June 27, 2026

Micron (MU) June 2026 Update: The Memory Supercycle Got More Real, and More Dangerous

Technical data sourced via Interactive Brokers. Fundamental framing updates our May 2026 Micron article. This is analysis, not financial advice.

Overview

Micron did not just stay in the news in June. It became one of the clearest stress tests for the entire AI trade.

Our May article argued that the AI memory supercycle was real, that Micron had been re-rated from commodity memory producer to AI infrastructure bottleneck, and that the biggest risk was no longer whether demand existed. The risk was whether the market was paying a permanent-supercycle multiple for a business that could still face cyclicality, capex overshoot, customer pushback, or more memory-efficient AI models.

June sharpened both sides of that argument.

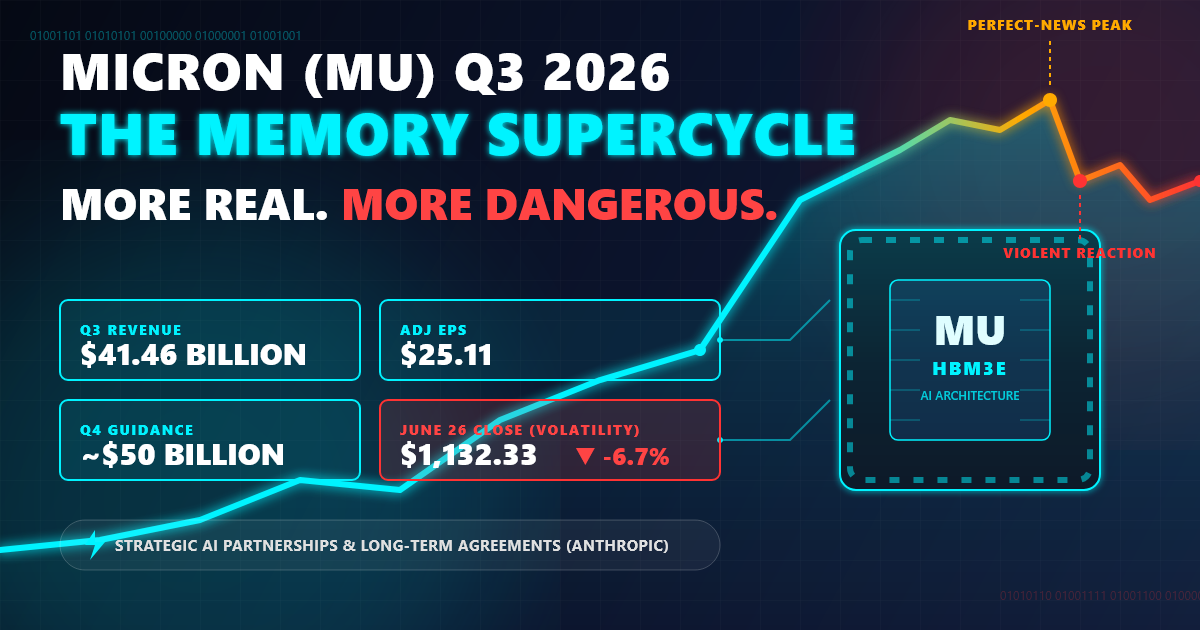

Micron’s fiscal Q3 results were extraordinary: revenue of $41.46 billion, adjusted EPS of $25.11, and guidance for roughly $50 billion of fiscal Q4 revenue. The company also became more visibly strategic to AI customers, including a reported Anthropic memory-and-storage partnership and long-term strategic customer agreements that reshape the business away from spot commodity memory.

But the stock also showed the other side of the setup. IBKR’s latest daily bar dated June 26, 2026 shows MU closing at $1,132.33, down 6.7% from its recent peak even though the technical trend is still bullish. That is the new Micron: fundamentals are exploding, but expectations are now so high that even a strong stock can trade violently around perfect-news events.

June Scorecard: What the May Article Got Right and Wrong

| Category | Assessment |

|---|---|

| Core thesis | Correct. AI memory demand, HBM scarcity, and pricing power continued to dominate. |

| $1T framing | Correct, but still too conservative. The stock pushed beyond the May milestone before pulling back. |

| Technical caution | Correct. MU remained bullish but volatile, and the stock is now in a measurable drawdown from its high. |

| Memory-efficiency risk | Still early, but more important. Rising memory costs make customers more motivated to optimize usage. |

| Biggest miss | We underestimated how quickly Micron could turn the “commodity memory” story into contracted, strategic infrastructure. |

| Biggest surprise | The scale of customer commitments: strategic agreements and AI partnerships are now central to the thesis. |

| Grade | B+ |

What We Got Right

The May article’s main call was right: Micron was not simply riding a short-term DRAM bounce. It was becoming one of the scarce suppliers of the memory layer behind AI infrastructure. June’s earnings confirmed that memory demand is broad, pricing is strong, and the market is still willing to pay for AI bottlenecks.

We were also right to warn that the chart was extended. The stock did not collapse, but it did stop being a clean straight-line move. A 6.7% drawdown after a historic run is not bearish by itself, but it confirms the point: this is not a low-volatility compounder.

What We Got Wrong

We were still too cautious on the power of customer lock-in. In May, we framed contracted HBM as an important bull-case support. In June, the story broadened: Micron is now being valued partly on strategic customer agreements, deposits, and long-term supply commitments across memory and storage.

That matters because it makes Micron look less like a spot-price commodity seller and more like a capacity allocator in a shortage market.

What Surprised Us

The biggest surprise was not the earnings beat. It was the business-model signal. The market is no longer only asking, “What is DRAM pricing this quarter?” It is asking, “How much future AI memory supply is already spoken for, and how much cash are customers willing to commit to secure it?”

That is a very different conversation.

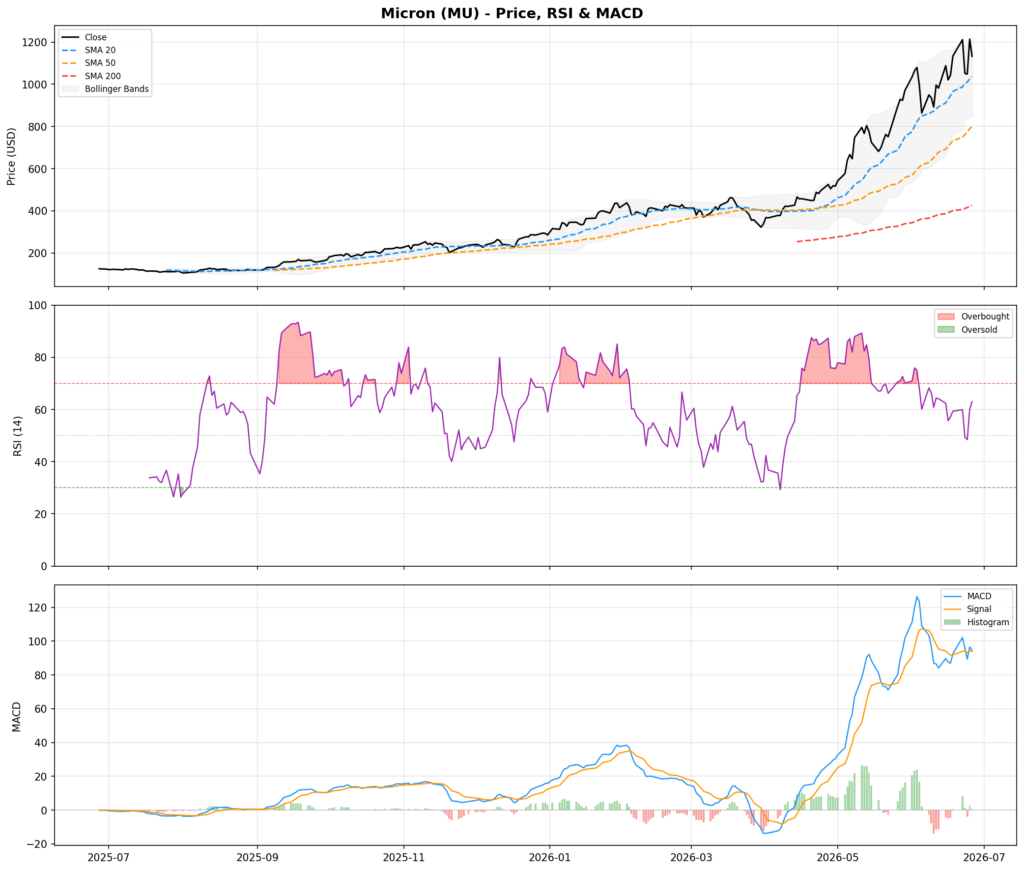

Live Technical Data via IBKR

As of latest IBKR daily bar dated June 26, 2026

| Indicator | Value |

|---|---|

| Last Close | $1,132.33 |

| SMA 20 | $1,035.41 |

| SMA 50 | $802.14 |

| SMA 200 | $425.84 |

| RSI (14) | 63.0 |

| MACD | 94.5245 |

| MACD Signal | 94.0487 |

| BB Upper | $1,222.09 |

| BB Lower | $848.73 |

| 1-Year Return | +807.6% |

| Current Drawdown | -6.7% |

| Max 1-Year Drawdown | -30.3% |

| Trend | BULLISH |

| RSI Signal | Neutral |

The chart is still bullish. The moving average stack remains clean: SMA 20 > SMA 50 > SMA 200. Price is also still above the 20-day average, which means the near-term trend has not broken.

But the tone is different from May. In May, MU was at a fresh all-time high with a 0.0% drawdown and RSI near overbought. In June, the stock is still strong, but it is no longer pinned to the absolute high. RSI has cooled to 63.0, MACD is only slightly above signal, and price is sitting between the 20-day average and the upper Bollinger band rather than riding the upper rail.

That is healthier technically, but also more complicated. The stock has room to reset without invalidating the trend, but it has also started to show how quickly sellers can appear when expectations are extreme.

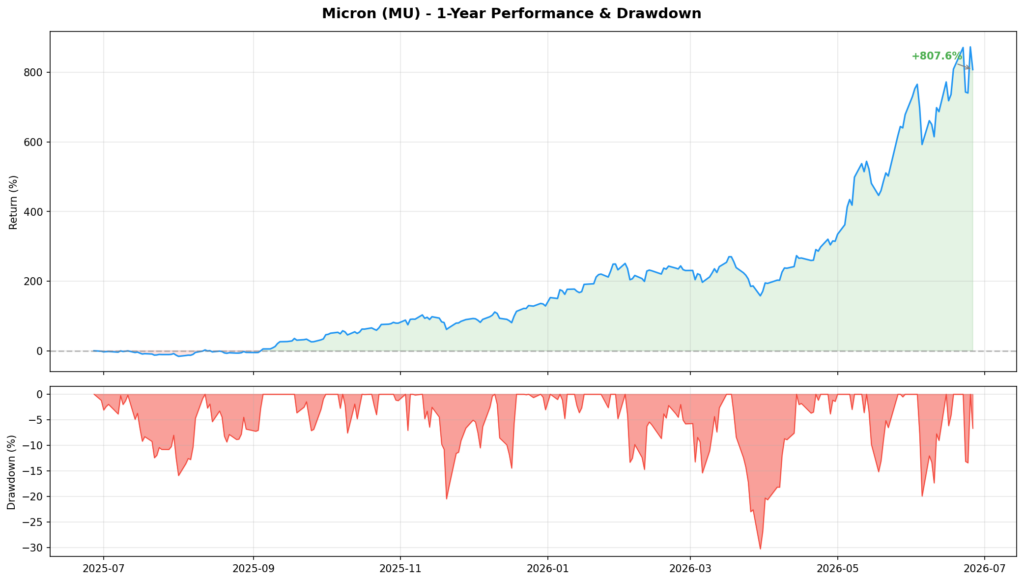

Performance and Drawdown

MU is still up 807.6% over the trailing year. That is almost impossible to overstate. Even after the latest pullback, the stock remains one of the defining AI infrastructure winners of 2026.

The key number is the drawdown. A -6.7% current drawdown is ordinary for this stock, especially compared with the -30.3% maximum drawdown over the same one-year window. But ordinary does not mean irrelevant. At this valuation, a 20-30% correction can happen without the long-term thesis being broken.

That is the risk profile investors need to internalize: the trend can be right and the stock can still punish late entries.

The Fundamental Update: June Was a Blowout

Micron’s fiscal Q3 report was stronger than the market expected on almost every major line.

| Metric | June Update |

|---|---|

| Fiscal Q3 revenue | $41.46B |

| Adjusted EPS | $25.11 |

| Reported Q4 revenue guide | Around $50B |

| Q4 adjusted EPS guide | Around $31 |

| Direction of margins | Still expanding |

| Main driver | AI memory demand and constrained supply |

The important part is not just that Micron beat estimates. It is that the forward guide supported the idea that the cycle is not rolling over yet.

In the old memory model, investors expected good quarters to plant the seed of the next bad cycle. Strong prices invite capex, capex creates supply, supply crushes price. That cycle has not disappeared. But June showed that the shortage is lasting long enough for Micron to earn extraordinary profits before new supply catches up.

The New Bull Case: Strategic Scarcity, Not Just Cyclical Pricing

The bull case is now stronger than it was in May, but also more crowded.

1. Memory Has Become a Strategic Input

The Anthropic partnership matters because it shows Micron being pulled directly into frontier-model infrastructure design. This is not just “sell DRAM into the channel.” It is memory, HBM, DRAM, and SSDs being treated as a co-designed piece of the AI stack.

That gives Micron more relevance and potentially more durable customer relationships.

2. Long-Term Agreements Reduce Commodity Exposure

The reported strategic customer agreements are the most important development. If customers are committing years ahead and putting real money behind supply reservations, Micron’s revenue base becomes less dependent on spot pricing.

That does not eliminate cyclicality, but it changes the shape of it.

3. HBM Still Has a Die-Penalty Advantage

HBM consumes more wafer area per bit than standard DRAM. That keeps broader DRAM supply tight when producers prioritize AI memory. Micron benefits twice: premium HBM pricing and tighter supply in conventional memory.

4. The AI Cost Stack Is Moving Toward Memory

The more AI shifts from training to large-scale inference, long-context workloads, retrieval, agents, and persistent memory, the more important memory bandwidth and capacity become.

That is the cleanest reason Micron’s multiple has expanded.

The Bear Case: The Better the Story Gets, the Less Room for Error

The bearish case is not that Micron is weak. It is that the stock now requires the supercycle to remain exceptional.

1. Customer Pain Is Becoming Visible

The May article warned that if Micron’s profits explode, those profits come from somewhere. In June, that became a sharper issue. AI labs, cloud providers, device makers, and storage customers are absorbing rapidly rising memory costs.

That can support Micron in the short run. But over time, high input costs create customer behavior changes: redesigns, supplier diversification, inventory discipline, lower precision, compression, and architecture work aimed at using less memory per unit of AI capability.

2. Memory Efficiency Is Still the Structural Risk

This remains the most important long-term risk.

If AI capability keeps requiring more HBM, more DRAM, larger KV caches, and more storage, Micron wins. If software progress reduces memory intensity faster than usage expands, the bull case weakens.

The market is currently pricing Micron as though memory intensity stays high. That may be right. But it is no longer a cheap assumption.

3. Capex Is Rising Fast

Micron is spending aggressively to meet demand. That is rational in a shortage, but it is also how memory cycles eventually turn. If industry capex arrives into a demand slowdown in 2027 or 2028, pricing can move against producers quickly.

This is the classic memory-cycle risk, and it has not been repealed.

4. Valuation Has Less Margin for Disappointment

At more than $1,100 per share and roughly a trillion-dollar-plus equity value using the same share-count framework as the May article, Micron is no longer undiscovered. It is a consensus AI infrastructure winner.

The market can forgive volatility. It will not forgive evidence that margins, HBM share, customer commitments, or AI memory demand are peaking.

What Matters Most From Here

| Signal | Why It Matters |

|---|---|

| HBM share and qualification wins | Determines whether Micron remains a premium AI supplier or loses ground to SK Hynix/Samsung |

| Strategic customer deposits | Shows how much future revenue is genuinely locked in |

| Q4 gross margin and FY2027 capex | Tells us whether profitability scales faster than spending |

| DRAM/NAND spot pricing | Early warning for cyclicality returning |

| Customer behavior | High prices may push AI labs and device makers to reduce memory intensity |

| Technical support near SMA 20 | A break below the 20-day would mark a real short-term momentum change |

Updated Investment Assessment

| Factor | View |

|---|---|

| Long-term outlook | Still constructive, but now dependent on sustained AI memory scarcity |

| Near-term technicals | Bullish, less stretched than May, but volatile |

| Fundamental momentum | Extremely strong after fiscal Q3 and Q4 guidance |

| Valuation | High-expectation, not bargain territory |

| Biggest upside driver | Contracted AI memory demand and HBM scarcity |

| Biggest downside risk | Memory-efficiency gains, capex oversupply, or customer cost pushback |

| Risk level | High |

Micron’s June update makes the May thesis stronger, but not safer.

The company has moved deeper into the center of the AI infrastructure stack. The results, guidance, customer agreements, and Anthropic partnership all support the idea that memory is no longer being treated as a generic commodity input. It is becoming strategic capacity.

But the stock already reflects that. The easy part of the re-rating is over. From here, Micron has to prove that the memory supercycle is not just a violent cyclical boom, but a structurally durable cash-flow regime.

Bottom line: Micron remains one of the purest public-market ways to invest in the AI memory bottleneck. June made the bull case more credible, but it also made the valuation more demanding. The next debate is not whether Micron is benefiting from AI. It clearly is. The debate is whether today’s extraordinary profitability is the new baseline or the top half of another memory cycle.