June 2, 2026

SK hynix Stock Analysis: The AI Memory Leader Is Still Winning, but the Chart Is Hot

Technical data sourced from the Interactive Brokers API for SK hynix’s Korea Exchange listing (KRX:000660). Fundamental data is based on SK hynix’s official earnings releases and newsroom announcements.

Overview

SK hynix has moved far beyond being treated as a conventional cyclical memory manufacturer. The market now sees the company as one of the critical infrastructure suppliers for the AI buildout: a leader in high-bandwidth memory (HBM), an increasingly important supplier of high-capacity server DRAM and enterprise SSDs, and a company pushing into more customized memory products for next-generation AI systems.

The stock reflects that change in perception. Interactive Brokers’ daily bar for June 2, 2026 shows SK hynix closing at KRW 2,360,000, up 985.1% over the returned one-year window. The share price is almost eleven times where it stood at the start of that period.

The fundamental results have also been extraordinary. In its first-quarter 2026 results, SK hynix reported KRW 52.5763 trillion in revenue, KRW 37.6103 trillion in operating profit, and a 72% operating margin. Revenue grew 198% year over year and operating profit grew 405%. Those are not normal memory-cycle numbers.

The investment question is no longer whether SK hynix is benefiting from AI. It clearly is. The question is how much future success is already priced into a stock that has risen nearly 10x in one year.

Live Technical Data From Interactive Brokers

As of the latest IBKR daily bar dated June 2, 2026

| Indicator | Value |

|---|---|

| Last Close | KRW 2,360,000 |

| SMA 20 | KRW 1,935,950 |

| SMA 50 | KRW 1,408,540 |

| SMA 200 | KRW 775,508 |

| RSI (14) | 75.4 |

| MACD | 266,542 |

| MACD Signal | 235,597 |

| Bollinger Upper Band | KRW 2,470,523 |

| Bollinger Lower Band | KRW 1,401,377 |

| 1-Year Return | +985.1% |

| Current Drawdown | -0.1% |

| Max 1-Year Drawdown | -26.6% |

| Trend | BULLISH |

| RSI Signal | Overbought |

What the Chart Is Telling Us

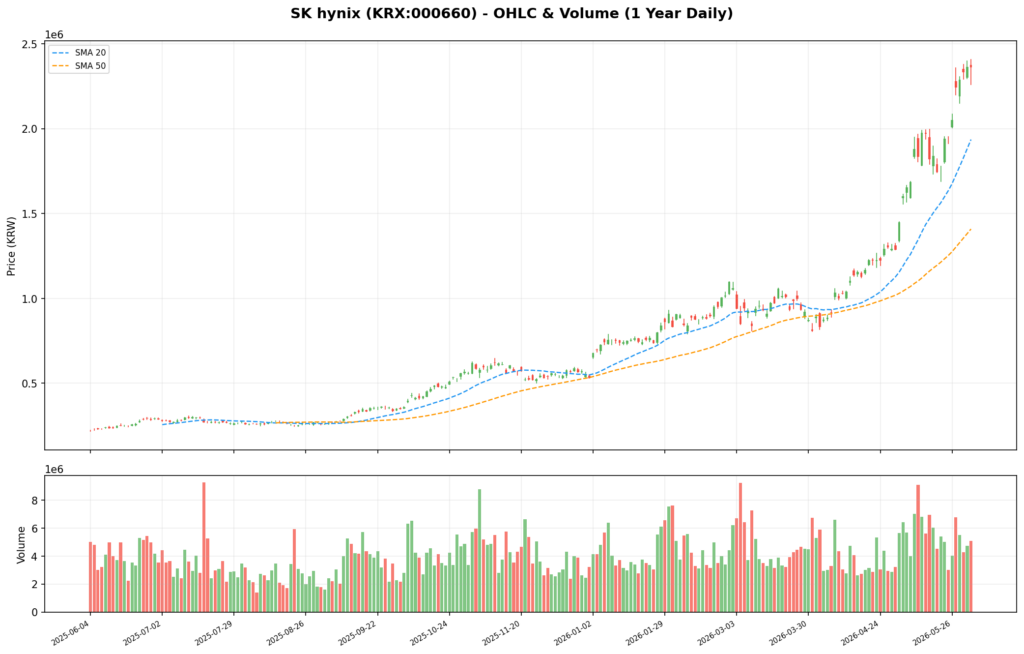

OHLC Price and Volume

The trend is unambiguously bullish. The moving averages are stacked in the strongest possible order:

SMA 20 (KRW 1.936M) > SMA 50 (KRW 1.409M) > SMA 200 (KRW 775,508).

The closing price is roughly 22% above the 20-day average, 68% above the 50-day average, and more than 200% above the 200-day average. That confirms the strength of the move, but it also tells us this is not an attractive low-risk entry point. The stock is priced for continued operational excellence.

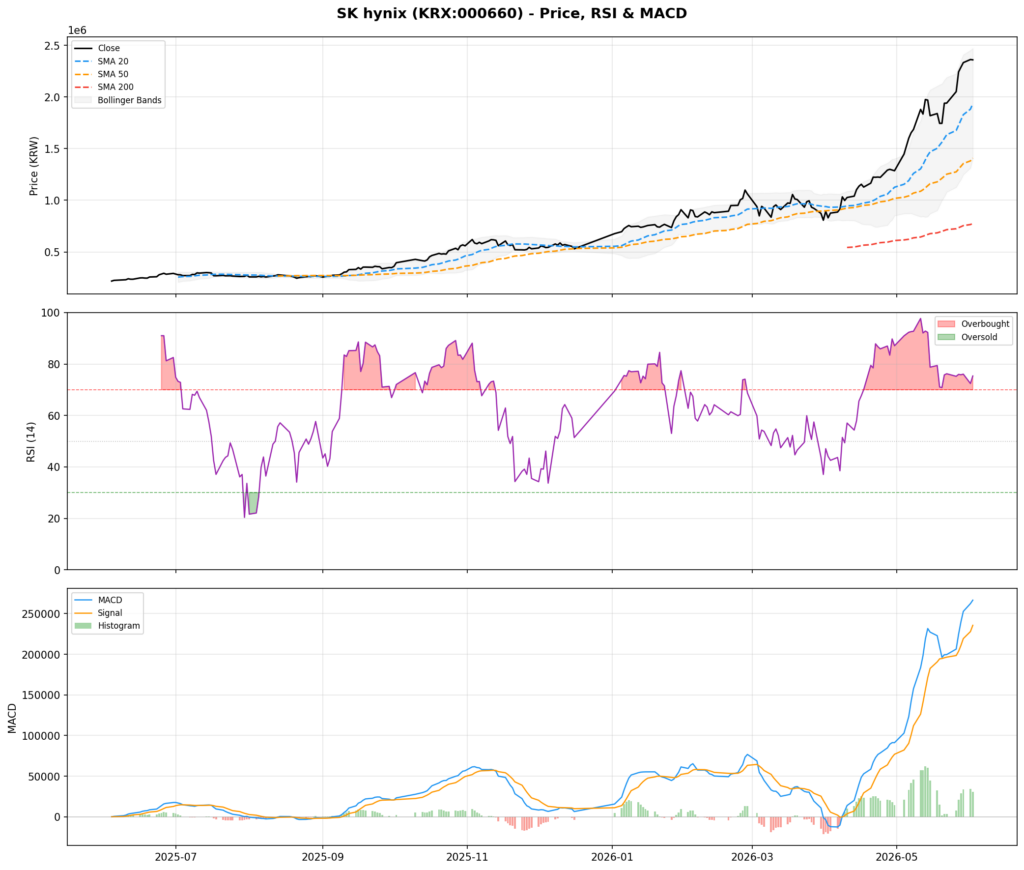

RSI, MACD, and Bollinger Bands

RSI is 75.4, above the conventional overbought threshold of 70. An overbought reading is not an automatic sell signal in a powerful momentum trend, but it means buyers are chasing a stock with limited short-term slack.

MACD remains constructive: the MACD line at 266,542 is above its 235,597 signal line. Momentum has not rolled over yet.

The stock is also close to its upper Bollinger band at KRW 2.471M. The first support level is the 20-day average near KRW 1.936M. A deeper pullback toward the 50-day average near KRW 1.409M would be painful, but it would not automatically break the long-term uptrend.

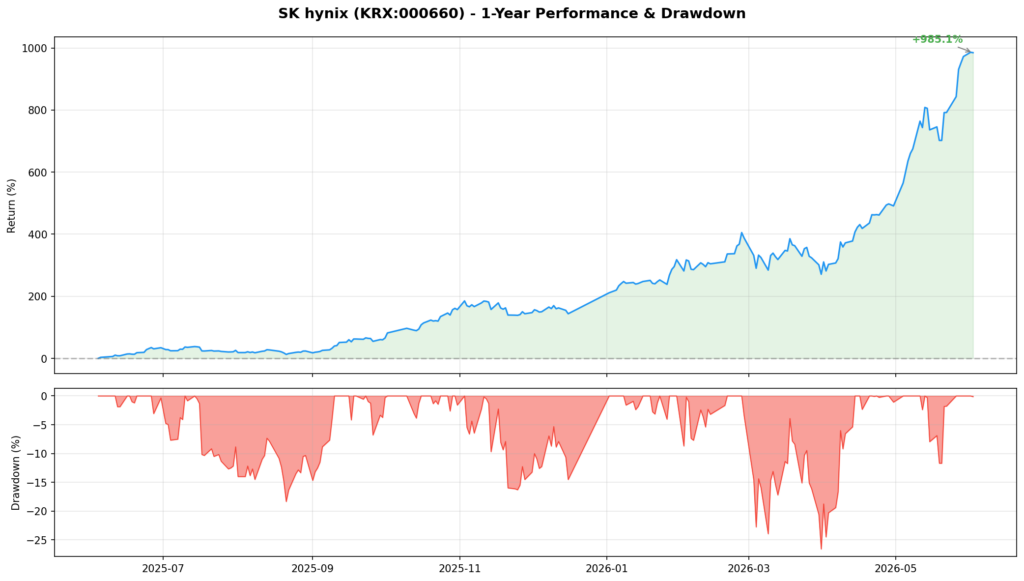

Performance and Drawdown

The trailing one-year return is +985.1%, while the current drawdown is only -0.1%. Even during that rally, however, the stock experienced a -26.6% peak-to-trough decline. This remains a volatile memory stock, not a steady defensive compounder.

Scorecard: What Our November 2025 SK hynix Article Got Right and Wrong

We previously wrote about Sk Hynix, the article itself was published on November 4, 2025. You can read the original piece here: SK hynix: Powering the Future of Memory and Semiconductor Innovation.

What we got right

1. HBM leadership was the central thesis, and it mattered.

The November article focused on SK hynix’s position as an AI-memory leader rather than treating it as a generic DRAM company. That framing was correct. SK hynix said its record FY2025 results were driven by AI-memory competitiveness and higher-value products including HBM. In Q1 2026, management again cited HBM, high-capacity server DRAM modules, and eSSDs as major drivers.

2. The HBM4 roadmap was real, not promotional noise.

The earlier article highlighted HBM4 as the next major product cycle. SK hynix completed development and prepared its HBM4 mass-production system in September 2025. By Q3 2025, the company said HBM4 shipments would begin in the fourth quarter. That roadmap is now feeding into a broader next-generation AI memory portfolio.

3. The Solidigm and enterprise-storage angle was relevant.

The prior article did not focus only on HBM. That was useful. Q1 2026 results specifically identified eSSDs as part of the record quarter, and management said it plans to use Solidigm’s high-capacity QLC eSSD strengths to compete in AI data centers.

4. The memory upcycle lasted longer and became stronger.

We argued that AI demand, constrained supply, and premium products could sustain a multi-year upcycle. FY2025 revenue reached KRW 97.1467 trillion, up 47%, while operating profit reached KRW 47.2063 trillion, up 101%. Q1 2026 then accelerated far beyond that already strong base.

What we got wrong or underestimated

1. We underestimated the magnitude of the earnings expansion.

The November article discussed the possibility that 2025 operating profit could approach KRW 30 trillion under favorable conditions. Actual FY2025 operating profit was KRW 47.2063 trillion. Q1 2026 operating profit alone was KRW 37.6103 trillion.

2. We underestimated the speed of the stock repricing.

The earlier article treated SK hynix as undervalued relative to its AI-memory leadership. That direction was right, but the magnitude was not. A 985.1% one-year move is much larger than the valuation rerating we were contemplating.

3. Some precise market-share and valuation snapshots aged too quickly.

The previous article used a mid-2025 HBM market-share estimate and late-2025 market-cap comparisons. Those were useful snapshots, but this market has moved too quickly to anchor a June 2026 thesis around them. The better question now is whether SK hynix can keep converting product leadership into earnings while industry capacity rises.

4. The old article gave conventional memory cyclicality too little weight in the final conclusion.

The bullish call worked, but the stock’s own -26.6% drawdown during a nearly 10x year is a reminder that even a correct long-term thesis can produce violent corrections.

Fundamental Update: A Business Performing at an Exceptional Level

Q1 2026 broke the scale of the old model

SK hynix’s Q1 2026 results deserve to be stated plainly:

| Metric | Q1 2026 | YoY Change |

|---|---|---|

| Revenue | KRW 52.5763T | +198% |

| Operating Profit | KRW 37.6103T | +405% |

| Operating Margin | 72% | +30 percentage points |

| Net Income | KRW 40.3459T | +398% |

The company also ended the quarter with KRW 54.3 trillion in cash and cash equivalents and KRW 19.3 trillion in interest-bearing debt, producing a KRW 35 trillion net-cash position. That balance sheet matters because SK hynix plans to increase investment significantly, including the M15X ramp, Yongin cluster infrastructure, and EUV equipment.

The product story is widening

HBM remains the core advantage, but SK hynix is building a broader AI-memory stack:

- In April 2026, the company began mass production of a 192GB SOCAMM2 module designed for NVIDIA’s Vera Rubin platform. SK hynix said it more than doubles bandwidth and improves power efficiency by over 75% versus conventional RDIMM.

- In May 2026, SK hynix announced an iHBM thermal solution that integrates cooling elements into the HBM package and reduces thermal resistance by 30%.

- The Q1 release also highlighted LPDDR6, 321-layer QLC NAND products, and high-capacity eSSDs.

This is important because the bull case is not simply “AI needs more DRAM bits.” SK hynix is trying to sell higher-value, workload-specific solutions where performance, power efficiency, packaging, and thermal management all matter.

The Micron Read-Through

Our May 2026 Micron analysis is relevant because Micron and SK hynix are riding the same industry structure: HBM demand is pulling capacity toward premium AI products, conventional DRAM supply remains tight, and the market is assigning memory companies much higher valuations than it did in older cycles.

The most important shared bear case is also the same: AI models may become substantially more memory-efficient. Distillation, quantization, KV-cache compression, sparse architectures, and better inference software could reduce memory required per unit of AI capability.

SK hynix itself addresses the counterargument in its Q1 release: management expects efficiency improvements to make AI services more economical, expand usage, and drive more aggregate memory demand. That may be right. Lower inference cost can create far more inference demand. But investors should recognize that this is now one of the central assumptions behind the valuation.

Valuation: The Stock Requires Scenario Analysis

SK hynix’s official ownership structure page lists 728,002,365 shares as of December 31, 2025. Applying the June 2 IBKR close of KRW 2.36M implies a rough equity value of about KRW 1,718 trillion, before considering later treasury-share handling.

That produces two very different valuation lenses:

| Valuation Lens | Approximate Result |

|---|---|

| Equity value / FY2025 net income | ~40x |

| Equity value / annualized Q1 2026 net-income run rate | ~10.6x |

Neither number should be used mechanically. FY2025 understates the current earnings power, while annualizing one extraordinary quarter assumes margins and pricing remain near peak levels. Q1 net income also exceeded operating profit, which is another reason to avoid treating the quarterly run rate as a permanent base.

My view: SK hynix can still grow into part of this valuation if HBM4, SOCAMM2, server DRAM, and eSSD demand stay tight. But after a nearly 10x one-year move, the stock no longer offers much protection if margins normalize faster than expected.

Bull Case

1. SK hynix remains one of the best-positioned AI infrastructure suppliers.

Memory bandwidth and power efficiency are real bottlenecks. HBM4, SOCAMM2, and iHBM are direct responses to those constraints.

2. The mix shift supports structurally better economics.

Designed-in, performance-sensitive AI memory is more valuable than undifferentiated commodity DRAM. If a larger share of revenue comes from advanced products, the historical low-multiple memory framework becomes less useful.

3. Strong cash generation funds the next capacity cycle.

The company moved to a KRW 35 trillion net-cash position even as it prepares major investments. That reduces financing risk and gives SK hynix room to defend its technology lead.

4. AI inference could broaden demand rather than replace training demand.

If agentic AI creates constant, real-time inference workloads across many services, total memory demand can keep rising even as each model becomes more efficient.

Bear Case

1. The chart is stretched.

RSI is overbought, the stock is close to its upper Bollinger band, and the closing price is far above its 50-day and 200-day averages. A strong company can still have a sharp correction.

2. Memory efficiency may become a real demand headwind.

If software improvements reduce memory intensity faster than AI usage grows, the market could reassess the assumption that demand remains structurally supply-constrained.

3. Capacity expansion can recreate the old memory cycle.

SK hynix is increasing investment, while Samsung and Micron are pursuing the same opportunity. If new supply arrives after demand growth cools, premium pricing and margins can compress quickly.

4. Peak margins create difficult comparisons.

A 72% operating margin is exceptional. The market may punish even strong results if margins decline from that level.

5. Competition remains serious.

SK hynix has executed well, but Samsung and Micron are not standing still. HBM yields, customer qualifications, packaging, thermals, and supply stability will determine who captures the highest-value orders.

Bottom Line

Our November 2025 SK hynix thesis was directionally right: HBM leadership, AI-server demand, premium memory products, and Solidigm’s storage capabilities mattered. We were too conservative about the magnitude. SK hynix’s earnings and stock price expanded much faster than the earlier article anticipated.

The updated view is more demanding. Fundamentally, SK hynix is executing at an extraordinary level and widening its advantage from HBM into a broader AI-memory platform. Technically, the stock remains bullish but overheated: RSI is above 75, the shares are near the upper Bollinger band, and the price has risen almost 10x in one year.

| Factor | View |

|---|---|

| Business quality | Strong and improving |

| AI-memory position | Industry-leading |

| Balance sheet | Strong net-cash position |

| Near-term technicals | Bullish but overbought |

| Valuation | Supportable only if elevated earnings persist |

| Risk level | High after a nearly 10x run |

Investment assessment: SK hynix remains one of the highest-quality ways to invest in AI-memory infrastructure, but the easy rerating is behind it. At this price, the stock should be treated as a high-expectation momentum holding rather than an undiscovered value opportunity. The critical signals to watch are HBM4 execution, AI-server memory demand, capacity expansion, and whether memory-efficiency gains expand total AI usage or reduce the amount of memory the industry ultimately needs.

Disclosure: This article is for informational purposes only and does not constitute financial advice. Technical data was sourced from Interactive Brokers using its data. Fundamental figures are based on SK hynix’s official releases and remain subject to the company’s stated review and forward-looking-statement disclaimers.