November 4, 2025

SK hynix: Powering the Future of Memory and Semiconductor Innovation

Business Model and Major Products

SK hynix Inc. is a South Korean integrated device manufacturer (IDM) specializing in memory semiconductors. Its core business is the design, manufacture, and sale of memory chips, notably dynamic random-access memory (DRAM) and NAND flash memory[1][2]. In recent years, SK hynix has also expanded into solid-state drives (SSDs) – especially enterprise SSDs – following its 2021 acquisition of Intel’s NAND and SSD business. This has made SK hynix a full-stack memory provider, offering everything from raw memory chips to finished storage drives[3][3]. The company’s products are widely used in PCs, mobile devices, servers, and consumer electronics; major clients include industry leaders like Apple, Microsoft, Dell, and HP[4]. SK hynix operates its own fabrication facilities (fabs) and R&D, giving it end-to-end control over production as an IDM[5][2].

Role in the Semiconductor Industry: SK hynix is one of the world’s largest semiconductor vendors, ranking as the second-largest memory chip maker globally (trailing only Samsung Electronics)[2]. It commands a significant share of the DRAM market and, after integrating Intel’s NAND unit, is also a top-tier player in NAND flash. In the fast-growing AI segment, SK hynix has emerged as a pioneer in “AI memory.” It leads in cutting-edge High Bandwidth Memory (HBM) – a specialized DRAM for advanced computing – with about 62% of the global HBM market as of mid-2025[6]. In fact, SK hynix is the primary HBM supplier for NVIDIA’s AI GPUs[7], underscoring its pivotal role in the AI hardware ecosystem. Overall, the company’s position can be likened to one leg of the “memory oligopoly” alongside Samsung and Micron; these three dominate global memory supply.

Key Growth Drivers for Revenue

Several factors are driving SK hynix’s growth and revenue:

- Data Center & Server Demand: Explosive growth in cloud computing and AI has fueled demand for advanced memory. SK hynix’s sales of server-grade DRAM (like DDR5) and HBM have surged – in 4Q 2023, shipments of DDR5 and HBM3 were 4–5× higher than a year earlier[8] as AI servers and new processors require much more memory. Hyperscale cloud companies are investing heavily in memory to support AI training and big-data workloads, which directly benefits SK hynix.

- Mobile and 5G: Smartphones (especially 5G devices) and other consumer gadgets continue to need more memory and storage. SK hynix is a leading supplier of mobile DRAM (LPDDR) and high-density NAND for smartphones. Although the smartphone market slowed in 2022–2023, the rollout of 5G and increasingly memory-heavy apps mean the long-term trend is upward.

- Enterprise SSD & Storage: With the Intel NAND acquisition, SK hynix (through its subsidiary Solidigm) expanded into enterprise and data center SSDs. This opened a new revenue stream by allowing SK hynix to sell not just flash chips but complete storage solutions. Enterprise SSD demand is rising as data centers replace hard disks with faster flash storage.

- Product Mix & Technology Leadership: SK hynix’s focus on cutting-edge technologies gives it pricing power. It was early to market with HBM3 and is now moving to HBM3E and HBM4 development[9]. Its technological edge lets it charge premium prices for high-performance chips. Similarly, in NAND flash, SK hynix is producing high-layer count 4D NAND (TLC and QLC) and focusing on profitable segments (like SSD and high-capacity drives) to drive revenue[10][11].

- Strategic Partnerships and Ecosystem: The company also benefits from collaborations within the SK Group and externally. For instance, SK hynix and NVIDIA announced a partnership to build an “AI factory” with 50,000 GPUs, aiming to advance next-gen memory solutions for AI[12][13]. Such partnerships not only secure future demand but also accelerate SK hynix’s innovation, reinforcing its revenue drivers.

Summary: In essence, SK hynix’s growth is fueled by secular trends – the world’s appetite for data and computation – which translate to higher demand for memory. From the AI boom to 5G and cloud services, SK hynix’s chips are critical enablers. Its ability to innovate (e.g. HBM leadership) and its broadened product lineup (DRAM, NAND, SSDs) have positioned the company to capture rising memory content across tech devices.

Stock Performance Over the Past 5 Years

Share Price Trends and Influencing Factors

Over the last five years, SK hynix’s stock has experienced significant volatility in tandem with the memory industry’s boom-bust cycles and macro events. Overall, the stock’s trajectory can be divided into a few phases:

- 2019–2020 Upswing: After a memory downturn in 2018, SK hynix shares rebounded strongly in 2019 (rising about +50.6%)[14]. This momentum continued into 2020 with a further +33.5% gain[15] as global demand for tech surged. In 2020, pandemic-driven trends (remote work, online services) boosted memory demand for PCs and servers. Additionally, a global chip shortage in late 2020/early 2021 – while primarily affecting logic chips – created a positive sentiment across the semiconductor sector. SK hynix benefited from strong memory pricing and record earnings in 2020–2021, which lifted its stock.

- 2021 Peak and Mild Correction: By early 2021, memory prices were near cyclical highs and SK hynix’s stock reflected optimism for continued growth. However, the stock saw a modest pullback in 2021 (about –3.6% for the year)[16]. This was partly because investors anticipated a mid-cycle cooldown – PC and smartphone markets showed signs of saturation and memory supply was catching up. Indeed, Samsung Electronics (a broader tech bellwether) also had a slight stock decline in 2021 (around –12%)[17]. In short, 2021 marked a pause as the market priced in a potential end to the extremely tight chip supply of 2020.

- 2022 Downturn: The year 2022 saw a sharp downturn for SK hynix’s stock, which plunged roughly –44.5%[18]. Several factors drove this: a glut in memory chips emerged as manufacturers (including SK hynix) ramped output just as demand for PCs and smartphones cooled post-pandemic. Global macroeconomic headwinds (rising inflation and interest rates, war in Ukraine, etc.) dampened consumer electronics sales, causing memory prices to crash. SK hynix also faced its first operating loss in a decade by late 2022[19]. Investor sentiment soured on memory makers, and SK hynix’s shares reflected those challenges. Notably, Samsung’s stock fell ~–32% in 2022[17], and U.S. rival Micron Technology dropped as well. (Micron’s fiscal 2022 saw steep profit declines, and China’s ban on Micron’s chips in critical infrastructure that year added to uncertainty[20].)

- 2023 Strong Recovery: In 2023, SK hynix staged a remarkable recovery – the stock soared about +84% for the year[18]. This turnaround was propelled by a memory market rebound in the second half of 2023. Industry conditions improved as suppliers cut production and excess inventory cleared. More importantly, demand for AI server memory exploded, requiring large quantities of DRAM and especially HBM (high-bandwidth memory) for AI accelerators. SK hynix, being a leader in HBM, saw a surge in orders. By Q4 2023 the company returned to quarterly profit[21], signaling the worst was over. Market optimism about an “AI boom” drove SK hynix shares upward. The trend mirrored other chip stocks: Samsung Electronics rose ~40% in 2023[17], and Micron’s stock also climbed as the memory cycle bottomed out. In fact, over the five-year span ending 2023, Micron had outperformed many peers – its stock was up ~137% vs. 2018, whereas Intel’s was down ~55% in the same period[22] – highlighting how memory-focused stocks rebounded strongly from cyclical lows.

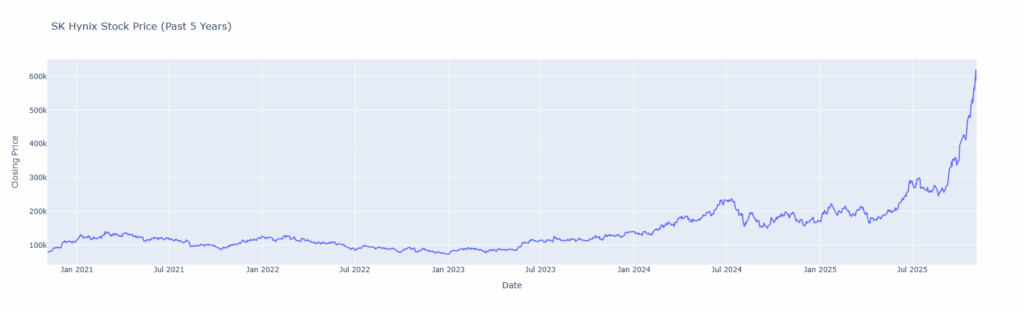

- 2024–2025 Surge to New Highs: In 2024 and into 2025, SK hynix’s rally accelerated further. The stock not only regained pre-2022 levels but hit record highs by 2025[23]. Year-to-date 2025, SK hynix shares had skyrocketed (up nearly +277% by November 2025, according to market data[24]). This dramatic climb was fueled by euphoric investor sentiment around AI: Nvidia’s blockbuster growth in 2023–2024 underscored the value of AI-related suppliers like SK hynix. In mid-2025, SK hynix’s market capitalization reached ₩213 trillion (~$157 billion)[25], making it the second-most valuable company in Korea after Samsung. News of record quarterly earnings (e.g. a >₩11 trillion operating profit in Q3 2025) and sold-out order books for next-generation memory reinforced the bull case. By late 2025, SK hynix’s stock was trading at its highest level since the dot-com era[26].

In summary, market trends and events have strongly impacted SK hynix’s stock. Cyclical memory pricing has been the dominant factor: during upcycles (2019–early 2021, and again 2023–2025) the stock delivered outsized gains, whereas in downcycles (2018 and 2022) it suffered steep losses. Broader market forces amplified these moves – e.g. the COVID-19 tech boom lifted it, while global recession fears sank it. Company-specific news (such as the Intel NAND acquisition or major capex announcements) has been secondary to these larger industry swings in influencing the share price.

Comparison to Major Competitors

When comparing SK hynix’s stock performance to Samsung Electronics, Micron Technology, and Intel over a five-year horizon, a few points stand out:

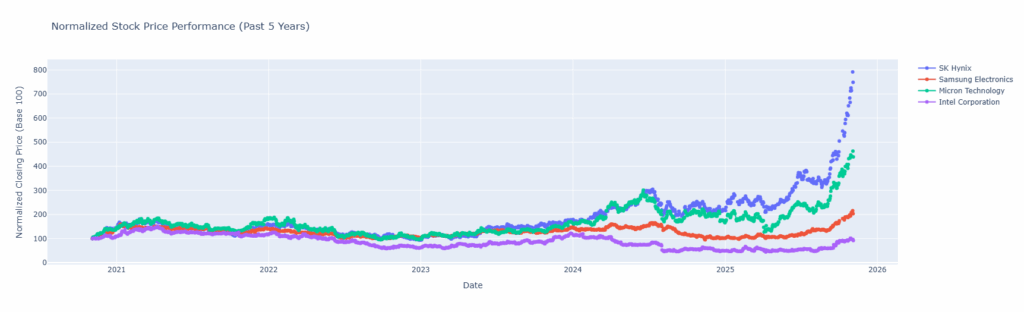

- Samsung Electronics (KRX:005930): As a diversified tech giant (memory, logic chips, consumer electronics), Samsung’s stock has been less volatile than pure-play memory makers. Nonetheless, it followed a similar pattern: strong gains in 2019–20, a dip in 2021, a sharp drop in 2022, then recovery in 2023. For example, Samsung’s share price jumped +62% in 2020, dipped in 2021, fell –32.5% in 2022, and rebounded +40.6% in 2023[17]. Over five years, Samsung’s total return is positive but moderate (roughly +60–80% from 2018 to late 2023, factoring in dividends). SK hynix’s stock, being more narrowly focused on memory, outpaced Samsung in upswings (e.g. +84% vs +40% in 2023) but also fell harder in the bust (–45% vs –32% in 2022). By 2025, both stocks hit all-time highs, but Samsung’s market cap (~$475 billion) remains much larger[27]. In essence, SK hynix provided higher risk-reward: bigger rallies during memory booms and deeper drops during slumps, whereas Samsung’s broader business buffered its stock somewhat.

- Micron Technology (NASDAQ: MU): Micron, the leading US-based memory maker, is perhaps the most direct comparable to SK hynix. Both have similar product portfolios (DRAM and NAND). Over the past five years, Micron’s stock performance has been very strong, outpacing even SK hynix’s on some measures. From 2019 to October 2024, Micron’s stock price soared ~137%, whereas Intel’s fell by more than half in that period[22]. Micron’s strong run continued into 2023–25 alongside SK hynix: in the last 12 months alone, SK hynix returned +203% versus Micron’s +112%[28]. The two stocks tend to move in tandem with memory cycles, but Micron has enjoyed a premium as a U.S.-listed company with broader investor access. Notably, through mid-2025, Micron’s market cap (around $250 billion) was in the same ballpark as SK hynix’s (~$280 billion)[29][30], despite SK hynix’s larger revenue and earnings. This reflects a valuation gap (discussed below). Both companies were hit by the 2022 downturn (Micron had quarterly losses in 2023 similar to SK hynix) and then lifted by the AI-driven upturn. Overall, Micron and SK hynix have had comparable directional stock trends, but Micron’s five-year appreciation (especially factoring in its early 2021 peak and late-2023/2024 rally) has been at least on par if not higher. By late 2025, investors in both companies saw substantial gains from the 2018–2019 base – a testament to staying invested through the cycles.

- Intel Corporation (NASDAQ: INTC): Intel is not a memory pure-play (its main business is processors), but it’s a semiconductor heavyweight often compared for context. Over the past five years, Intel’s stock has underperformed dramatically relative to SK hynix. As noted, Intel’s share price fell ~55% (2019–2024)[22] due to a series of missteps – it lost technological leadership in CPUs, faced manufacturing delays, and missed the AI chip boom[31][32]. In contrast, memory firms like SK hynix were riding industry tailwinds part of that time. Even with a partial rebound in 2023–25 (Intel’s stock recovered from multi-year lows, reaching ~$175–190 billion market cap by late 2025)[33][34], Intel lagged far behind. For example, since January 2020, SK hynix’s stock roughly doubled, whereas Intel’s is roughly flat to down in the same span. The divergence highlights that SK hynix’s fortunes are tied to memory market cycles, while Intel’s are tied to its own CPU/GPU roadmap and competitive position – which have been challenged lately. From an investor perspective, SK hynix and Micron have been the big winners in semiconductors during the recent AI wave, handily outperforming Intel (and even the broader Philadelphia Semiconductor Index) over the last couple of years.

In conclusion, SK hynix’s stock performance has been strong over a five-year horizon, but with high volatility. It has outperformed a conglomerate like Samsung and a struggling giant like Intel, and has been in the same league as Micron’s impressive run. The key differentiator is the cyclical nature – SK hynix delivered superior returns for those who weathered the downturns. Each competitor had unique factors (Samsung’s diversification, Micron’s U.S. listing and tech strengths, Intel’s execution issues), but industry cycles and the recent AI trend have been the dominant drivers shaping all their stock trajectories.

Financial Health of SK hynix

Latest Financial Results (Revenue, Profitability, Margins)

SK hynix’s recent financial results underscore its cyclicality. After a difficult 2022–23, the company’s financial health improved dramatically in 2024:

- Revenues: In 2024, SK hynix achieved revenue of ₩66.19 trillion (Korean won)[1], which is approximately $48 billion USD (converted)[35]. This was a 92% increase from 2023, when sales had slumped to ₩32.8 trillion (about $24.9 billion) amid the memory glut[36][37]. The 2024 top-line was a record for the company, driven by recovery in memory prices and surging demand for its high-end products. By the first three quarters of 2025, SK hynix had already generated $55.3 billion in revenue (TTM)[35], indicating further growth on track, thanks to the ongoing AI-related boom.

- Profit/Loss: SK hynix swung back to profitability in 2024 in a big way. It posted a net income of ₩19.8 trillion in 2024[1] (roughly $15 billion USD after tax, converted). For context, the company had incurred a net loss of ₩9.14 trillion in 2023[38][39] due to the memory price crash. In other words, SK hynix went from its worst loss on record in 2023 to one of its best profits ever in 2024 – a dramatic turnaround. Operating profit in 2024 was ₩23.47 trillion (~$17.5 billion), equating to an operating margin around 35%, whereas 2023 saw a ₩7.7 trillion operating loss[38][40]. As of the latest quarters, profitability is still climbing: in Q3 2025, SK hynix reported its highest quarterly profit ever (₩12.6 trillion net profit in one quarter) amid the AI memory boom[41][25].

- Profit Margins: Given the above, SK hynix’s profit margins have rebounded to excellent levels. In 2024, net profit margin was roughly 30% (≈$15 billion net on $48 billion sales), and operating margin ~35%. These figures are well above industry averages for semiconductor companies. (For comparison, in “normal” years many chip firms have 15–20% net margins; even industry leader TSMC has ~30% net margins. SK hynix exceeding 30% underscores how lucrative memory can be in a tight-supply environment.) It’s worth noting that during the 2023 downturn, margins were deeply negative – the full-year 2023 net margin was about –28%[38][39]. Such wild swings are typical for memory makers. Over a full cycle, SK hynix’s average profitability might be lower than fabless peers or foundry companies, but in boom times it far surpasses them. For example, in mid-2025, SK hynix’s management commented that “just over half of every dollar of revenue is pure profit”[42] for the latest quarter – an astounding margin reflecting sky-high HBM prices and high factory utilization.

In summary, SK hynix’s financial health in 2024–2025 is very strong, following a brief weak period. Revenues have doubled from the trough and profits are robust, providing ample cash flow.

Balance Sheet and Debt Levels

SK hynix has maintained a solid balance sheet, and recent improvements in cash flow are helping it deleverage:

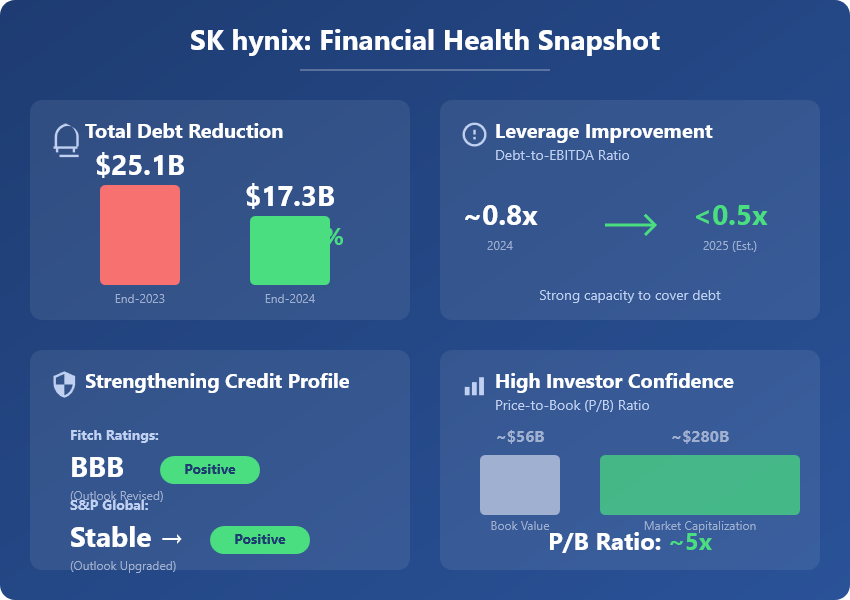

- Debt: The company’s total debt stood at about $17.3 billion USD at end-2024, a 31% reduction from roughly $25.1 billion a year prior[43]. During the 2023 downturn, SK hynix’s debt had risen (the company likely issued debt to cover losses and fund strategic investments), but the 2024 rebound enabled aggressive debt paydown. By traditional metrics, SK hynix’s leverage is now low – according to Moody’s and Fitch, debt-to-EBITDA is expected to fall below 0.5× in 2025 from ~0.8× in 2024[44]. This means the company generates enough earnings in one year to cover its debt almost twice over, which is a comfortable position.

- Cash and Liquidity: While exact cash figures aren’t cited here, SK hynix’s booming profits in 2024/25 have bolstered its cash reserves. In 2023, the company did experience cash burn due to losses and maintained CapEx, but it managed through that with available liquidity (including credit lines and support from parent SK Group if needed). By late 2024, free cash flow turned positive again, easing any liquidity concerns[45]. Furthermore, SK hynix can tap capital markets relatively easily as a large, partly conglomerate-backed firm in Korea.

- Credit Ratings: Reflecting the improved financial health, credit agencies have become more optimistic. In mid-2025, Fitch Ratings revised SK hynix’s outlook to “Positive” (while affirming a solid investment-grade rating of BBB)[46]. Fitch noted the rapid earnings recovery and debt reduction, though it also cautioned about demand uncertainty and U.S. trade policy impacts[46]. S&P Global similarly upgraded SK hynix’s outlook from Negative to Stable in early 2024, then to Positive, anticipating “significant improvement in debt leverage” thanks to the upcycle[45]. In short, SK hynix’s credit profile is strengthening, which should lower borrowing costs and give it flexibility for future investments.

- Equity and Book Value: As of 2024, SK hynix’s shareholders’ equity was around ₩73.9 trillion (≈$56 billion)[47]. With the stock’s market cap around $280 billion in late 2025, the price-to-book ratio is roughly 5. This is higher than during the downturn (when the P/B fell close to 1), indicating that investors are valuing SK hynix well above the accounting value of its assets – a sign of confidence in its earnings power.

Comparison to Industry Averages

Compared to industry peers and averages, SK hynix’s financial health metrics reflect the memory sector’s higher volatility:

- Revenue Growth: SK hynix’s ~92% revenue jump in 2024 was extraordinary, far above the semiconductor industry average growth (which might have been in the teens). This is because few other sectors swing so dramatically – memory demand and pricing can double revenue in a boom (as seen) or cut it in a bust. Over a multi-year period, SK hynix’s CAGR is still healthy (e.g. ~13% annual revenue growth from 2018 to 2024 in USD terms[37]), but not as smooth as, say, a microprocessor company.

- Profitability: At cycle peaks, SK hynix’s operating and net margins often outshine broader industry averages. For instance, in the late 2020/early 2021 period and again in 2024, its net margin ~30%+ is on par with or above giants like TSMC (~37% net in 2024) and well above diversified chip firms. However, the variance is huge – the company had negative margins in the trough. In contrast, a logic chip company or an IDM like Intel usually maintains positive margins even in weaker years (Intel’s struggles were more strategic, not cyclical). So one might say SK hynix’s average profitability over the cycle is respectable but not exceptional; what stands out is the high highs and low lows.

- Return on Equity (ROE): In a boom year like 2024, SK hynix’s ROE likely exceeded 20–25%. In bust years it was negative. The memory industry tends to have higher ROE swings than, e.g., fabless semiconductor firms which might have steadier ~15–20% ROEs.

- Debt/Equity: SK hynix’s debt-to-equity ratio is moderate and improving (debt ~30% of equity in 2024, down from ~45% in 2023 based on the figures above). This is roughly in line with industry norms. Memory peers often carry some debt to fund fab expansions; Micron, for example, also has a debt/equity around 0.2–0.5. In contrast, many fabless companies have little debt. So SK hynix’s leverage is satisfactory and now arguably conservative given its cash generation.

- Investment & Strategy: In the downturn, SK hynix pruned expenditures (it cut 2023 capital spending sharply and focused on cost reduction, especially in NAND[48][49]). This is a common industry response – Samsung and Micron did similarly. As the market rebounded, SK hynix ramped investment again: in Q1 2025 alone, it invested ₩7.4 trillion ($5–6 billion) in facilities/R&D – double the year-ago quarter[50]. Such counter-cyclical investment is part of its strategy to maintain technology leadership. From a financial standpoint, this means SK hynix is not hoarding cash excessively; it reinvests for growth, which is typical for leading chipmakers.

Overall, SK hynix’s financial health is robust relative to peers at this stage of the cycle. It has more volatility in results than a diversified peer like Samsung or an average semiconductor firm, but it currently enjoys above-average growth and margins. The company’s prudent balance sheet management (reducing debt during good times) and strong cash flow indicate it is well-prepared to handle future downturns or make strategic investments.

Recent news reinforces this view: analysts note SK hynix’s “remarkable turnaround” in late 2023 and 2024[51] and ratings agencies highlight vastly improved free cash flow and debt metrics[45]. Barring an unforeseen shock, SK hynix appears financially healthy and capable of funding its ambitious R&D and capacity expansion plans without compromising stability.

Market Trends and External Factors Impacting SK hynix

Macroeconomic Trends: Chip Shortages, Supply Chain, and Cycles

The last few years have seen unprecedented macro and supply chain events, which have directly impacted SK hynix’s business and stock price:

- Global Chip Shortages (2020–2021): During the pandemic, a surge in demand for electronics led to a global semiconductor shortage. While much of the news focused on auto and CPU chip shortages, memory was also tight in 2021. This benefited SK hynix in the short term – strong demand and limited supply meant higher prices. For example, in 1H 2021, DRAM and NAND prices were elevated, boosting SK hynix’s revenues and contributing to record earnings in that period. However, the shortage environment encouraged customers to double-order and manufacturers to increase output, which sowed the seeds for the later glut.

- Supply Chain Disruptions: COVID-19 and geopolitical issues disrupted global supply chains. For SK hynix, key impacts included logistics slowdowns (e.g. shipping delays could affect delivering chips to customers) and export control frictions. Notably, in 2019 Japan imposed restrictions on exports of critical semiconductor materials to South Korea (a dispute unrelated to COVID). This had potential to hinder SK hynix’s production (since those chemicals are needed for memory fab), but the company mitigated the impact by securing alternate suppliers and inventory. In general, SK hynix’s manufacturing is primarily in Korea (and some in China for certain products), so it navigated pandemic lockdowns relatively well, with its fabs largely staying operational. Nonetheless, supply chain hiccups added to cost pressures (expediting shipments, etc.) and inventory management challenges.

- Cyclical Oversupply (2022): After the 2021 boom, the memory industry went into oversupply in 2022–early 2023. This was a classic cyclical downturn exacerbated by macroeconomic factors: consumer demand for PCs/phones fell sharply as stimulus faded and inflation rose, just as memory suppliers (including SK hynix) had expanded capacity. The result was a steep drop in DRAM and NAND prices (over 50% decline in some cases). SK hynix was hit hard, with plummeting revenue and large losses[38][40]. The stock price, as discussed, mirrored this collapse. It’s worth noting macro factors like the war in Ukraine and China’s economic slowdown in 2022 affected overall tech spending, indirectly hurting memory demand further. SK hynix responded by cutting production (it idled some NAND flash capacity, for instance) and by reducing capex, aiming to help balance supply.

- Economic and Interest Rate Environment: Broad economic trends also play a role. In a high interest rate environment (like 2022–23), tech stocks and cyclicals tend to underperform as future earnings are discounted more and financing costs rise. Conversely, when rates stabilize or fall, these stocks often rebound. The anticipation of rate hikes in early 2022 contributed to a market rotation out of tech, which hurt SK hynix’s valuation. On the flip side, by late 2023, hopes that central banks would ease up coincided with the memory market bottoming, giving a double boost to SK hynix shares.

In summary, macroeconomic swings and supply chain issues have had pronounced effects on SK hynix. The company experienced whiplash from shortage to glut, and had to adjust rapidly. Its stock has effectively been a barometer of these global trends – soaring when chips are scarce and tumbling when there’s a glut.

Geopolitical Factors: Trade Wars and Regulations

Geopolitical developments are critically important for SK hynix, given its position in the global tech supply chain:

- US–China Tech Tensions: SK hynix finds itself in the crossfire of the ongoing US–China technology rivalry. The United States has imposed export controls on advanced semiconductor technology to China, and since late 2022 these rules have tightened. SK hynix operates a major DRAM fab in Wuxi, China, and a NAND flash fab in Dalian (the one acquired from Intel). U.S. rules require licenses for supplying cutting-edge chip equipment to these Chinese plants. Fortunately for SK hynix, the U.S. Commerce Department granted it (and Samsung) one-year waivers to continue normal operations in China[52]. These waivers, recently extended, allow SK hynix to ship needed tools and blueprints so far. However, the risk remains that future U.S. restrictions could hamper SK hynix’s China operations or cut it off from Chinese customers. China accounts for a significant portion of memory demand (many electronics manufacturers and cloud providers there use SK hynix chips), so losing access to the Chinese market would be a major blow.

- China’s Countermeasures: Conversely, China has retaliated against U.S. actions in some cases. In 2023, China banned Micron’s memory chips in certain infrastructure projects on alleged security grounds[20]. This ban benefitted SK hynix and Samsung in the short run – Chinese customers simply shifted orders to the Korean suppliers. Indeed, SK hynix likely gained market share in China at Micron’s expense in late 2023. However, there’s a geopolitical tightrope: China could similarly scrutinize SK hynix if relations worsen (though as of now, China needs SK hynix’s chips and has not targeted Korean firms). Additionally, increased Chinese investment in domestic memory companies (e.g. CXMT, YMTC) poses a long-term threat, though Chinese DRAM is still generations behind. Geopolitical tensions thus create both opportunity and risk: opportunity to grab business when a rival is banned, but risk of becoming the next pawn in the dispute.

- Korea–Japan Relations: In 2019, as mentioned, Japan’s curbs on exports of photoresists and etching gas to Korea created uncertainty for SK hynix. While this specific dispute was later resolved diplomatically, it highlighted supply chain vulnerabilities to political spats. SK hynix has since worked to localize or diversify critical materials sourcing to reduce such exposure.

- Government Policies and Subsidies: The global race to build semiconductor capacity (e.g. the U.S. CHIPS Act, EU Chips Act, and similar initiatives in Korea and Japan) could indirectly affect SK hynix. The company has announced investment in the U.S. – for example, a nearly $15 billion plan to build an advanced packaging and R&D facility in the United States over the next several years (partly to take advantage of U.S. incentives and to serve American customers)[53]. Such moves are essentially responses to geopolitical pressures to “friendshore” production. In Korea, SK hynix is likely to benefit from its government’s support for the chip sector (tax breaks for new fabs, etc.). Geopolitics is thus reshaping where SK hynix allocates capital.

- Regulatory Scrutiny: Being a large tech company, SK hynix also faces regulatory considerations. For instance, any future M&A (mergers and acquisitions) would likely be closely examined by multiple countries’ regulators for national security implications. The Intel NAND deal took over a year to get approved by regulators worldwide. Similarly, export control compliance and data security laws (like EU’s or China’s) are things SK hynix must navigate, given it operates globally.

Impact on Stock Price: Geopolitical news often causes swings in SK hynix’s stock. For example, when the U.S. announced new chip export curbs in October 2022, SK hynix’s stock dropped on fears it might have to halt its China fab expansion. Conversely, when waivers were confirmed, the stock regained some ground. Likewise, news of the Micron ban in China caused a short-term bump for SK hynix (as investors saw it as a win for the Korean firms). Ongoing talk of decoupling or restrictions keeps some risk premium on the stock – investors are aware that a sudden rule change could disrupt a chunk of SK hynix’s business.

In summary, geopolitical factors present both headwinds and tailwinds. SK hynix has thus far managed to avoid major fallout (thanks to exemptions and the crucial role it plays in the supply chain), but it remains vigilant. The company is diversifying geographically (building facilities in the U.S., considering others) and technically (maintaining a tech edge that few can substitute) to mitigate these external risks.

Industry Outlook and Emerging Technologies

Looking ahead, the overall outlook for the semiconductor and memory industry is optimistic, albeit with the usual caveats of cyclicality. Key trends and developments that could impact SK hynix include:

- Artificial Intelligence (AI) and Machine Learning: The rise of AI is a game-changer for memory demand. Training and running AI models (especially large language models, image processors, etc.) require enormous amounts of high-speed memory. HBM (High Bandwidth Memory) in particular has seen explosive growth – it’s now a critical component in AI accelerator GPUs. SK hynix, being the market leader in HBM, is poised to reap the benefits. Analysts predict AI will be a secular growth driver for memory for years. Goldman Sachs, for instance, recently noted we are entering “one of the strongest memory upcycles” driven by AI and forecast SK hynix’s HBM bit shipments to grow ~50% YoY[54][55]. This implies that even if other segments slow, AI could keep memory demand elevated. Outlook: Very positive for SK hynix – as long as it maintains technology leadership (which it’s doing by moving swiftly to HBM3E and HBM4), it should capture a large share of this growing pie. The risk is mainly if AI adoption falters or competitors catch up; but near-term (next 2–3 years), demand far outstrips supply in AI memory.

- 5G and Edge Computing: The continued global rollout of 5G networks and the proliferation of IoT devices will steadily boost memory requirements. Every new smartphone tends to have more DRAM and flash than the last. Moreover, 5G enables new use cases (AR/VR, richer media, connected vehicles) that ultimately drive more data generation and cloud storage – indirectly fueling demand for SK hynix’s products. While the smartphone market is mature, even modest growth or just a replacement cycle with higher memory content benefits SK hynix. Additionally, edge computing (processing data closer to where it’s generated) is emerging; many edge devices will need substantial memory and storage (for AI at the edge, etc.). SK hynix’s broad memory portfolio (from low-power mobile DRAM to high-end NAND) positions it to supply these needs. Outlook: Moderately positive – not a spike like AI, but a steady underpinning of demand.

- Cloud Services and Data Center Expansion: The major cloud service providers (AWS, Azure, Google, etc.) are consistently expanding their data center capacity. Each new server added typically includes tens to hundreds of gigabytes of DRAM and several terabytes of flash storage. Even apart from AI-specific servers, the general trend of cloud adoption means more “traditional” servers that use standard DRAM and SSDs. SK hynix will benefit from this organic growth. Enterprise IT spending on memory (for on-premises servers) also contributes. One interesting development is CXL (Compute Express Link) memory expansion modules – a new technology that allows data centers to flexibly add pooled memory. SK hynix has been working on CXL memory solutions (it demonstrated some in 2022–2023). If CXL gains traction, it could open new markets for selling memory in more modular forms to data centers. Outlook: Positive – as long as cloud and data generation graphs point up and to the right, so does memory demand.

- Advanced Computing and Graphics: Beyond AI, other compute-intensive applications like high-end graphics, gaming, and HPC (high-performance computing) require advanced memory (e.g., GDDR graphics memory, high-speed DDR5). SK hynix is a top player in GDDR as well (used in GPUs and game consoles) and is readying even faster iterations for new graphics cards. The advent of the metaverse and extended reality could also boost demand for high-performance memory in the future.

- Technological Advancements in Memory: SK hynix’s future also depends on its ability to keep advancing memory technology. On the DRAM side, the roadmap includes going to finer process nodes (the “1β, 1γ… nanometer class” DRAM) and new architectures. SK hynix is actively developing next-gen DDR6 and LPDDR6 for future systems. On the NAND flash side, the industry is moving to over 300 layers in 3D NAND. SK hynix has announced a 238-layer NAND and is working on higher-layer counts. More layers and new cell technologies (PLC – Penta-Level Cell maybe) could increase chip capacity and lower cost per bit. However, these advancements are complex and capital-intensive. If SK hynix executes well, it retains cost competitiveness; if it stumbles, it could lose share in the low-margin bits of the market. Thus far, SK hynix has been at parity with competitors on tech. It will need to sustain heavy R&D to keep up over the next decade.

- Emerging Memory & Storage Class Memory: The industry often talks about new forms of memory (like MRAM, ReRAM, etc.) and storage-class memory bridging DRAM and NAND (like Intel’s now-defunct 3D XPoint). SK hynix has dabbled in some of these (it had a phase-change memory project and is researching MRAM). While none of these have materially affected the business yet, SK hynix stays involved to not miss out. If any new memory tech becomes mainstream, SK hynix would aim to be a supplier or leverage it. For now, though, DRAM and NAND are expected to remain dominant and SK hynix’s focus is rightly there.

- Geopolitical and Supply Considerations: As noted earlier, external factors could impact the industry outlook. If, for example, U.S.–China tensions significantly restrict supply chains or markets, that could alter demand projections (e.g., if China cannot get enough memory, it might accelerate domestic efforts but in the meantime cause shifts in trade flows). Also, government incentives globally could lead to overcapacity in a few years – many new fabs are being incentivized in the U.S., Japan, India, etc. If all come online around the same time, the industry could swing to oversupply again mid/late-decade, affecting pricing and utilization. Analysts are aware of this risk, but currently the next 1-2 years look tight due to AI demand absorbing a lot of output[56].

To summarize the outlook: The semiconductor industry’s future is bright, with memory playing a crucial role in virtually all advancements (AI, 5G, IoT, cloud, automotive autonomy, etc.). For SK hynix, near-term developments like AI and DDR5 adoption present strong tailwinds, while longer-term growth in data-centric computing ensures a rising baseline demand. The company is expected to be a major beneficiary of these trends, though it must navigate the usual cyclical nature of the memory business and any external shocks. Analysts largely foresee robust memory market growth over the next few years, tempered by the understanding that “this time is not different” – i.e., at some point, supply will catch up and another correction will occur. SK hynix’s challenge and opportunity is to ride the growth trends, invest wisely during the boom, and emerge even stronger after the next cycle, a pattern it has followed for decades.

Valuation of SK hynix

Current Valuation Metrics (P/E, Market Cap, etc.)

As of late 2025, SK hynix’s valuation reflects its improved earnings and bullish outlook:

- Market Capitalization: SK hynix’s market cap is approximately ₩380 trillion, which is about $280–290 billion USD at current exchange rates[29]. This places it among the top 50 most valuable companies globally by market cap, and second in South Korea (behind Samsung Electronics). By comparison, Micron’s market cap is around $250 billion[30], and Intel’s around $180 billion[57], while Samsung Electronics is about $475 billion[27]. So SK hynix has closed the gap with (and even exceeded) some U.S. peers in size, despite historically trading at a discount (more on that below).

- P/E (Price-to-Earnings) Ratio: Based on trailing twelve months (TTM) earnings, SK hynix’s P/E ratio is ~15.6 as of November 2025[58]. This is a dramatic turnaround from a year earlier, when the company had negative earnings (hence no meaningful P/E) due to the downturn. It’s also a reasonable multiple in absolute terms, suggesting the stock is not in “bubble” territory relative to its current profits. For context, at the end of 2022 (when earnings were collapsing), SK hynix’s P/E was around 22 (using 2022’s small profit)[59], and at the end of 2023 it was negative[60]. The current ~15× multiple is in line with SK hynix’s mid-cycle historical average.

- Comparisons: SK hynix’s P/E is lower than many peers. Micron’s trailing P/E is ~29–30 (as of Nov 2025)[61][62], because Micron’s earnings are only just recovering (its fiscal TTM includes some loss-making quarters). Even on a forward basis, Micron trades around 12–13× 2026 earnings[63], whereas SK hynix, given its faster earnings recovery, might be closer to 10× forward earnings. Samsung Electronics trades around 15–20× earnings (its trailing P/E ~20, forward ~15)[64]. Intel has an extremely high trailing P/E (over 100) because its recent earnings were depressed, but forward P/E ~15–20 as it hopes for a turnaround[65]. So in summary, SK hynix’s valuation multiples are generally lower or on par with competitors – certainly not stretched.

- Other Multiples: The Price-to-Sales (P/S) ratio for SK hynix is currently about 5.0 (since market cap ~$280B and TTM sales ~$55B)[35][29]. Micron’s P/S is slightly higher (~6.5–7, with ~$38B revenue vs $250B cap), reflecting Micron’s lower margins at the moment. Samsung’s P/S is much lower (~2), but Samsung has lower margins and a conglomerate business mix. The Price-to-Book (P/B) ratio for SK hynix is ~5 as noted. The enterprise value to EBITDA (EV/EBITDA) multiple would be another lens; given SK hynix’s hefty EBITDA in 2024/25, that multiple is likely well under 10.

- Dividend Yield: SK hynix historically pays a modest dividend (it paid ₩1,200 per share in recent years, roughly 0.5–1% yield)[66]. With the stock price surge, the yield is now quite low (<0.5%). The company prioritized cash conservation in the downturn (it even reduced the dividend when losses hit), so income-focused investors don’t buy SK hynix for the yield.

In terms of absolute valuation, SK hynix’s ~$280B market cap is underpinned by the expectation of strong earnings going forward. If we annualize the Q3 2025 profit, for example, the company could make over $20B net profit in 2025, making the forward P/E ~13–14. This is relatively low for a company in a high-growth phase, but typical for memory due to the risk of earnings peaking.

Overvalued or Undervalued?

To assess whether SK hynix is over- or undervalued, one must consider both relative valuation and the cyclicality of earnings:

- Relative to Peers: By several measures, SK hynix appears undervalued compared to peers. As noted, its P/E and P/S are lower than Micron’s, despite SK hynix having higher revenue and profit. In fact, a recent comparison highlighted that SK hynix’s TTM revenue (~$50B) and earnings (~$27.5B pre-tax) vastly exceeded Micron’s ($31–37B revenue, ~$8B earnings), yet SK hynix’s market cap was slightly below Micron’s at one point[67][68]. This implied Micron was getting a richer valuation. One reason could be the difference in market listing: U.S. investors have easier access to Micron, whereas SK hynix (listed in Korea) historically trades at lower multiples. Korean stocks often have a “Korea discount” due to factors like lower foreign investor participation and corporate governance concerns[69]. For example, Hyundai Motor trades at a P/E of ~5 while U.S. automakers or Tesla trade far higher[69]. Similarly, SK hynix’s single-digit P/E (until recently) contrasts with Micron’s double-digit. This suggests that on a pure fundamentals basis, SK hynix might be undervalued – it produces comparable (or better) financial results yet its stock hasn’t been bid up as much.

- Relative to History: SK hynix’s current multiples are within its historical range. During peak euphoria in past cycles, the stock sometimes hit P/E as low as 4–6 (e.g. at the end of 2017, a boom year, SK hynix’s trailing P/E was ~2.5 because investors expected earnings to fall[70]). During troughs, P/E is not meaningful. So at P/E ~15, the market is neither pricing it like a cyclically-adjusted bargain (say P/E <10 would imply either skepticism or peak earnings) nor like a high-growth tech stock (P/E 30+). It’s roughly in between, which could imply the market expects continued earnings growth (justifying a moderate multiple) but is also cautious about the next downturn. Given that memory earnings can evaporate when the cycle turns, many value investors apply a low multiple to peak earnings. If one believes 2025–26 will be peak earnings, a mid-teens multiple is arguably fair. However, if one believes this cycle has structural differences (AI bringing a new level of sustained demand), then SK hynix might indeed be undervalued at current prices.

- Comparative Valuation Metrics: Another metric, EV/EBITDA, might show SK hynix around 8×, which is not high for a semiconductor firm with strong IP and market position. The PEG ratio (price/earnings to growth) also looks reasonable; SK hynix’s earnings growth from 2023 to 2025 will be enormous (off a low base), making PEG well below 1. Even using normalized mid-cycle earnings, PEG would be in a decent range given long-term memory demand growth prospects (~10% CAGR).

- Analyst Fair Value Estimates: Many analysts have been raising their price targets for SK hynix in 2023–2025. For instance, SK Securities (a local brokerage) recently issued a ₩1,000,000 target price – more than double the prior level – after the company’s record profits, which was one of the most bullish calls on the street[23]. Goldman Sachs also upgraded the stock to Buy in October 2025 and more than doubled its target from ₩300k to ₩700k[54]. These targets, if converted to USD, imply a valuation of ~$400B or higher for SK hynix (especially the ₩1M target). Such targets suggest analysts see further upside, i.e., they consider the stock undervalued relative to its growth prospects. It’s notable that at around ₩600k–₩620k current share price, SK hynix has already run up a lot, yet analysts are still finding justification for 15–60% further upside.

- Consideration of Risks in Valuation: The main argument one could make for the stock being fairly valued or overvalued is if we assume today’s earnings are near a cyclical peak. Memory is notorious for reverting – a couple years of super-profits often lead to capacity expansion and then a crash. If one assumes 2026–27 will see a downturn, the “E” in the P/E could drop, making the current price less cheap than it looks. For example, if earnings halved in a downturn, the forward P/E would effectively double. So some investors may be pricing in that caution. Additionally, SK hynix’s book value per share is much lower than the stock price now (P/B ~5 as mentioned), which isn’t unusual for a growth tech company, but it means there’s a lot of optimism baked into intangible value. If, say, AI demand fizzled or geopolitical issues hit, that optimism could deflate.

On balance, many market experts lean towards SK hynix being undervalued to reasonably valued, rather than overvalued, especially in comparison to peers. The stock’s huge rally in 2023–25 has been backed by equally huge earnings improvement, so its valuation multiples have not ballooned the way some other tech stocks have. For instance, NVIDIA’s P/E went over 100 during the AI craze, whereas SK hynix remained in the teens.

One can conclude that SK hynix’s stock does not appear excessively priced given its fundamentals. In fact, the “Korea discount” phenomenon suggests SK hynix trades at a lower multiple partly due to its listing locale, not purely its business performance[69]. If SK hynix were a U.S. company, it might well trade at 20–25× earnings given its market position – which implies upside. However, investors must weigh that against the certainty that memory cycles will swing. As Fitch Ratings pointed out, there is uncertainty about demand sustainability and policy impacts despite a rosy near-term outlook[46]. This keeps the valuation somewhat restrained.

Bottom line: SK hynix is likely not overvalued by conventional metrics, and could even be considered undervalued relative to its peers and potential. The current valuation reflects a mix of robust earnings momentum and lingering caution, a balance that seems justified for a cyclical leader in a critical industry.

Investor Sentiment and Analyst Views

General Investor Sentiment

Investor sentiment toward SK hynix has undergone a notable shift in the past year – from cautious or negative during the 2022 downturn to highly optimistic by late 2024 and 2025. A few points characterize the current sentiment:

- Optimism on AI and Growth: There is a broadly positive buzz around SK hynix as a key AI beneficiary. The market now views SK hynix not just as a commodity memory supplier but as an “AI play” – essential for NVIDIA GPUs, cloud AI, etc. This narrative has attracted investors who might not normally invest in cyclical stocks. As a result, SK hynix has seen increased foreign investor inflows and its share price hitting record levels (highest since 1999, as noted)[26]. Being in the spotlight for something as transformative as AI has improved sentiment dramatically.

- From Fear to Greed: In early 2023, sentiment was fearful – concerns about ongoing losses, high inventory, and whether the cycle would ever turn kept many investors on the sidelines. That sentiment began to thaw after SK hynix managed a surprise profit in Q4’23[21], signaling the worst was over. Since then, each quarter’s improvements have built confidence. By mid-2025, sentiment could be described as outright bullish, with some caution at the margins. The stock’s strong momentum fed a bit of a FOMO (fear of missing out) among investors as well.

- Market Perception vs Competitors: Interestingly, some investors still perceive SK hynix as undervalued relative to Micron or other global peers (as discussed in Valuation). Discussion on investment forums has pointed out that SK hynix trades at lower multiples and questioned why – often attributing it to market accessibility issues[71][69]. This indicates that savvy investors recognize a value case, further bolstering sentiment that the stock has room to run. In Korea, SK hynix is now regarded as one of the “national champion” tech stocks, and local sentiment is very positive, buoyed by national pride in the semiconductor sector’s success.

- Trading Trends: Over the past months, SK hynix has frequently been among the most actively traded stocks on the KRX. Retail interest is high (though large ownership is also by institutions and foreign investors). The stock’s inclusion in various MSCI and FTSE indices means broad exposure. Momentum traders have liked it due to the clear uptrend. There’s little sign yet of euphoria or bubble-like behavior (e.g. retail frenzy or meme-stock status) – the interest seems fundamentally driven.

Analyst Ratings and Recent Upgrades/Downgrades

Wall Street and regional analysts have largely been upgrading their outlook on SK hynix through 2023 and 2024:

- Goldman Sachs Upgrade: In a notable move, Goldman Sachs upgraded SK hynix to “Buy” from Neutral on Oct 31, 2025[54]. Goldman not only changed the rating but also more than doubled the price target – from ₩300,000 to ₩700,000[54]. Their rationale was very bullish: they expect “one of the strongest memory upcycles” extending through 2026, driven by AI server demand outpacing supply[72]. Goldman cited SK hynix’s leadership in HBM and new demand drivers (like CXL memory modules) as reasons earnings will surprise to the upside[73]. This call was significant because Goldman is a high-profile global broker; the upgrade likely drew additional international investors to take a look.

- Local Broker Upgrades: Korean brokerage firms have also been lifting their targets. The most eye-catching was SK Securities (an affiliate of the SK Group), which raised its 12-month target to ₩1,000,000 in November 2025[23]. They noted the stock had reached its highest level since 1999 after “record-breaking profits,” and responded by setting an aggressive target, effectively implying the stock could roughly double from current levels[23]. They also adjusted Samsung Electronics’ target upward at the same time, indicating a broad bullish stance on Korean chipmakers.

- Consensus Ratings: As of the latest, the consensus analyst rating for SK hynix is generally between a “Buy” and “Strong Buy.” Out of major analysts covering, a majority have buy-equivalent ratings, and the rest mostly hold neutrals. Very few, if any, have sell ratings at this point. This is a turnaround from mid-2022 when some analysts had cut ratings amid the bust. For instance, in 2022 some brokers downgraded SK hynix to Hold citing the coming earnings slump. Now, those same firms are upgrading again. One can think of it as analysts following the cycle: downgrading in downturns, upgrading in upturns – which, to be fair, mirrors the changes in fundamentals.

- Earnings Revisions: Analysts have been raising earnings estimates sharply. Since Q2 2023, SK hynix’s EPS estimates for 2024 and 2025 have been revised upward almost every month. Goldman in its report mentioned that consensus earnings forecasts have “risen rapidly since September [2025]” but that they believe “substantial upside remains”[56]. This suggests analysts collectively might still be underestimating SK hynix’s profit potential in this upcycle. It’s common in memory cycles that analysts are too pessimistic at the bottom and perhaps too optimistic at the very peak. Right now, we’re in the phase of catching up with optimism.

- No Major Downgrades Recently: There haven’t been notable downgrades in recent months. One area of slight concern some analysts voice is valuation/cycle timing – e.g., some could move to Hold if they think the stock has fully priced in the upswing. But given the data we have, the prevailing actions have been upgrades or reiterating buys with higher targets. Credit rating “upgrades” (outlook improvements by Fitch, Moody’s, etc.) have further reinforced positive sentiment from a credit perspective[45].

- What Are Analysts Saying? Beyond ratings, analysts are emphasizing SK hynix’s strengths. Morningstar, for example, highlighted SK hynix’s HBM leadership and resilient AI demand, raising their fair value by 20% after recent earnings beats[74]. Many note that mid-term risks (like oversupply) appear to be waning for now, and that SK hynix’s business strategy (focusing on higher-margin products) is paying off. There is of course some balanced commentary: concerns remain about the memory cycle’s historic volatility – i.e., “enjoy it while it lasts, but it won’t last forever.” However, even those cautious voices often conclude that the next couple of years look strong. Some have used this opportunity to compare SK hynix and Micron – and some are favoring SK hynix due to its tech lead in HBM and valuation. For instance, one Seeking Alpha analysis titled “SK hynix: Trading At A Mere 7x 2026E P/E vs peers at 10–12x” argued the stock is a bargain given its prospects[75].

In terms of investor communication, SK hynix’s management has also been upbeat yet measured. In conference calls, they acknowledge uncertainties but focus on how SK hynix is “now ready to grow into a total AI memory provider” given its technology leadership[51]. This messaging likely helps investor confidence by aligning the company with the most exciting growth areas.

Market Expert Perception

Market experts and commentators largely view SK hynix as a strategically well-positioned company in a favorable cycle. The stock is often cited in financial media as a top pick to play the AI trend indirectly (through memory). The Korea JoongAng Daily, for instance, ran a piece noting SK hynix’s market cap hitting a record on AI optimism, and flagged the “renewed investor optimism” and how closely SK hynix’s stock is correlating with Nvidia’s moves now[25][76]. This indicates the market sees SK hynix almost as an AI proxy.

The flip side is that some market experts caution that if the AI hype cools or if orders don’t live up to expectations in a year or two, SK hynix’s stock could be vulnerable. But at present, the mood is that such a scenario is not imminent – e.g., Micron’s CEO recently said “Our HBM is sold out for 2025”[77], implying demand is more than healthy. If Micron (which is #3 in memory) is sold out, SK hynix likely is as well, reinforcing bullish sentiment.

In summary, investor and analyst sentiment for SK hynix is strongly positive right now. The company is widely seen as a winner of current industry trends, and its financial comeback has instilled confidence. Analysts’ upgrades and lofty price targets reflect an expectation of further upside. However, there is an undercurrent of realism among some – acknowledging that memory remains cyclical. So far though, that hasn’t curbed the enthusiasm, as evidenced by the stock’s performance and the glowing analyst commentary in recent months.

Future Projections and Growth Potential

Growth Potential According to Analysts and Experts

Looking forward, SK hynix is projected to have significant growth opportunities. Analysts and industry experts generally agree that the company’s earnings can continue to expand in the near to mid-term, driven by multiple factors:

- Continued Memory Market Upswing: Industry projections (from firms like TrendForce, Gartner, etc.) see the memory market entering a sustained upcycle through at least 2025–2026. Global memory demand is expected to grow at a double-digit annual pace in those years, thanks to AI and data center needs. Goldman Sachs, in its upgrade, explicitly forecasts a multi-year upcycle for memory and implies SK hynix will see strong revenue and profit growth through 2026[54]. They believe consensus is still underestimating how tight the supply-demand balance will be. In numbers, some sell-side analysts predict SK hynix’s operating profit in 2025 could surpass its previous record (which was around ₩20+ trillion in 2018) and possibly approach ₩30 trillion if conditions are very favorable. That would be ~30%+ growth in profit from 2024 levels. While exact figures vary, the tone is that SK hynix’s earnings will likely grow further in 2025 before any moderation.

- HBM and Premium DRAM Growth: Because SK hynix is so well-positioned in HBM, experts see outsized growth in that segment. For example, Counterpoint Research expects the HBM market to more than double by 2026, and SK hynix, with currently ~60% share, could capture a large chunk of that expansion[6]. If Samsung ramps up HBM3E in 2024–25, SK hynix’s share might dip slightly (as the Astute Group article suggests Samsung could exceed 30% share next year)[6]. Even so, the pie is growing fast, so SK hynix’s HBM revenue can keep growing even if share normalizes a bit. Micron’s projection of $8B annual HBM revenue by 2026[78] gives a sense of scale; SK hynix’s HBM revenue could feasibly be on the order of $10–12B by then, given its lead – a huge jump from essentially near-zero a few years ago. Analysts thus project SK hynix’s revenue mix to tilt more toward high-margin AI memory, lifting overall growth and profitability.

- NAND Flash/SSD Recovery: While much attention is on DRAM, SK hynix’s NAND flash business is also expected to recover. NAND is still facing a slower recovery (oversupply persisted longer), but signs indicate 2024 will improve. SK hynix in 2023 had curtailed NAND investment to cut losses[48]. As prices rebound, the company could go from break-even or losses in NAND to solid profits by 2024/25. The integration of Solidigm (Intel’s SSD unit) also means SK hynix can introduce new SSD products. If PC and smartphone markets stabilize (which they have been into late 2023) and new game consoles or other devices drive storage demand, NAND flash revenue for SK hynix should climb. This represents an upside to future projections, as NAND was a drag in 2022–23. A note of caution: NAND is a commoditized, competitive market (with Samsung, Kioxia, WDC, Micron, and Chinese upstarts), so no one expects extraordinary growth here – but even moderate growth from a low base helps SK hynix’s totals.

- Micron vs SK hynix Projections: Some industry watchers have compared the two. Micron’s own outlook (provided in its investor events) is for a robust rebound with multi-year growth as well, and SK hynix is in a similar or better spot. Both see AI, automotive, and 5G as new demand drivers on top of traditional ones[79][80]. SK hynix in particular has articulated a vision of becoming a “total AI memory solutions provider,” indicating it will tailor products for emerging needs (as it mentioned customized solutions and new module types in its CFO’s statements[51]). This suggests SK hynix is aligning its R&D toward where growth will be, which bodes well for capturing that upside.

- Secular Demand Trend: A key point many experts make: we are in an era where “data is the new oil”. Data creation is exploding, and all that data resides in memory or storage at some point. By some estimates, global data storage and memory demand could double over the next 5 years. Even with cycles, the secular trend for memory is upward. SK hynix stands to benefit as long as it remains one of the dominant suppliers. In essence, the volume of bits the world needs is growing exponentially; the trick is managing price and supply. But in terms of sheer growth potential, the ceiling is high.

In summary, analysts see substantial growth potential for SK hynix in the next few years. Revenue and profit records set in 2024 may be broken again in 2025 or 2026 if trends hold. There is a broad consensus that SK hynix’s earnings 2–3 years out will be higher than today’s, though views diverge on how high (some bullish cases foresee extreme growth if AI demand keeps surprising to the upside).

Upcoming Products, Technologies, and Partnerships

SK hynix’s future growth will also be propelled by its product roadmap and strategic initiatives. Some key upcoming developments include:

- HBM3E and HBM4 Launch: SK hynix is on the cusp of mass-producing HBM3E, the enhanced version of HBM3, with even greater bandwidth, targeted for late 2023/early 2024 deployment[81]. This will go into the latest AI accelerators and should command premium pricing. More importantly, SK hynix has completed development of HBM4 (next-gen High Bandwidth Memory) and reports a 40% power efficiency boost and 10 Gbps speeds[9]. It plans to move to mass production once customer qualification is done[9]. HBM4 is likely to be the memory of choice for 2025–2026 AI hardware (e.g., NVIDIA’s next-gen “Rubin” GPU platform will use HBM4, and SK hynix is Nvidia’s primary HBM4 supplier)[7]. Additionally, Micron is also pushing HBM4 and Samsung will join, so the 2026 “battle for HBM4” is already in view[82]. SK hynix’s head start should translate to capturing high-value orders. These new HBM products will boost revenue per bit (they sell at far higher prices than standard DRAM) and reinforce SK hynix’s tech leadership image.

- DDR5 and Next-Gen DRAM: The industry transition from DDR4 to DDR5 memory in PCs and servers is ongoing. DDR5 has higher speeds and densities, meaning customers need to upgrade. SK hynix was a frontrunner in DDR5 rollout and continues to innovate (they even previewed a DDR5-based solution called MCR DIMM for servers)[83]. By 2024–25, DDR5 adoption in data centers will accelerate (Intel and AMD’s newest server CPUs use DDR5 exclusively). This should drive replacement demand that benefits SK hynix’s DRAM sales. Looking further out, SK hynix will develop DDR6 in a few years, keeping the pipeline flowing. For mobile, SK hynix introduced LPDDR5T (Turbo) and eventually will work on LPDDR6 – important for future smartphones and AR/VR devices that need fast, low-power memory[84].

- CXL Memory & New Module Types: As mentioned, SK hynix is preparing new memory module technologies such as LPCAMM (Low Power CAMM) for laptops and MCR DIMM for servers[83]. These are innovative form factors that could replace traditional SO-DIMMs in notebooks and offer better performance in servers. It’s also working on CXL memory expanders, which allow data centers to have pools of memory accessible via the CXL interface. In October 2023, SK hynix demonstrated a CXL memory device prototype. These products may start contributing meaningfully by 2025–2026, opening new revenue streams where SK hynix can sell not just raw chips but value-added memory subsystems.

- NAND Flash Roadmap: On the NAND side, SK hynix (with Solidigm) has been sampling a 238-layer 4D NAND (one of the highest layer counts in the industry so far). It’s expected to go to production and into SSDs that Solidigm will sell for client and data center use. They will continue pushing the layer count (e.g., 300+ layers later in the decade) and exploring technologies like QLC (4-bit) and PLC (5-bit per cell) to increase capacity. Also, SK hynix is likely to leverage Solidigm’s controller and firmware expertise to launch more competitive SSDs (perhaps a flagship NVMe drive for enterprise in the next year). Product launches in this area, while not as headline-grabbing as HBM, are crucial for SK hynix to capture more share in the storage market. With Western Digital and Kioxia facing uncertainty (they’ve discussed merging), SK hynix could seize opportunity if it executes well on upcoming SSD product releases.

- Strategic Partnerships: SK hynix’s collaborations will also shape its future:

- The NVIDIA partnership announced in Oct 2025 is particularly significant[12][13]. SK Group’s planned AI data center with 50,000 NVIDIA GPUs will not only consume a lot of SK hynix memory, but the deeper partnership means SK hynix can co-develop and optimize memory for NVIDIA’s needs. For example, working on base die design for custom HBM (as SK hynix is doing with TSMC’s help)[85] means tighter integration of memory and processors – potentially leading to stickier customer relationships. This AI factory initiative indicates SK hynix will have a direct hand in next-gen chip design and digital twin simulations (they’re using NVIDIA’s Omniverse for fab digital twins[86][87]). Over time, this could improve yields, shorten development cycles, and yield better products.

- SK hynix is also part of the Hynix-Intel-Solidigm chain, meaning it will continue to cooperate with Intel (even post acquisition) on certain SSD tech. Intel remains a big buyer of memory for its own products (like Optane’s successor, which was shelved, but maybe future needs).

- Government and academic partnerships (like with Purdue University for packaging R&D, as they announced a $4B investment in an advanced packaging facility in Indiana) will bolster SK hynix’s capabilities in chip packaging and heterogenous integration[53]. By late 2020s, advanced packaging (like stacking memory with logic, a concept akin to what HBM is but could extend further) may be a differentiator; SK hynix is preparing via such investments.

- Capacity Expansion Plans: To meet future demand, SK hynix will likely announce new fab expansions. It already has a mega-fab complex plan in Yongin, Korea (the so-called “SK hynix Semiconductor Cluster”) set to be built over the coming decade. There’s also talk of expanding its footprint in the U.S. beyond just packaging (depending on incentives) and perhaps in other regions. New capacity coming online around 2025–2027 will support volume growth (though the company will be careful to align expansions with demand to avoid glut). Analysts will watch these plans closely as they affect supply – but from SK hynix’s perspective, they need to invest to secure future market share.

All these upcoming launches and initiatives point to a company that is not standing still. On the contrary, SK hynix is doubling down on innovation and strategic growth areas. This aggressive roadmap is a reason analysts remain bullish – SK hynix is expected to not only maintain but extend its competitive advantages (tech leadership in HBM/DRAM, moving up the value chain in memory solutions, etc.).

Long-Term Outlook

In the long term (5+ years), SK hynix’s growth will eventually moderate as cycles play out, but the overall trajectory is expected to be upward. Key factors influencing long-term prospects:

- AI Everywhere: AI’s integration into virtually every industry (from healthcare to finance to transportation) means the demand for memory could be less prone to big downturns than in the past. If AI inference and training remain high priorities, SK hynix might experience more of a supercycle with smaller dips – this is a thesis some bulls have: that structural demand (AI, big data, IoT) will smooth out cycles to some degree. It’s too early to confirm this, but it’s a possibility that would favor long-term growth.

- Competition: SK hynix will face competition from Samsung and Micron continuously. How it navigates that will affect its growth. If SK hynix can stay ahead in technology and not engage in destructive price wars, it can secure healthy growth. The DRAM industry has consolidated to three players, which historically has led to more rational behavior – this is good for long-term profitability. In NAND, there are more players (6 major ones), and consolidation (like WDC-Kioxia) could happen, which might also help the industry’s health. Long-term, fewer players mean each can grow roughly with the market if disciplined.

- Diversification and New Business: SK hynix might explore diversifying within semiconductors (for instance, into logic chips or foundry via partnerships, though no concrete moves there yet). However, its core competence is memory. Perhaps more realistic is diversifying within memory – e.g., offering memory-as-a-service or software solutions with memory, or further developing the solutions business (like how Samsung has its own SSD controllers and portable SSD products, etc.). Any new revenue streams (even small ones) on top of selling chips could bolster growth.

- Sustainability of Growth: Eventually, memory bits become cheaper (cost per bit declines ~20% annually historically), so to grow revenue, volume needs to grow even faster or higher-value products must be introduced. SK hynix’s focus on high-value products (HBM, premium SSDs, etc.) is essentially an answer to this. There is a limit to how much volume the world can absorb in a short time, so adding value is key. Long-term growth will thus depend on innovation – introducing products that customers are willing to pay a premium for, rather than just selling commodity bits. SK hynix’s future projections built by analysts assume it will continue to succeed on that front.

In conclusion, the future for SK hynix looks promising. In the near term, it’s riding a wave of demand that should drive record results. Over the medium term, planned product launches and partnerships are likely to keep it at the forefront of memory technology, enabling it to capitalize on trends like AI, 5G, and cloud. Long-term, while cyclicality remains a factor, the fundamental demand for memory is only growing, providing a strong foundation for SK hynix’s continued expansion. The consensus among industry experts is that SK hynix is well-positioned to grow profitably in the coming years, making it one of the most exciting companies in the semiconductor sector to watch going forward.

(All financial figures in KRW have been converted to USD for clarity, using approximate contemporary exchange rates.)

Sources: SK hynix corporate fact sheet[1][2]; CompaniesMarketCap data[35][37]; SK hynix 4Q 2023 earnings release[38][40]; Korea JoongAng Daily (Jun 2025)[25][76]; Motley Fool/Nasdaq analysis[22][20]; CompaniesMarketCap stock performance data[18][15]; Reddit investing discussion[67][69]; Goldman Sachs upgrade via Investing.com[54][88]; GuruFocus news[23]; Astute Group industry report[6][9]; and additional sources as cited above.

Company Overview

- SK Hynix – Wikipedia

- Fact Sheet – SK hynix Newsroom

- Semiconductor 101: SK hynix’s Guide to Key Industry Players

HBM Leadership & AI Growth

- SK hynix Holds 62% of HBM Market, Micron Overtakes Samsung

- NVIDIA and SK Group Build AI Factory to Drive Korea’s Manufacturing and Digital Transformation

- SK Hynix’s HBM Leadership Continues to Impress Amid Resilient AI Demand

- HBM Gold Mine Sends SK hynix Revenues to a New High Point

- SK hynix Announces Semiconductor Advanced Packaging Investment in Purdue Research Park

Financial Results & Profitability

- SK hynix Reports Fourth Quarter 2023 Financial Results

- SK hynix Reports First Loss in a Decade as Memory Prices Fall

- SK Hynix Posts Record Profit After AI Boom Fuels Chip Demand

- SK Hynix Revenue History

Stock Performance & Valuation

- SK Hynix Stock Price History

- SK Hynix Surges to Record High on Strong Earnings

- SK Hynix P/E Ratio

- SK Hynix ADR Price vs Fair Value

- Goldman Sachs Upgrades SK Hynix to Buy on AI Memory Demand

- SK Hynix: Trading at a Mere 7x With Growing HBM Complexity

- Why Is SK Hynix Trading So Low Compared With Micron?

Market Capitalization & Industry Comparison

- SK Hynix Hits Record $157B Market Cap

- SK Hynix vs Micron Comparison

- Better Semiconductor Stock: Intel vs. Micron Technology

- Samsung Market Capitalization

- Micron Market Capitalization

- Intel Market Capitalization

Balance Sheet & Credit Ratings

- SK Hynix Total Debt

- Moody’s Affirms SK Hynix Baa2 Rating With Positive Outlook

- S&P Revises SK Hynix Outlook to Stable

- Fitch Revises SK Hynix Outlook to Positive