and narrative[4][3][30][16][2], among others, as cited throughout the report.

[1] [13] [14] [19] [55] [56] [57] [58] [83] [84] [86] [101] [102] Seagate Highlights Strategy to Build Long-Term Value in Today’s Data-driven World at 2025 Investor and Analyst Event | Seagate US

[2] [3] [7] [12] [18] [47] [70] [71] [75] [76] [77] [78] [79] [85] [87] [88] This Artificial Intelligence (AI) Stock Quietly Outperformed Nvidia in 2025. It Can Continue Soaring in 2026. | The Motley Fool

[4] [5] [67] [68] [69] [74] Seagate – Seagate Technology Reports Fiscal Fourth Quarter and Fiscal Year 2025 Financial Results

[6] [22] [23] [42] [43] [44] [45] [46] [62] [65] [72] [73] [80] [99] Seagate (STX) Q4 2025 Earnings Call Transcript | The Motley Fool

[8] [9] [24] [25] [35] [60] [61] [63] [64] Western Digital roller coaster continues as Seagate brings down the HAMR

Western Digital roller coaster continues as Seagate brings down the HAMR

[10] [11] [48] [49] [50] [51] [52] [53] [54] [66] Analyst Day 2025

[15] [16] [17] [81] [94] [95] Seagate Technology: AI’s Silent Winner Up 220% – Here’s What Happens Next (NASDAQ:STX) | Seeking Alpha

[20] [21] [26] [27] [28] [30] [31] [32] [33] [34] [39] [40] [41] A Balancing Act: HDDs and SSDs in Modern Data Centers

A Balancing Act: HDDs and SSDs in Modern Data Centers

[29] Will SSD replace HDD in the future? : r/datastorage – Reddit

[36] [37] [38] [89] [90] [91] [92] [93] [97] [98] HDDs Can’t Compete with the Shift to SSDs in AI Infrastructure

[59] Seagate vs. Western Digital: Which Storage Stock is the Better Buy …

[82] STX-FQ3-25-Press Release

[96] Seagate to pay $300 million penalty for shipping Huawei 7 … – Reuters

[100] Seagate’s Massive Q1 Beat Shows the Power of AI Demand | Trefis